Question: Before beginning the assignment, take a moment to look through the papers in this module. Note in the lower left-hand corner that some documents

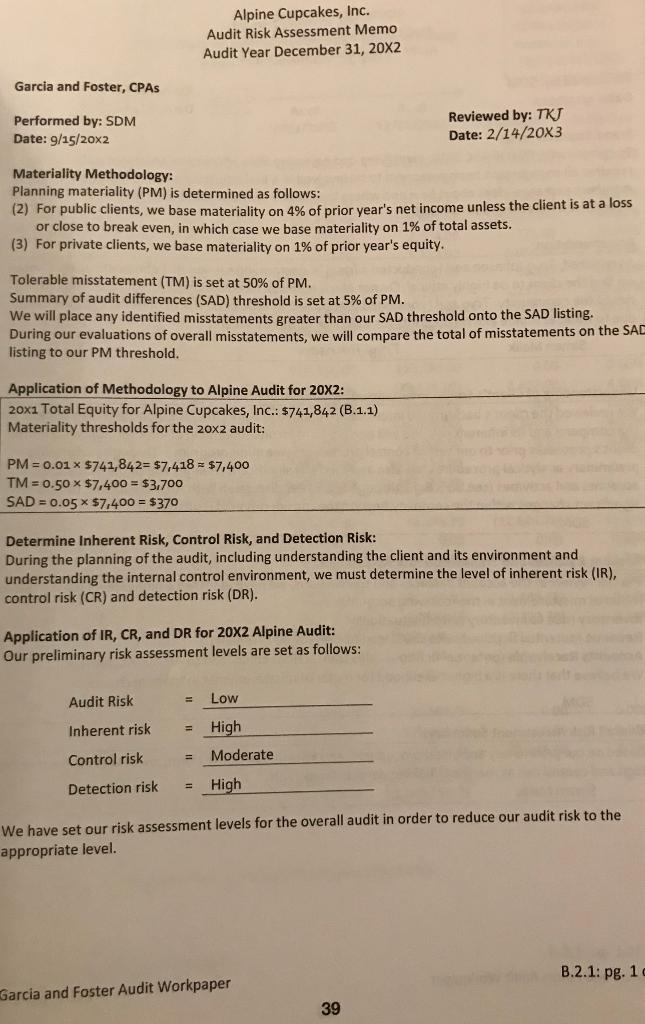

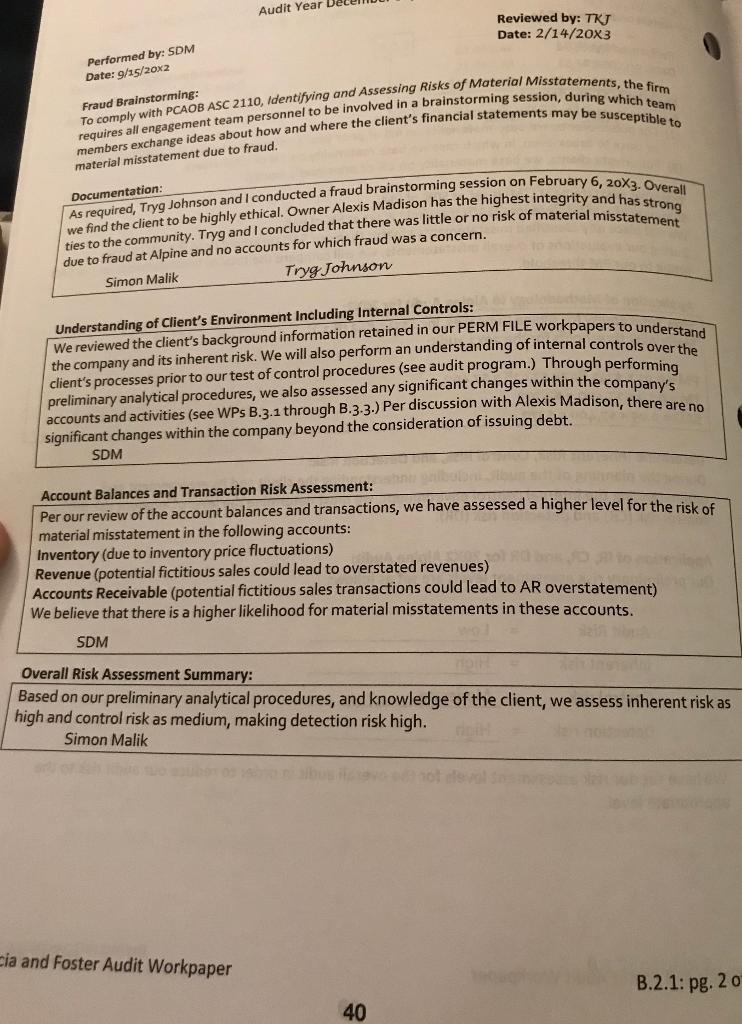

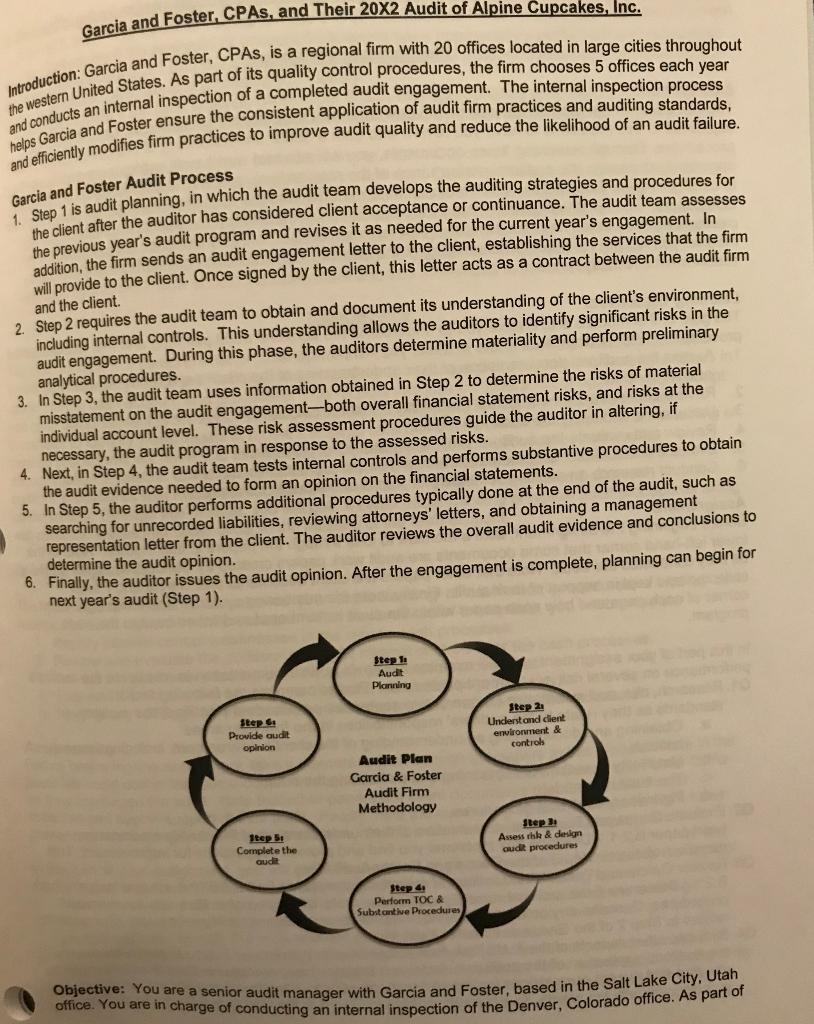

Before beginning the assignment, take a moment to look through the papers in this module. Note in the lower left-hand corner that some documents are audit work papers created by Garcia and Foster CPAS as they conducted the audit. Note that other papers are client documents that Garcia and Foster collected and kept in support of their audit. Finally, note the numbering system in the lower right-hand corner of each page and how each paper within the audit is numbered and linked back to the audit Q2. Evaluate Garcia and Foster's documentation of their understanding of the client's environment you discover with the memo. This question relates to Step 3 of the Garcia and Foster Audit Plan. B.2.1.) Determine if the auditors correctly applied the materiality concept in their risk assessment (workpaper B.2.1.) Describe any problems you find and provide suggestions for improvement. This Q4. Evaluate other aspects of the Audit Risk Assessment memo (workpaper B.2.1.) In particular, review Q3. Review Garcia and Foster's calculations of materiality thresholds for the 20X2 Audit (workpaper you find and provide suggestions for improvement. Identify and document any additional problems the auditors' application of the audit risk model and brainstorming processes. Describe any problems procedures. Describe any problems you find and provide suggestions for improvement. This question program. In this part of your assignment, you will examine the firm's audit documentation in relation to the auditors' performance on several risk assessment procedures. Please complete the following tasks: Qt, Research, cite, and summarize (in one or two sentences per standard identified) the auditing standards as they relate to the auditors' responsibilities in the following areas: a. Obtaining and documenting an understanding of the client's environment, including internal controls. b. Materiality assessment in planning and performing the audit. C. The audit risk model. d. Preliminary analytical procedures. question relates to Step 2 of the Garcia and Foster Audit Plan. relates to Step 2 of the Garcia and Foster Audit Plan. Alpine Cupcakes, Inc. Audit Risk Assessment Memo Audit Year December 31, 20X2 Garcia and Foster, CPAS Performed by: SDM Date: 9/15/20x2 Reviewed by: TKJ Date: 2/14/20X3 Materiality Methodology: Planning materiality (PM) is determined as follows: (2) For public clients, we base materiality on 4% of prior vear's net income unless the client is at a loss or close to break even, in which case we base materiality on 1% of total assets. (3) For private clients, we base materiality on 1% of prior year's equity. Tolerable misstatement (TM) is set at 50% of PM. Summary of audit differences (SAD) threshold is set at 5% of PM. We will place any identified misstatements greater than our SAD threshold onto the SAD listing. During our evaluations of overall misstatements, we will compare the total of misstatements on the SAC listing to our PM threshold. Application of Methodology to Alpine Audit for 20X2: 20x1 Total Equity for Alpine Cupcakes, Inc.: $741,842 (B.1.1) Materiality thresholds for the 20x2 audit: PM = 0.01 x $741,842= $7,418 = $7,400 TM = 0.50 x $7,400 = $3,700 SAD = 0.05 x $7,400 = $370 Determine Inherent Risk, Control Risk, and Detection Risk: During the planning of the audit, including understanding the client and its environment and understanding the internal control environment, we must determine the level of inherent risk (IR), control risk (CR) and detection risk (DR). Application of IR, CR, and DR for 20X2 Alpine Audit: Our preliminary risk assessment levels are set as follows: Audit Risk Low Inherent risk High Control risk Moderate Detection risk = High We have set our risk assessment levels for the overall audit in order to reduce our audit risk to the appropriate level. B.2.1: pg. 1 c Garcia and Foster Audit Workpaper 39 Audit Year Reviewed by: TKJ Date: 2/14/20x3 Performed by: SDM Date: 9/15/20x2 Fraud Brainstorming: material misstatement due to fraud. Documentation: due to fraud at Alpine and no accounts for which fraud was a concern. Simon Malik Tryg Johnson Understanding of Client's Environment Including Internal Controls: We reviewed the client's background information retained in our PERM FILE workpapers to understan the company and its inherent risk. We will also perform an understanding of internal controls over client's processes prior to our test of control procedures (see audit program.) Through performing preliminary analytical procedures, we also assessed any significant changes within the company's accounts and activities (see WPs B.3.1 through B.3.3.) Per discussion with Alexis Madison, there are significant changes within the company beyond the consideration of issuing debt. SDM Account Balances and Transaction Risk Assessment: Per our review of the account balances and transactions, we have assessed a higher level for the rick ef material misstatement in the following accounts: Inventory (due to inventory price fluctuations) Revenue (potential fictitious sales could lead to overstated revenues) Accounts Receivable (potential fictitious sales transactions could lead to AR overstatement) We believe that there is a higher likelihood for material misstatements in these accounts. SDM Overall Risk Assessment Summary: Based on our preliminary analytical procedures, and knowledge of the client, we assess inherent risk as high and control risk as medium, making detection risk high. Simon Malik artor cia and Foster Audit Workpaper B.2.1: pg. 2 o 40 gie and Foster, CPAS, and Their 20X2 Audit of Alpine upcakes, Inc. Garcia and Foster Audit Process Gaten 1 is audit planning, in which the audit team develops the auditing strategies and procedures for te dient after the auditor has considered client acceptance or continuance. The audit team assesses the previous year's audit program and revises it as needed for the current year's engagement. In addition, the firm sends an audit engagement letter to the client, establishing the services that the firm will provide to the client. Once signed by the client, this letter acts as a contract between the audit firm and the client. 2. Step 2 requires the audit team to obtain and document its understanding of the client's environment. including internal controls. This understanding allows the auditors to identify significant risks in the audit engagement. During this phase, the auditors determine materiality and perform preliminary analytical procedures. 3. In Step 3, the audit team uses information obtained in Step 2 to determine the risks of material misstatement on the audit engagement-both overall financial statement risks, and risks at the individual account level. These risk assessment procedures guide the auditor in altering, if necessary, the audit program in response to the assessed risks. 4. Next, in Step 4, the audit team tests internal controls and performs substantive procedures to obtain the audit evidence needed to form an opinion on the financial statements. 5. In Step 5, the auditor performs additional procedures typically done at the end of the audit, such as searching for unrecorded liabilities, reviewing attorneys' letters, and obtaining a management representation letter from the client. The auditor reviews the overall audit evidence and conclusions to determine the audit opinion. 6. Finally, the auditor issues the audit opinion. After the engagement is complete, planning can begin for next year's audit (Step 1). Step Audit Planning Step 6 Provide audt opinion Step 2 Understand dient environment & controh Audit Plan Garcia & Foster Audit Firm Methodology Itep S Complete the audit Step 3 Assess rhk & design oudt procedures Step d Perform TOC & Substantive Procedures Objective: You are a senior audit manager with Garcia and Foster, based in the Salt Lake City, Otan office. You are in charge of conducting an internal inspection of the Denver, Colorado office. As pan or

Step by Step Solution

3.44 Rating (154 Votes )

There are 3 Steps involved in it

solution auditor an auditor is an authorized personnel that reviews and verifies the accuracy of financial records and ensures that companies comply with tax norms their primary objective is to protec... View full answer

Get step-by-step solutions from verified subject matter experts