Question: Problem#7 Using the binominal model value three-year European put option with the periodically computed one-year interest rate as the underlying. Assume the notional amount of

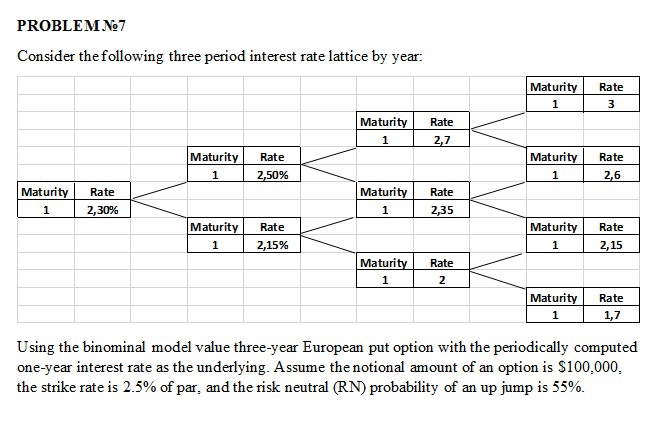

Problem#7

Using the binominal model value three-year European put option with the periodically computed one-year interest rate as the underlying. Assume the notional amount of an option is $100,000, the strike rate is 2.5% of par, and the risk neutral (RN) probability of an up jump is 55%.

PROBLEMN.7 Consider the following three period interest rate lattice by year: 1 3 Maturity Rate 12,7 Maturity Rate 2,50% Maturity Rate 12,6 Maturity Maturity Rate 2,30% Rate 2,35 1 Maturity 1 2 Rate ,15% Maturity 1 Rate 2,15 Maturity 1 | Rate 2 Maturity Rate 11,7 Using the binominal model value three-year European put option with the periodically computed one-year interest rate as the underlying. Assume the notional amount of an option is $100,000, the strike rate is 2.5% of par, and the risk neutral (RN) probability of an up jump is 55%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock