Question: Problem 5-09 The table below shows data on the returns over five 1-year periods for seven mutual funds. A firm's portfolio managers will assume that

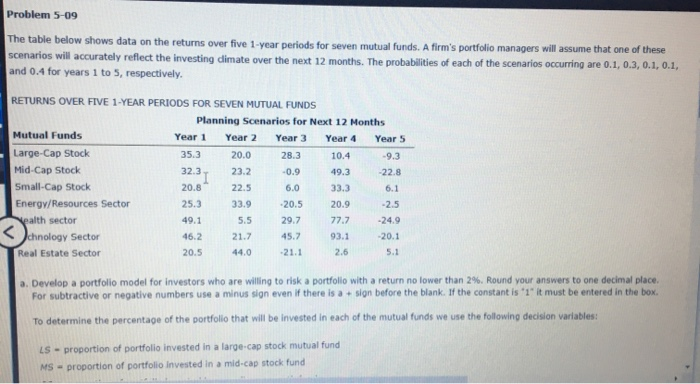

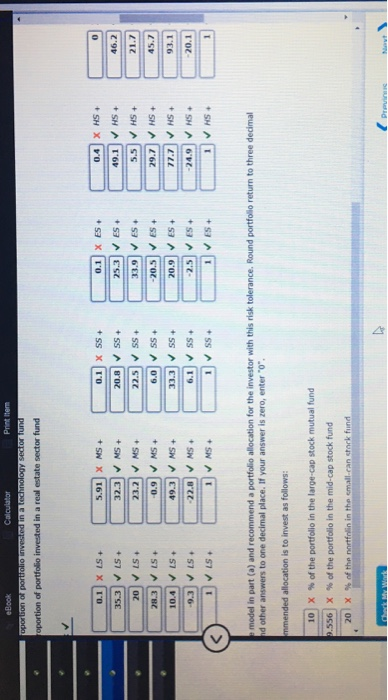

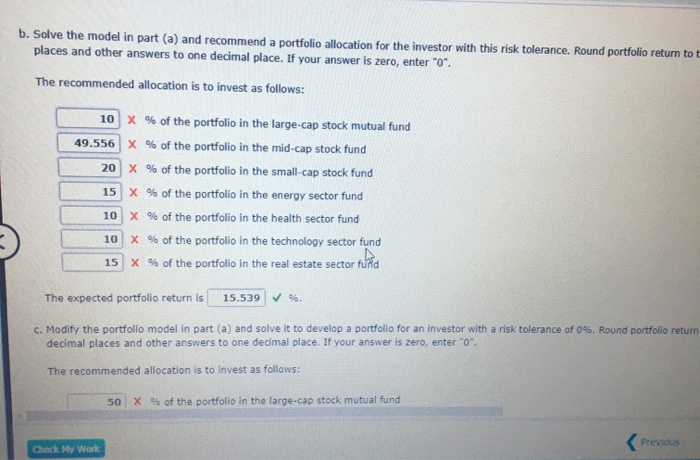

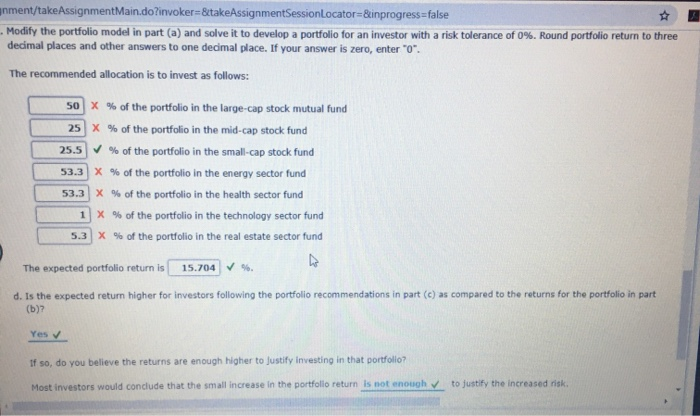

Problem 5-09 The table below shows data on the returns over five 1-year periods for seven mutual funds. A firm's portfolio managers will assume that one of these scenarios will accurately reflect the investing dimate over the next 12 months. The probabilities of each of the scenarios occurring are 0.1, 0.3, 0.1, 0.1, and 0.4 for years 1 to 5, respectively. 93 228 32.3 RETURNS OVER FIVE 1-YEAR PERIODS FOR SEVEN MUTUAL FUNDS Planning Scenarios for Next 12 Months Mutual Funds Year 1 Year 2 Year 3 Year 4 Year 5 Large-Cap Stock 35.3 20.0 28.3 Mid-Cap Stock 23.2 Small-Cap Stock 20.8 22.5 Energy/Resources Sector 25.3 33.9 Nealth sector 49.1 5.5 -24.9 32.3 0.1 20.8 22.5 23.2 > > 333 > MS > 6.1 MS + model in part (a) and recommend a portfolio allocation for the investor with this risk tolerance. Round portfolio return to three decimal nd other answers to one decimal place. If your answer is zero, enter"0". mmended allocation is to invest as follows: 10 2.556 X % of the portfolio in the large-cap stock mutual fund X % of the portfolio in the mid-cap stock fund 20x of the nortfolin in the small can stack fund De b. Solve the model in part (a) and recommend a portfolio allocation for the investor with this risk tolerance. Round portfolio return to places and other answers to one decimal place. If your answer is zero, enter "0". The recommended allocation is to invest as follows: 10 49.556 20 15 10 10 15 X % of the portfolio in the large-cap stock mutual fund X % of the portfolio in the mid-cap stock fund X % of the portfolio in the small-cap stock fund X % of the portfolio in the energy sector fund X % of the portfolio in the health sector fund X % of the portfolio in the technology sector fund X % of the portfolio in the real estate sector fund The expected portfolio return is 15.539 %. c. Modify the portfolio model in part (a) and solve it to develop a portfolio for an investor with a risk tolerance of 0%. Round portfolio return decimal places and other answers to one decimal place. If your answer is zero, enter"0". The recommended allocation is to invest as follows: 50 X of the portfolio in the large-cap stock mutual fund Previous MyW nment/take AssignmentMain.do?invoker=&takeAssignmentSessionLocator=&inprogress=false - Modify the portfolio model in part (a) and solve it to develop a portfolio for an investor with a risk tolerance of 0%. Round portfolio return to three decimal places and other answers to one decimal place. If your answer is zero, enter"0" The recommended allocation is to invest as follows: so X % of the portfolio in the large-cap stock mutual fund 25 X % of the portfolio in the mid-cap stock fund 25.5 % of the portfolio in the small-cap stock fund 53.3 X % of the portfolio in the energy sector fund 53.3 X % of the portfolio in the health sector fund 1 X % of the portfolio in the technology sector fund 5.3 X % of the portfolio in the real estate sector fund The expected portfolio return is 15.704 S. d. Is the expected return higher for investors following the portfolio recommendations in part (c) as compared to the returns for the portfolio in part (b)? Yes & If so, do you believe the returns are enough higher to justify Investing in that portfolio? Most investors would conclude that the small increase in the portfolio return is not enough to justify the increased risk. Problem 5-09 The table below shows data on the returns over five 1-year periods for seven mutual funds. A firm's portfolio managers will assume that one of these scenarios will accurately reflect the investing dimate over the next 12 months. The probabilities of each of the scenarios occurring are 0.1, 0.3, 0.1, 0.1, and 0.4 for years 1 to 5, respectively. 93 228 32.3 RETURNS OVER FIVE 1-YEAR PERIODS FOR SEVEN MUTUAL FUNDS Planning Scenarios for Next 12 Months Mutual Funds Year 1 Year 2 Year 3 Year 4 Year 5 Large-Cap Stock 35.3 20.0 28.3 Mid-Cap Stock 23.2 Small-Cap Stock 20.8 22.5 Energy/Resources Sector 25.3 33.9 Nealth sector 49.1 5.5 -24.9 32.3 0.1 20.8 22.5 23.2 > > 333 > MS > 6.1 MS + model in part (a) and recommend a portfolio allocation for the investor with this risk tolerance. Round portfolio return to three decimal nd other answers to one decimal place. If your answer is zero, enter"0". mmended allocation is to invest as follows: 10 2.556 X % of the portfolio in the large-cap stock mutual fund X % of the portfolio in the mid-cap stock fund 20x of the nortfolin in the small can stack fund De b. Solve the model in part (a) and recommend a portfolio allocation for the investor with this risk tolerance. Round portfolio return to places and other answers to one decimal place. If your answer is zero, enter "0". The recommended allocation is to invest as follows: 10 49.556 20 15 10 10 15 X % of the portfolio in the large-cap stock mutual fund X % of the portfolio in the mid-cap stock fund X % of the portfolio in the small-cap stock fund X % of the portfolio in the energy sector fund X % of the portfolio in the health sector fund X % of the portfolio in the technology sector fund X % of the portfolio in the real estate sector fund The expected portfolio return is 15.539 %. c. Modify the portfolio model in part (a) and solve it to develop a portfolio for an investor with a risk tolerance of 0%. Round portfolio return decimal places and other answers to one decimal place. If your answer is zero, enter"0". The recommended allocation is to invest as follows: 50 X of the portfolio in the large-cap stock mutual fund Previous MyW nment/take AssignmentMain.do?invoker=&takeAssignmentSessionLocator=&inprogress=false - Modify the portfolio model in part (a) and solve it to develop a portfolio for an investor with a risk tolerance of 0%. Round portfolio return to three decimal places and other answers to one decimal place. If your answer is zero, enter"0" The recommended allocation is to invest as follows: so X % of the portfolio in the large-cap stock mutual fund 25 X % of the portfolio in the mid-cap stock fund 25.5 % of the portfolio in the small-cap stock fund 53.3 X % of the portfolio in the energy sector fund 53.3 X % of the portfolio in the health sector fund 1 X % of the portfolio in the technology sector fund 5.3 X % of the portfolio in the real estate sector fund The expected portfolio return is 15.704 S. d. Is the expected return higher for investors following the portfolio recommendations in part (c) as compared to the returns for the portfolio in part (b)? Yes & If so, do you believe the returns are enough higher to justify Investing in that portfolio? Most investors would conclude that the small increase in the portfolio return is not enough to justify the increased risk

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts