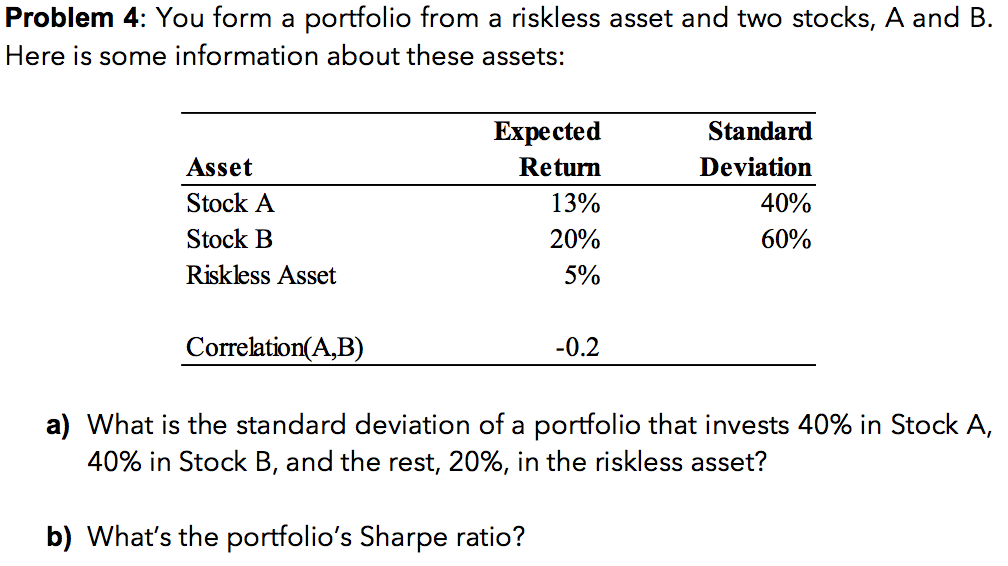

Question: Problem 4: You form a portfolio from a riskless asset and two stocks, A and B. Here is some information about these assets: Asset Stock

Problem 4: You form a portfolio from a riskless asset and two stocks, A and B. Here is some information about these assets: Asset Stock A Stock B Riskless Asset Expected Return 13% 20% 5% Standard Deviation 40% 60% Correlation(A,B) 0.2 a) What is the standard deviation of a portfolio that invests 40% in Stock A, 40% in Stock B, and the rest, 20%, in the riskless asset? b) What's the portfolio's Sharpe ratio? Problem 4: You form a portfolio from a riskless asset and two stocks, A and B. Here is some information about these assets: Asset Stock A Stock B Riskless Asset Expected Return 13% 20% 5% Standard Deviation 40% 60% Correlation(A,B) 0.2 a) What is the standard deviation of a portfolio that invests 40% in Stock A, 40% in Stock B, and the rest, 20%, in the riskless asset? b) What's the portfolio's Sharpe ratio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts