Question: QUESTION 1. (20 marks) We consider a two-step binomial market model (St)==0,1,2 with two return rates a=0,b=1, and So = 1. S2 = 4, C

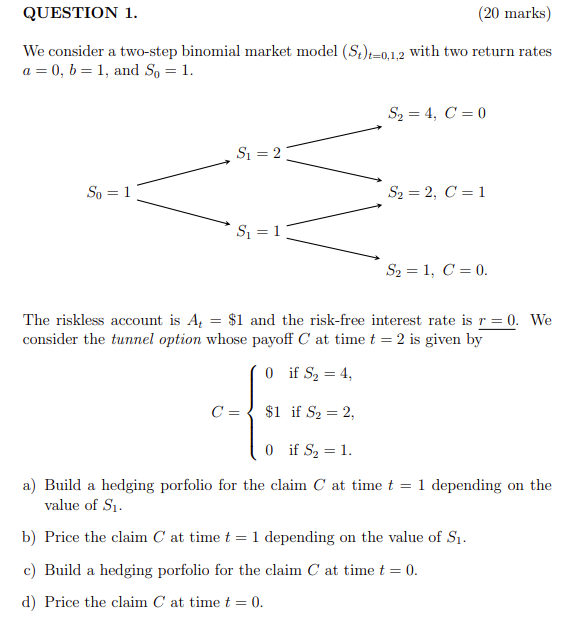

QUESTION 1. (20 marks) We consider a two-step binomial market model (St)==0,1,2 with two return rates a=0,b=1, and So = 1. S2 = 4, C = 0 Si = 2 So = 1 S2 = 2, C=1 S = 1 S2 = 1, C = 0. The riskless account is A = $1 and the risk-free interest rate is r = 0. We consider the tunnel option whose payoff C at time t = 2 is given by 0 if S2 = 4, C= $1 if S2 = 2, 0 if S2 = 1. a) Build a hedging porfolio for the claim C at time t = 1 depending on the value of S. b) Price the claim C at time t = 1 depending on the value of S. c) Build a hedging porfolio for the claim C at time t = 0. d) Price the claim C at time t = 0. QUESTION 1. (20 marks) We consider a two-step binomial market model (St)==0,1,2 with two return rates a=0,b=1, and So = 1. S2 = 4, C = 0 Si = 2 So = 1 S2 = 2, C=1 S = 1 S2 = 1, C = 0. The riskless account is A = $1 and the risk-free interest rate is r = 0. We consider the tunnel option whose payoff C at time t = 2 is given by 0 if S2 = 4, C= $1 if S2 = 2, 0 if S2 = 1. a) Build a hedging porfolio for the claim C at time t = 1 depending on the value of S. b) Price the claim C at time t = 1 depending on the value of S. c) Build a hedging porfolio for the claim C at time t = 0. d) Price the claim C at time t = 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts