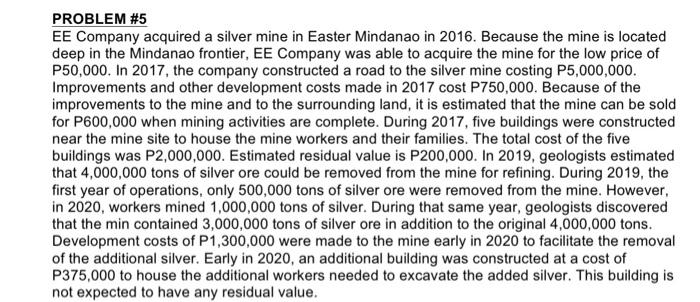

Question: PROBLEM #5 EE Company acquired a silver mine in Easter Mindanao in 2016. Because the mine is located deep in the Mindanao frontier, EE Company

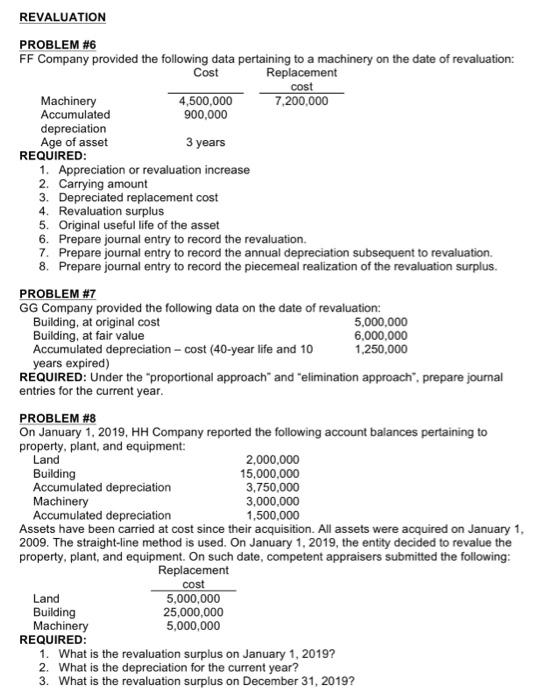

PROBLEM #5 EE Company acquired a silver mine in Easter Mindanao in 2016. Because the mine is located deep in the Mindanao frontier, EE Company was able to acquire the mine for the low price of P50,000. In 2017, the company constructed a road to the silver mine costing P5,000,000. Improvements and other development costs made in 2017 cost P750,000. Because of the improvements to the mine and to the surrounding land, it is estimated that the mine can be sold for P600,000 when mining activities are complete. During 2017, five buildings were constructed near the mine site to house the mine workers and their families. The total cost of the five buildings was P2,000,000. Estimated residual value is P200,000. In 2019, geologists estimated that 4,000,000 tons of silver ore could be removed from the mine for refining. During 2019, the first year of operations, only 500,000 tons of silver ore were removed from the mine. However, in 2020, workers mined 1,000,000 tons of silver. During that same year, geologists discovered that the min contained 3,000,000 tons of silver ore in addition to the original 4,000,000 tons. Development costs of P1,300,000 were made to the mine early in 2020 to facilitate the removal of the additional silver. Early in 2020, an additional building was constructed at a cost of P375,000 to house the additional workers needed to excavate the added silver. This building is not expected to have any residual value. REQUIRED: 1. Compute for the depletion expense for the year ending 2019 and 2020. 2. Compute for the depreciation expense for the year ending 2019 and 2020. 3. Assuming that on 2021, the company decided to shutdown its mining operations. a. Compute for the carrying amount of the wasting asset as of December 31, 2021. b. Compute for the depreciation expense of the buildings for the year 2021, assuming that the useful lives of the buildings are 5 years and 2 years, respectively REVALUATION PROBLEM #6 FF Company provided the following data pertaining to a machinery on the date of revaluation: Cost Replacement cost Machinery 4,500,000 7,200,000 Accumulated 900,000 depreciation Age of asset 3 years REQUIRED: 1. Appreciation or revaluation increase 2. Carrying amount 3. Depreciated replacement cost 4. Revaluation surplus 5. Original useful life of the asset 6. Prepare journal entry to record the revaluation 7. Prepare journal entry to record the annual depreciation subsequent to revaluation 8. Prepare journal entry to record the piecemeal realization of the revaluation surplus. PROBLEM #7 GG Company provided the following data on the date of revaluation: Building, at original cost 5.000.000 Building, at fair value 6.000.000 Accumulated depreciation - cost (40-year life and 10 1,250,000 years expired) REQUIRED: Under the "proportional approach" and "elimination approach", prepare journal entries for the current year. PROBLEM #8 On January 1, 2019, HH Company reported the following account balances pertaining to property, plant, and equipment: Land 2,000,000 Building 15,000,000 Accumulated depreciation 3,750,000 Machinery 3,000,000 Accumulated depreciation 1,500,000 Assets have been carried at cost since their acquisition. All assets were acquired on January 1, 2009. The straight-line method is used. On January 1, 2019, the entity decided to revalue the property, plant, and equipment. On such date, competent appraisers submitted the following: Replacement cost Land 5,000,000 Building 25,000,000 Machinery 5,000,000 REQUIRED: 1. What is the revaluation surplus on January 1, 2019? 2. What is the depreciation for the current year? 3. What is the revaluation surplus on December 31, 2019? PROBLEM #5 EE Company acquired a silver mine in Easter Mindanao in 2016. Because the mine is located deep in the Mindanao frontier, EE Company was able to acquire the mine for the low price of P50,000. In 2017, the company constructed a road to the silver mine costing P5,000,000. Improvements and other development costs made in 2017 cost P750,000. Because of the improvements to the mine and to the surrounding land, it is estimated that the mine can be sold for P600,000 when mining activities are complete. During 2017, five buildings were constructed near the mine site to house the mine workers and their families. The total cost of the five buildings was P2,000,000. Estimated residual value is P200,000. In 2019, geologists estimated that 4,000,000 tons of silver ore could be removed from the mine for refining. During 2019, the first year of operations, only 500,000 tons of silver ore were removed from the mine. However, in 2020, workers mined 1,000,000 tons of silver. During that same year, geologists discovered that the min contained 3,000,000 tons of silver ore in addition to the original 4,000,000 tons. Development costs of P1,300,000 were made to the mine early in 2020 to facilitate the removal of the additional silver. Early in 2020, an additional building was constructed at a cost of P375,000 to house the additional workers needed to excavate the added silver. This building is not expected to have any residual value. REQUIRED: 1. Compute for the depletion expense for the year ending 2019 and 2020. 2. Compute for the depreciation expense for the year ending 2019 and 2020. 3. Assuming that on 2021, the company decided to shutdown its mining operations. a. Compute for the carrying amount of the wasting asset as of December 31, 2021. b. Compute for the depreciation expense of the buildings for the year 2021, assuming that the useful lives of the buildings are 5 years and 2 years, respectively REVALUATION PROBLEM #6 FF Company provided the following data pertaining to a machinery on the date of revaluation: Cost Replacement cost Machinery 4,500,000 7,200,000 Accumulated 900,000 depreciation Age of asset 3 years REQUIRED: 1. Appreciation or revaluation increase 2. Carrying amount 3. Depreciated replacement cost 4. Revaluation surplus 5. Original useful life of the asset 6. Prepare journal entry to record the revaluation 7. Prepare journal entry to record the annual depreciation subsequent to revaluation 8. Prepare journal entry to record the piecemeal realization of the revaluation surplus. PROBLEM #7 GG Company provided the following data on the date of revaluation: Building, at original cost 5.000.000 Building, at fair value 6.000.000 Accumulated depreciation - cost (40-year life and 10 1,250,000 years expired) REQUIRED: Under the "proportional approach" and "elimination approach", prepare journal entries for the current year. PROBLEM #8 On January 1, 2019, HH Company reported the following account balances pertaining to property, plant, and equipment: Land 2,000,000 Building 15,000,000 Accumulated depreciation 3,750,000 Machinery 3,000,000 Accumulated depreciation 1,500,000 Assets have been carried at cost since their acquisition. All assets were acquired on January 1, 2009. The straight-line method is used. On January 1, 2019, the entity decided to revalue the property, plant, and equipment. On such date, competent appraisers submitted the following: Replacement cost Land 5,000,000 Building 25,000,000 Machinery 5,000,000 REQUIRED: 1. What is the revaluation surplus on January 1, 2019? 2. What is the depreciation for the current year? 3. What is the revaluation surplus on December 31, 2019

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts