Question: provide introduction, background, analysis, executive summary , main issues, assumptions, SWOT analysis, alternatives and recommendations and conclusion CASE Municipality of Freestone Amanda Pospect, a member

provide introduction, background, analysis, executive summary , main issues, assumptions, SWOT analysis, alternatives and recommendations and conclusion

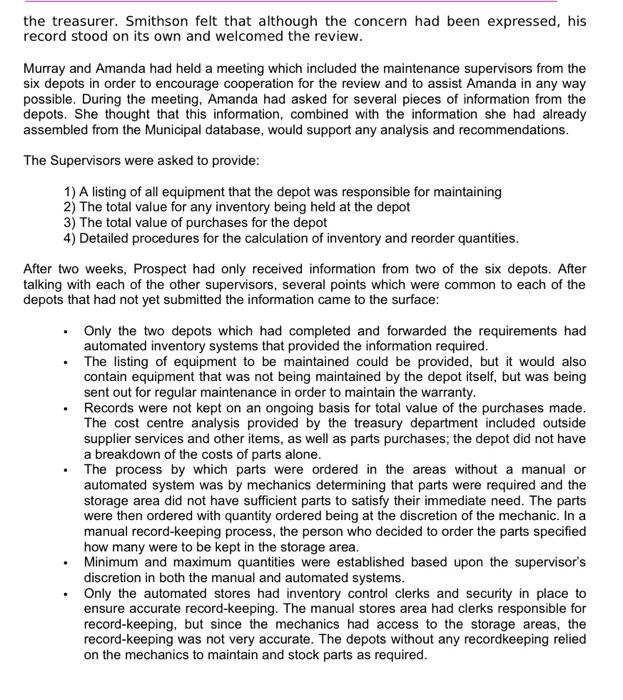

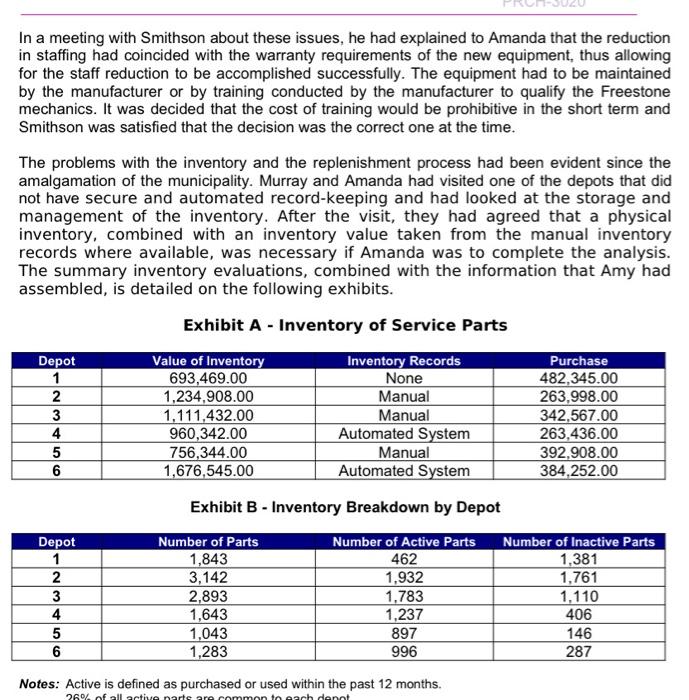

CASE Municipality of Freestone Amanda Pospect, a member of the Municipality of Freestone (also referred to as City of Freestone) Treasury Department, was in the process of reviewing the practices of the Maintenance Department. She needed to be sure that she had all of the information necessary in order to provide a comprehensive report and sound recommendations to the Municipal Treasurer. Municipality of Freestone - Maintenance Department (FMD) FMD had established six service depots in various regional sites in order to support the multitude of equipment used by the municipality. These depots were originally sites within the six townships which had been forced by regionalization to merge into one municipal entity 5 years ago. Many of the operations had been combined just for the sake of getting the departments under one roof. During the past 5 years, several types of equipment had been standardized in order to minimize the number of parts and storage required, while also making sure the equipment was maintained to established standards. The merged Maintenance Department had experienced less downtime of equipment in the last two years, while at the same time retiring the old non standard equipment and reducing by 14 percent the number of employees who maintained the equipment. Most of the reductions in employees had been through retirement, coinciding with the older equipment being replaced. Murray Smithson, the manager of the department, had been given public recognition for the work that had been done to improve the efficiency of the department. However, the Municipal Treasurer had recently voiced concerns over the cost of capital acquisitions, which was in excess of $13 million that had been used to upgrade the department's fleet. He was also concerned about the high spending costs associated with the parts required to maintain the inventory, this was now running at approximately $2.5 million per year, an increase of 20% over previous spending averages for the past two years. The Treasurer also knew that inventory was being kept at each location and that inventory carrying costs had been calculated at 25% per year. Prospect had been assigned the task of determining whether this money was being spent wisely and if the expense was warranted; she was also to investigate the maintenance department's spending and inventory processes and issue a report to the treasurer. Smithson felt that although the concern had been expressed, his record stood on its own and welcomed the review. Murray and Amanda had held a meeting which included the maintenance supervisors from the six depots in order to encourage cooperation for the review and to assist Amanda in any way possible. During the meeting, Amanda had asked for several pieces of information from the depots. She thought that this information, combined with the information she had already assembled from the Municipal database, would support any analysis and recommendations. The Supervisors were asked to provide: 1) A listing of all equipment that the depot was responsible for maintaining 2) The total value for any inventory being held at the depot 3) The total value of purchases for the depot 4) Detailed procedures for the calculation of inventory and reorder quantities. After two weeks, Prospect had only received information from two of the six depots. After talking with each of the other supervisors, several points which were common to each of the depots that had not yet submitted the information came to the surface: . Only the two depots which had completed and forwarded the requirements had automated inventory systems that provided the information required. The listing of equipment to be maintained could be provided, but it would also contain equipment that was not being maintained by the depot itself, but was being sent out for regular maintenance in order to maintain the warranty. Records were not kept on an ongoing basis for total value of the purchases made. The cost centre analysis provided by the treasury department included outside supplier services and other items, as well as parts purchases; the depot did not have a breakdown of the costs of parts alone. The process by which parts were ordered in the areas without a manual or automated system was by mechanics determining that parts were required and the storage area did not have sufficient parts to satisfy their immediate need. The parts were then ordered with quantity ordered being at the discretion of the mechanic. In a manual record-keeping process, the person who decided to order the parts specified how many were to be kept in the storage area. Minimum and maximum quantities were established based upon the supervisor's discretion in both the manual and automated systems. . Only the automated stores had inventory control clerks and security in place to ensure accurate record-keeping. The manual stores area had clerks responsible for record-keeping, but since the mechanics had access to the storage areas, the record-keeping was not very accurate. The depots without any recordkeeping relied on the mechanics to maintain and stock parts as required. In a meeting with Smithson about these issues, he had explained to Amanda that the reduction in staffing had coincided with the warranty requirements of the new equipment, thus allowing for the staff reduction to be accomplished successfully. The equipment had to be maintained by the manufacturer or by training conducted by the manufacturer to qualify the Freestone mechanics. It was decided that the cost of training would be prohibitive in the short term and Smithson was satisfied that the decision was the correct one at the time. The problems with the inventory and the replenishment process had been evident since the amalgamation of the municipality. Murray and Amanda had visited one of the depots that did not have secure and automated record-keeping and had looked at the storage and management of the inventory. After the visit, they had agreed that a physical inventory, combined with an inventory value taken from the manual inventory records where available, was necessary if Amanda was to complete the analysis. The summary inventory evaluations, combined with the information that Amy had assembled, is detailed on the following exhibits. Exhibit A - Inventory of Service Parts Depot Value of Inventory Inventory Records Purchase 1 693,469.00 None 482,345.00 2 1,234,908.00 Manual 263,998.00 3 1,111,432.00 Manual 342,567.00 4 960,342.00 Automated System 263,436.00 5 756,344.00 Manual 392,908.00 6 1,676,545.00 Automated System 384,252.00 Exhibit B - Inventory Breakdown by Depot olun - Depot 1 2 3 4 5 6 Number of Parts 1,843 3,142 2,893 1,643 1,043 1,283 Number of Active Parts 462 1,932 1.783 1,237 897 996 Number of Inactive Parts 1,381 1,761 1,110 406 146 287 Notes: Active is defined as purchased or used within the past 12 months. 260% of all active parte are common to each denot Exhibit C-DEPOT 4 Inventory Parts Breakdown - Summary of Findings Accumulated Number of Accumulated Accumulated Stock Keeping Units Total Annual Percent of Purchases Purchases Page 3 of 5 Public Sector Supply Chain PRCH-3020 Management 25 50 75 100 125 150 175 700 14,237.00 23,432.00 30,781.00 36,490.00 41,235.00 46,666.00 51,245.00 244,086.00 5.40 8.90 11.70 13.90 15.60 17.70 19.40 100.00 Jotes: The summary analysis of Stock Keeping Units for Depot 4 was representative of Depot 6 and representative of a manual analysis completed on Depot 2. All Depot Storage Facilities had many interactive parts that were mostly obsolete due to the updating of the equipment and standardization that took place Exhibit D - Map Area 1 Area 2 Area 3 Area 6 Area 5 Area 4 CASE Municipality of Freestone Amanda Pospect, a member of the Municipality of Freestone (also referred to as City of Freestone) Treasury Department, was in the process of reviewing the practices of the Maintenance Department. She needed to be sure that she had all of the information necessary in order to provide a comprehensive report and sound recommendations to the Municipal Treasurer. Municipality of Freestone - Maintenance Department (FMD) FMD had established six service depots in various regional sites in order to support the multitude of equipment used by the municipality. These depots were originally sites within the six townships which had been forced by regionalization to merge into one municipal entity 5 years ago. Many of the operations had been combined just for the sake of getting the departments under one roof. During the past 5 years, several types of equipment had been standardized in order to minimize the number of parts and storage required, while also making sure the equipment was maintained to established standards. The merged Maintenance Department had experienced less downtime of equipment in the last two years, while at the same time retiring the old non standard equipment and reducing by 14 percent the number of employees who maintained the equipment. Most of the reductions in employees had been through retirement, coinciding with the older equipment being replaced. Murray Smithson, the manager of the department, had been given public recognition for the work that had been done to improve the efficiency of the department. However, the Municipal Treasurer had recently voiced concerns over the cost of capital acquisitions, which was in excess of $13 million that had been used to upgrade the department's fleet. He was also concerned about the high spending costs associated with the parts required to maintain the inventory, this was now running at approximately $2.5 million per year, an increase of 20% over previous spending averages for the past two years. The Treasurer also knew that inventory was being kept at each location and that inventory carrying costs had been calculated at 25% per year. Prospect had been assigned the task of determining whether this money was being spent wisely and if the expense was warranted; she was also to investigate the maintenance department's spending and inventory processes and issue a report to the treasurer. Smithson felt that although the concern had been expressed, his record stood on its own and welcomed the review. Murray and Amanda had held a meeting which included the maintenance supervisors from the six depots in order to encourage cooperation for the review and to assist Amanda in any way possible. During the meeting, Amanda had asked for several pieces of information from the depots. She thought that this information, combined with the information she had already assembled from the Municipal database, would support any analysis and recommendations. The Supervisors were asked to provide: 1) A listing of all equipment that the depot was responsible for maintaining 2) The total value for any inventory being held at the depot 3) The total value of purchases for the depot 4) Detailed procedures for the calculation of inventory and reorder quantities. After two weeks, Prospect had only received information from two of the six depots. After talking with each of the other supervisors, several points which were common to each of the depots that had not yet submitted the information came to the surface: . Only the two depots which had completed and forwarded the requirements had automated inventory systems that provided the information required. The listing of equipment to be maintained could be provided, but it would also contain equipment that was not being maintained by the depot itself, but was being sent out for regular maintenance in order to maintain the warranty. Records were not kept on an ongoing basis for total value of the purchases made. The cost centre analysis provided by the treasury department included outside supplier services and other items, as well as parts purchases; the depot did not have a breakdown of the costs of parts alone. The process by which parts were ordered in the areas without a manual or automated system was by mechanics determining that parts were required and the storage area did not have sufficient parts to satisfy their immediate need. The parts were then ordered with quantity ordered being at the discretion of the mechanic. In a manual record-keeping process, the person who decided to order the parts specified how many were to be kept in the storage area. Minimum and maximum quantities were established based upon the supervisor's discretion in both the manual and automated systems. . Only the automated stores had inventory control clerks and security in place to ensure accurate record-keeping. The manual stores area had clerks responsible for record-keeping, but since the mechanics had access to the storage areas, the record-keeping was not very accurate. The depots without any recordkeeping relied on the mechanics to maintain and stock parts as required. In a meeting with Smithson about these issues, he had explained to Amanda that the reduction in staffing had coincided with the warranty requirements of the new equipment, thus allowing for the staff reduction to be accomplished successfully. The equipment had to be maintained by the manufacturer or by training conducted by the manufacturer to qualify the Freestone mechanics. It was decided that the cost of training would be prohibitive in the short term and Smithson was satisfied that the decision was the correct one at the time. The problems with the inventory and the replenishment process had been evident since the amalgamation of the municipality. Murray and Amanda had visited one of the depots that did not have secure and automated record-keeping and had looked at the storage and management of the inventory. After the visit, they had agreed that a physical inventory, combined with an inventory value taken from the manual inventory records where available, was necessary if Amanda was to complete the analysis. The summary inventory evaluations, combined with the information that Amy had assembled, is detailed on the following exhibits. Exhibit A - Inventory of Service Parts Depot Value of Inventory Inventory Records Purchase 1 693,469.00 None 482,345.00 2 1,234,908.00 Manual 263,998.00 3 1,111,432.00 Manual 342,567.00 4 960,342.00 Automated System 263,436.00 5 756,344.00 Manual 392,908.00 6 1,676,545.00 Automated System 384,252.00 Exhibit B - Inventory Breakdown by Depot olun - Depot 1 2 3 4 5 6 Number of Parts 1,843 3,142 2,893 1,643 1,043 1,283 Number of Active Parts 462 1,932 1.783 1,237 897 996 Number of Inactive Parts 1,381 1,761 1,110 406 146 287 Notes: Active is defined as purchased or used within the past 12 months. 260% of all active parte are common to each denot Exhibit C-DEPOT 4 Inventory Parts Breakdown - Summary of Findings Accumulated Number of Accumulated Accumulated Stock Keeping Units Total Annual Percent of Purchases Purchases Page 3 of 5 Public Sector Supply Chain PRCH-3020 Management 25 50 75 100 125 150 175 700 14,237.00 23,432.00 30,781.00 36,490.00 41,235.00 46,666.00 51,245.00 244,086.00 5.40 8.90 11.70 13.90 15.60 17.70 19.40 100.00 Jotes: The summary analysis of Stock Keeping Units for Depot 4 was representative of Depot 6 and representative of a manual analysis completed on Depot 2. All Depot Storage Facilities had many interactive parts that were mostly obsolete due to the updating of the equipment and standardization that took place Exhibit D - Map Area 1 Area 2 Area 3 Area 6 Area 5 Area 4 Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock