Question: Question 1 (10 points) Suppose that there are two factors represented by: (1) return on the market portfolio rM (2) return on Treasury bond portfolio

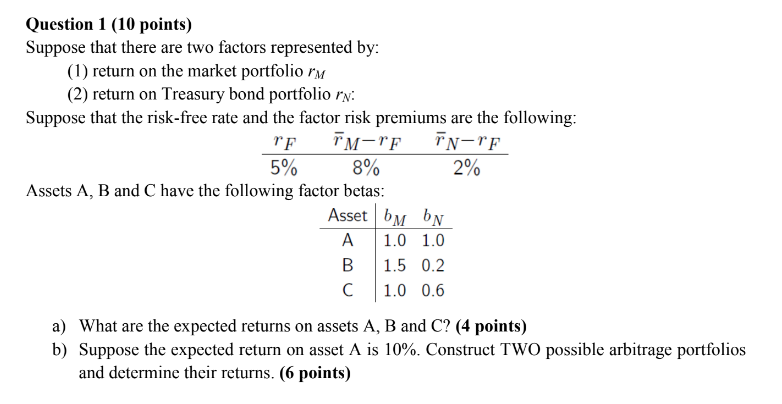

Question 1 (10 points) Suppose that there are two factors represented by: (1) return on the market portfolio rM (2) return on Treasury bond portfolio rv: Suppose that the risk-free rate and the factor risk premiums are the following: 5%8% Assets A, B and C have the following factor betas: - 0 2% Asset bMbN A 1.0 1.0 B 1.5 0.2 C1.0 06 a) b) What are the expected returns on assets A, B and C? (4 points) Suppose the expected return on asset A is 10%. Construct Two possible arbitrage portfolios and determine their returns. (6 points)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock