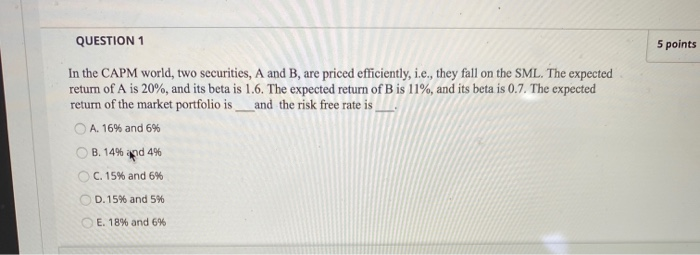

Question: QUESTION 1 5 points In the CAPM world, two securities, A and B, are priced efficiently, i.e., they fall on the SML. The expected return

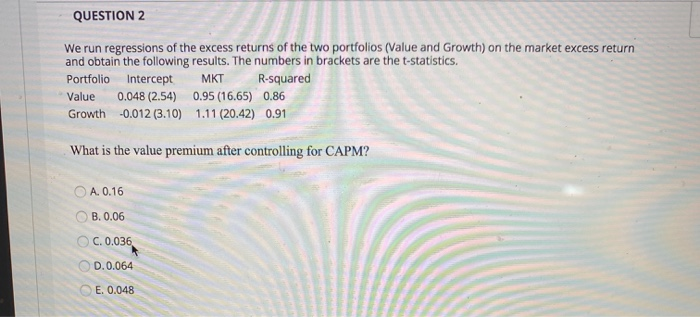

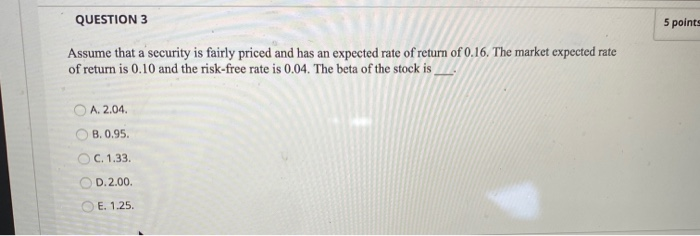

QUESTION 1 5 points In the CAPM world, two securities, A and B, are priced efficiently, i.e., they fall on the SML. The expected return of A is 20%, and its beta is 1.6. The expected return of Bis 11%, and its beta is 0.7. The expected return of the market portfolio is_and the risk free rate is A. 16% and 6% B. 14% and 4% C. 15% and 6% D. 15% and 5% E. 18% and 6% QUESTION 2 We run regressions of the excess returns of the two portfolios (Value and Growth) on the market excess return and obtain the following results. The numbers in brackets are the t-statistics. Portfolio Intercept MKT R-squared Value 0.048 (2.54) 0.95 (16.65) 0.86 Growth -0.012 (3.10) 1.11 (20.42) 0.91 What is the value premium after controlling for CAPM? A. 0.16 OB. 0.06 C. 0.036 D.0.064 E. 0.048 QUESTION 3 5 points Assume that a security is fairly priced and has an expected rate of return of 0.16. The market expected rate of return is 0.10 and the risk-free rate is 0.04. The beta of the stock is A. 2.04. OB. 0.95 C. 1.33 D.2.00 E. 1.25

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts