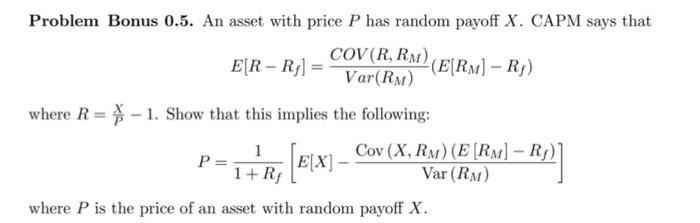

Question: Problem Bonus 0.5. An asset with price P has random payoff X. CAPM says that E[RRf]=Var(RM)COV(R,RM)(E[RM]Rf) where R=PX1. Show that this implies the following: P=1+Rf1[E[X]Var(RM)Cov(X,RM)(E[RM]Rf)]

Problem Bonus 0.5. An asset with price P has random payoff X. CAPM says that E[RRf]=Var(RM)COV(R,RM)(E[RM]Rf) where R=PX1. Show that this implies the following: P=1+Rf1[E[X]Var(RM)Cov(X,RM)(E[RM]Rf)] where P is the price of an asset with random payoff X

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock