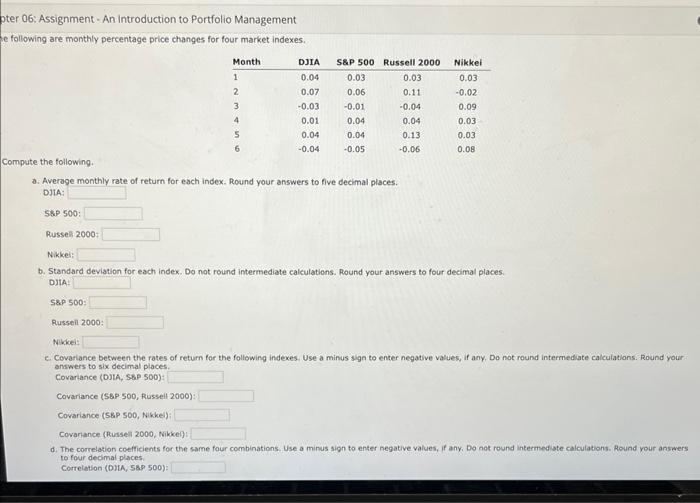

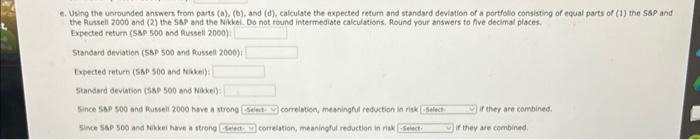

Question: pter 06: Assignment - An introduction to Portfolio Management te following are monthly percentage price changes for four market indexes. Compute the following. a. Average

pter 06: Assignment - An introduction to Portfolio Management te following are monthly percentage price changes for four market indexes. Compute the following. a. Average monthly rate of return for each index. Round your answers to five decimal places. DJIA: Ste 500: Russell 20007 Nikkei: b. Standard deviation for each index. Do not round intermediate calculations. Round your answers to four decimal places. DJtA: 5 500: Russeil 2000: Nakeis e. Covariance between the rates of return for the following indexes. Use a minus sign to enter negative values, if any, Do not round intermediate calculations. Round your answers to six decimal places. Covariance (D)tA, SBP 500): Covariance (SSP 500, Russell 2000): Covariance (5\&P 500, Nikke) : Covariance (Russell 2000, Nikkel): d. The correlation coefficients for the same four combinations. Use a minus sign to enter negative values, if any, Do not round intermed ate calculations. Round vour answers to four dedimal places. Correlation (D)tA, 589500) : e. Using the unrounded answers from parts (a), (b), and (d), calculate the expected retum and standard deviation of a portfollo consisting of equal parts of (1) the SsP and the Russell 2000 and (2) the 539 and the Nikkel. Do not round imtermediate calculations. Pound your answers to five decimal places. Expected teturn (58) 500 and Riassell 2000): Standerd deviation (58P 500 and fussell 2000) t Expected return (SNP 500 and tikkei): Standard deviation (sise 500 and Nakei): Since 5AP300 and thusell 2000 heve a strang correlatica, meaninghul reduction in riak If ther are combined. wince s4e 500 and takkei here a strong correlstion, meaningful resuction in riak

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts