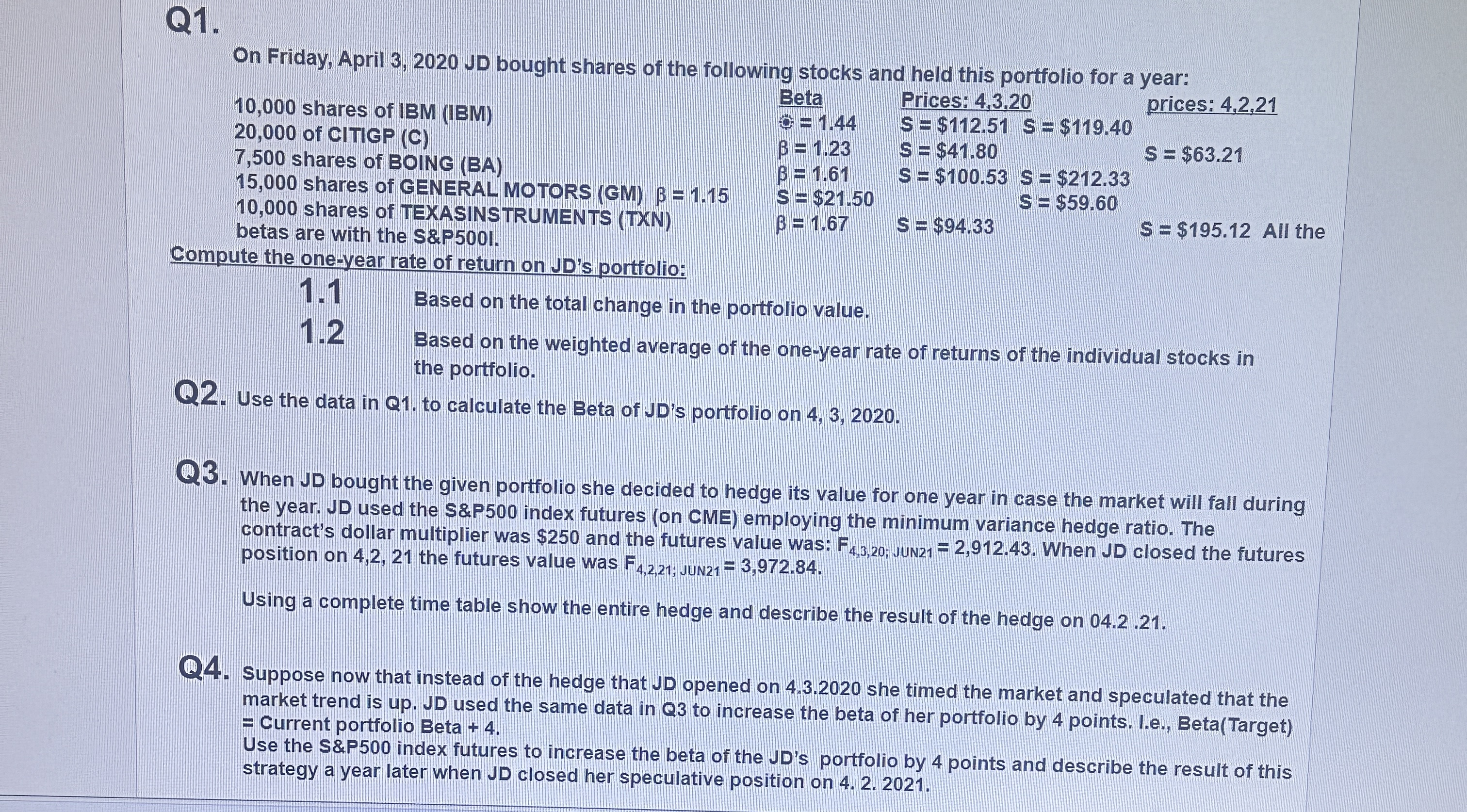

Question: Q 1 . O n Friday, April 3 , 2 0 2 0 J D bought shares o f the following stocks and held this

Friday, April bought shares the following stocks and held this portfolio for a year:

shares IBM

CITIGP

shares BOING

shares GENERAL MOTORS

shares TEXASINSTRUMENTS

betas are with the &

Compute the oneyear rate return portfolio:

Beta

$

Prices:

$$

$

$

$

$

$

prices:

$

$ All the

Based the total change the portfolio value.

Based the weighted average the oneyear rate returns the individual stocks

the portfolio.

Use the data calculate the Beta portfolio

When bought the given portfolio she decided hedge its value for one year case the market will fall during

the year. used the & index futures CME employing the minimum variance hedge ratio. The

contract's dollar multiplier was $ and the futures value was: ;unN When closed the futures

position the futures value was vuN

Using a complete time table show the entire hedge and describe the result the hedge

Suppose now that instead the hedge that opened she timed the market and speculated that the

market trend used the same data increase the beta her portfolio ANSWER QUESTION

points. I. Beta

Current portfolio Beta

Use the & index futures increase the beta the portfolio points and describe the result this

strategy a year later when closed her speculative position

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock