Question: Q 2 ( 6 0 % ) Write a Python program that solves ( a ) , ( b ) , & ( c )

Q Write a Python program that solves ab & c

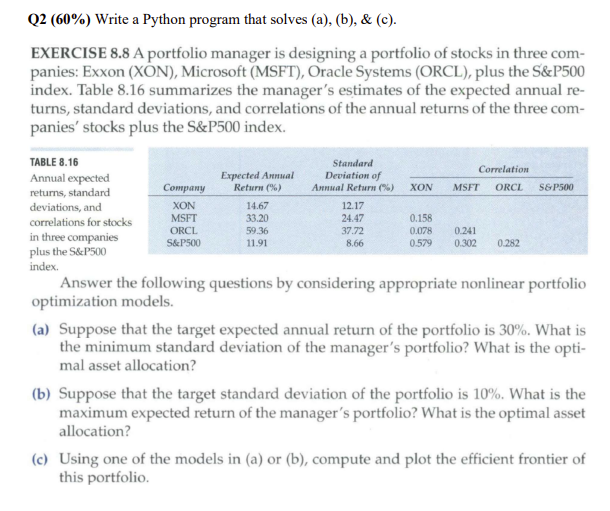

EXERCISE A portfolio manager is designing a portfolio of stocks in three com

panies: Exxon XON Microsoft MSFT Oracle Systems ORCL plus the S&P

index. Table summarizes the manager's estimates of the expected annual re

turns, standard deviations, and correlations of the annual returns of the three com

panies' stocks plus the S&P index.

TABLE

Annual expected

returns, standard

deviations, and

correlations for stocks

in three companies

plus the S&P

index.

Answer the following questions by considering appropriate nonlinear portfolio

optimization models.

a Suppose that the target expected annual return of the portfolio is What is

the minimum standard deviation of the manager's portfolio? What is the opti

mal asset allocation?

b Suppose that the target standard deviation of the portfolio is What is the

maximum expected return of the manager's portfolio? What is the optimal asset

allocation?

c Using one of the models in a or b compute and plot the efficient frontier of

this portfolio.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock