Question: Problem 8 (2 points): Both ABC and XYZ want to borrow $1,000,000 for 10 years. ABC wants to borrow at a floating interest rate while

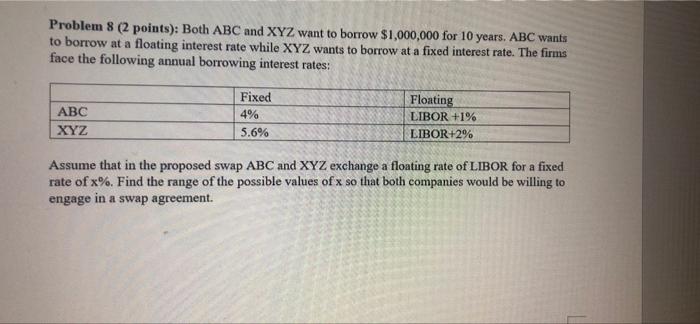

Problem 8 (2 points): Both ABC and XYZ want to borrow $1,000,000 for 10 years. ABC wants to borrow at a floating interest rate while XYZ wants to borrow at a fixed interest rate. The firms face the following annual borrowing interest rates: ABC XYZ Fixed 4% 5.6% Floating LIBOR +1% LIBOR +2% Assume that in the proposed swap ABC and XYZ exchange a floating rate of LIBOR for a fixed rate of x%. Find the range of the possible values of x so that both companies would be willing to engage in a swap agreement

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock