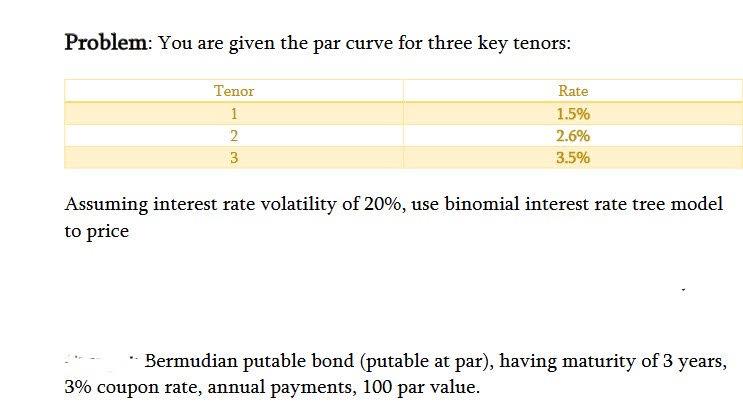

Question: Problem: You are given the par curve for three key tenors: Assuming interest rate volatility of 20%, use binomial interest rate tree model to price

Problem: You are given the par curve for three key tenors: Assuming interest rate volatility of 20%, use binomial interest rate tree model to price - Bermudian putable bond (putable at par), having maturity of 3 years, 3% coupon rate, annual payments, 100 par value

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock