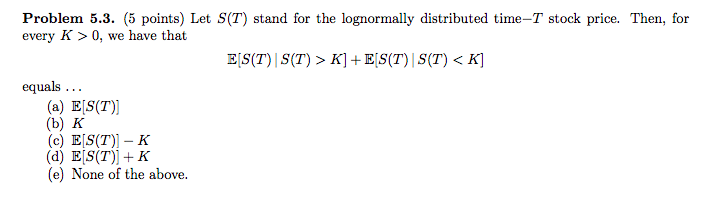

Question: Problem 5.3. (5 points) Let S(T) stand for the lognormally distributed time-T stock price. Then, for every K>0, we have that equals (a) E[S(T)] (b)

Problem 5.3. (5 points) Let S(T) stand for the lognormally distributed time-T stock price. Then, for every K>0, we have that equals (a) E[S(T)] (b) K (c) E[S(T)]-K (d) E[S(T) K (e) None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock