Question: provide correct option for the every MCQ without explanation don't give me just 1 answer 1.8. Which of the following statements apply to feed-forward control?

provide correct option for the every MCQ without explanation don't give me just 1 answer

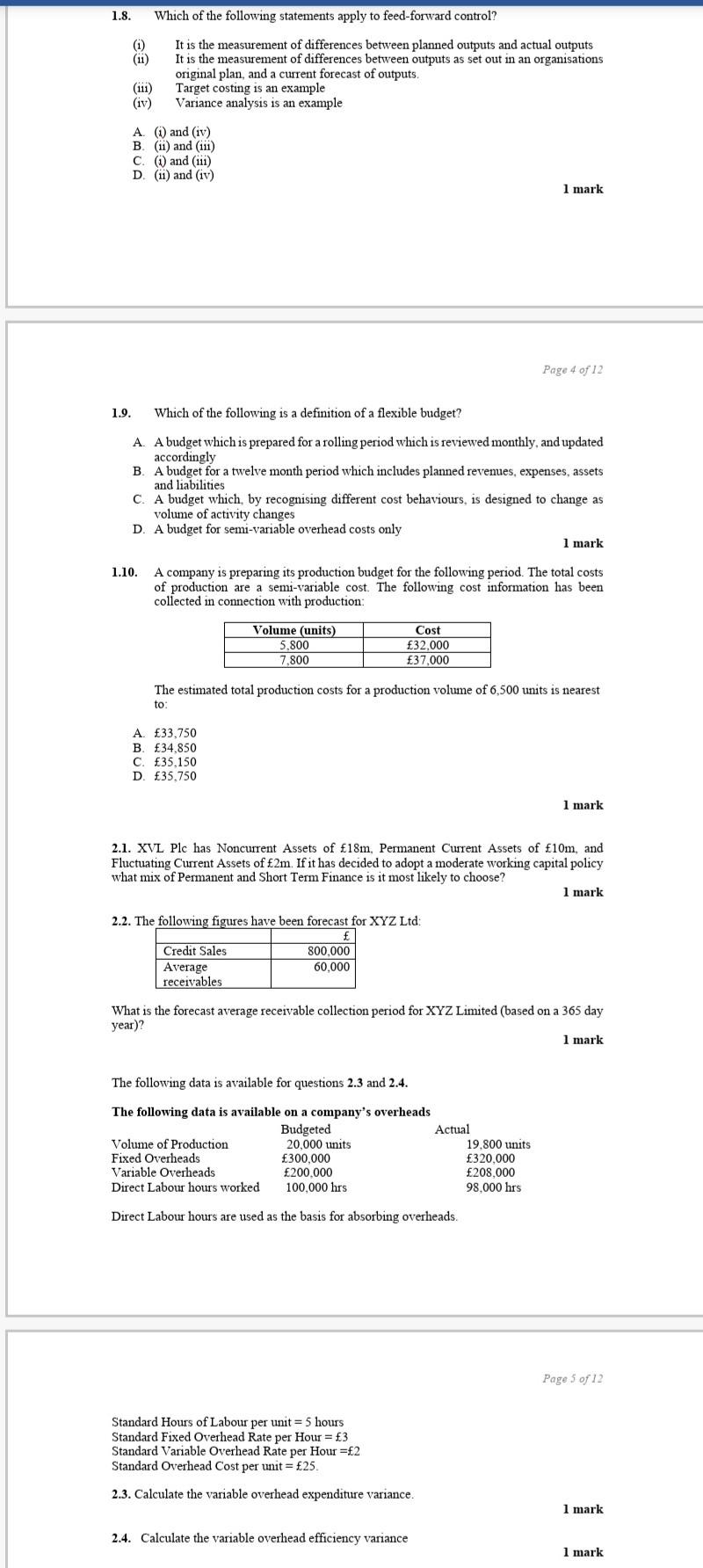

1.8. Which of the following statements apply to feed-forward control? (1) (ii) It is the measurement of differences between planned outputs and actual outputs It is the measurement of differences between outputs as set out in an organisations original plan, and a current forecast of outputs. Target costing is an example Variance analysis is an example (111) (iv) A () and (iv) B. (ii) and (iii) c. ) and (111) D. (i) and (iv) I mark Page 4 of 12 1.9. Which of the following is a definition of a flexible budget? A. A budget which is prepared for a rolling period which is reviewed monthly, and updated accordingly B. A budget for a twelve month period which includes planned revenues, expenses, assets and liabilities C. A budget which, by recognising different cost behaviours, is designed to change as volume of activity changes D. A budget for semi-variable overhead costs only 1 mark 1.10. A company is preparing its production budget for the following period. The total costs of production are a semi-variable cost. The following cost information has been collected in connection with production: Volume (units) 5.800 7,800 Cost 32.000 37,000 The estimated total production costs for a production volume of 6,500 units is nearest to A 33,750 B. 34,850 C. 35,150 D. 35,750 1 mark 2.1. XVL Plc has Noncurrent Assets of 18m, Permanent Current Assets of 10m, and Fluctuating Current Assets of 2m. If it has decided to adopt a moderate working capital policy what mix of Permanent and Short Term Finance is it most likely to choose? I mark 2.2. The following figures have been forecast for XYZ Ltd: Credit Sales Average receivables 800,000 60.000 What is the forecast average receivable collection period for XYZ Limited (based on a 365 day year)? 1 mark The following data is available for questions 2.3 and 2.4. The following data is available on a company's overheads Budgeted Actual Volume of Production 20.000 units 19.800 units Fixed Overheads 300,000 320.000 Variable Overheads 200,000 208.000 Direct Labour hours worked 100.000 hrs 98.000 hrs Direct Labour hours are used as the basis for absorbing overheads Page 5 of 12 Standard Hours of Labour per unit = 5 hours Standard Fixed Overhead Rate per Hour = 3 Standard Variable Overhead Rate per Hour = 2 Standard Overhead Cost per unit = 25. 2.3. Calculate the variable overhead expenditure variance. 1 mark 2.4. Calculate the variable overhead efficiency variance 1 mark

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts