Question: Q2. Consider 3 zero coupon bond: Maturity Yld: 10 1.50%; 20 2.00%; 30 2.25% Q2a. calculate duration and convexity, dollar duration and dollar convexity

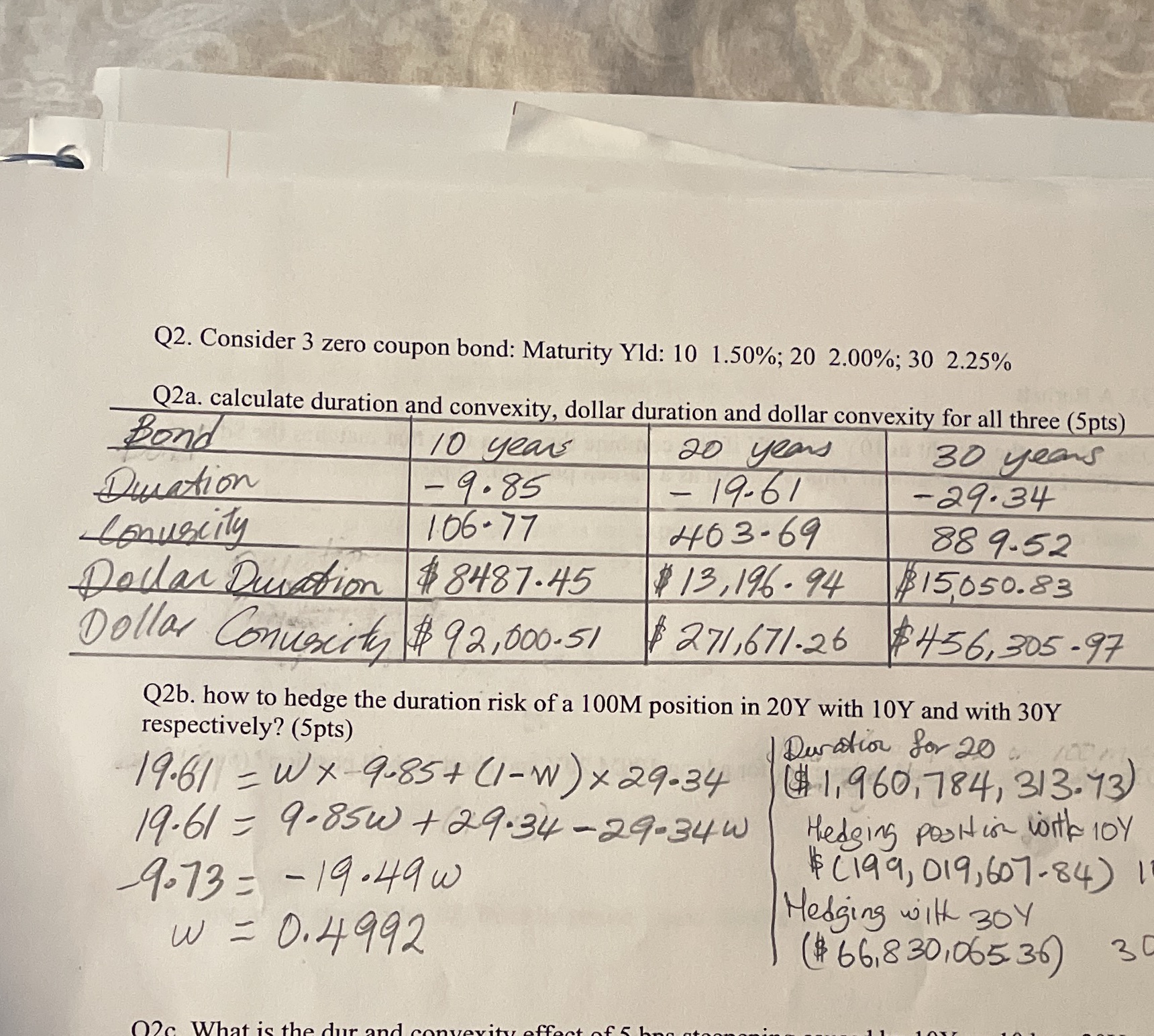

Q2. Consider 3 zero coupon bond: Maturity Yld: 10 1.50%; 20 2.00%; 30 2.25% Q2a. calculate duration and convexity, dollar duration and dollar convexity for all three (5pts) 30 years Bond Duration Conuscity 10 years -9.85 106-77 20 years - 19-61 463-69 -29.34 889-52 $13,196.94 $15,050.83 Dollar Duration $8487.45 Dollar Conuscity #92,000-51 $271,671.26 $456,305-97 Q2b. how to hedge the duration risk of a 100M position in 20Y with 10Y and with 30Y respectively? (5pts) Duration for 20 19.61=Wx-9.85+ (1-W) x 29-34 $1,960,784, 313.73) 19.61 = 9.85w+29.34-29-34W -9.73=-19.49w w = 0.4992 Hedging position with 10Y $199,019,607-84) 11 Hedging with 30Y ($66,830,06536) 30 02c What is the dur and convexity effect of 5 bes atc

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts