Question: Problem 4-13 Net Operating Losses (LO 4.9) Tyler, a single taxpayer, generates business income of $3,000 in 2016. In 2017, he generates an NOL of

Problem 4-13 Net Operating Losses (LO 4.9)

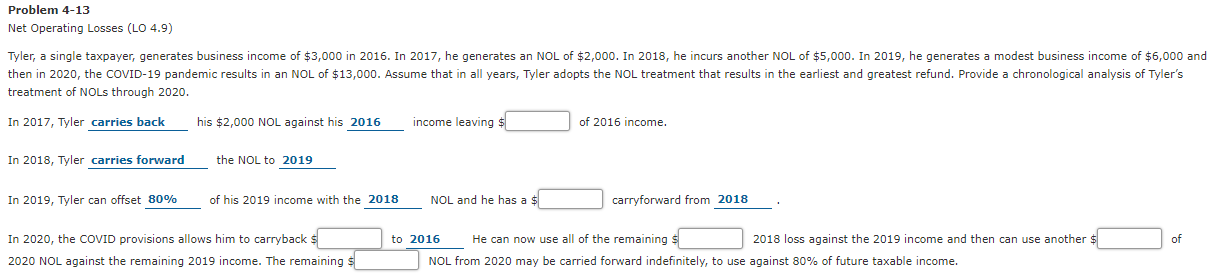

Tyler, a single taxpayer, generates business income of $3,000 in 2016. In 2017, he generates an NOL of $2,000. In 2018, he incurs another NOL of $5,000. In 2019, he generates a modest business income of $6,000 and then in 2020, the COVID-19 pandemic results in an NOL of $13,000. Assume that in all years, Tyler adopts the NOL treatment that results in the earliest and greatest refund. Provide a chronological analysis of Tylers treatment of NOLs through 2020.

In 2017, Tyler carries back his $2,000 NOL against his 2016 income leaving _____fill in the blank 3 of 2016 income. In 2018, Tyler carries forward the NOL to 2019 _______ In 2019, Tyler can offset 80% of his 2019 income with the 2018 NOL and he has a _______ fill in the blank 8 carryforward from 2018 . In 2020, the COVID provisions allows him to carryback _______ fill in the blank 10 to 2016 He can now use all of the remaining ______ fill in the blank 12 2018 loss against the 2019 income and then can use another ______ fill in the blank 13 of 2020 NOL against the remaining 2019 income. The remaining _____ fill in the blank 14 NOL from 2020 may be carried forward indefinitely, to use against 80% of future taxable income.

Problem 4-13 Net Operating Losses (LO 4.9) Tyler, a single taxpayer, generates business income of $3,000 in 2016. In 2017, he generates an NOL of $2,000. In 2018, he incurs another NOL of $5,000. In 2019, he generates a modest business income of $6,000 and then in 2020, the COVID-19 pandemic results in an NOL of $13,000. Assume that in all years, Tyler adopts the NOL treatment that results in the earliest and greatest refund. Provide a chronological analysis of Tyler's treatment of NOLs through 2020. In 2017, Tyler carries back his $2,000 NOL against his 2016 income leaving $ of 2016 income. In 2018, Tyler carries forward the NOL to 2019 In 2019, Tyler can offset 80% of his 2019 income with the 2018 NOL and he has a $ carryforward from 2018 of In 2020, the COVID provisions allows him to carryback s 2020 NOL against the remaining 2019 income. The remaining s to 2016 He can now use all of the remaining $ 2018 loss against the 2019 income and then can use another $ NOL from 2020 may be carried forward indefinitely, to use against 80% of future taxable income

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts