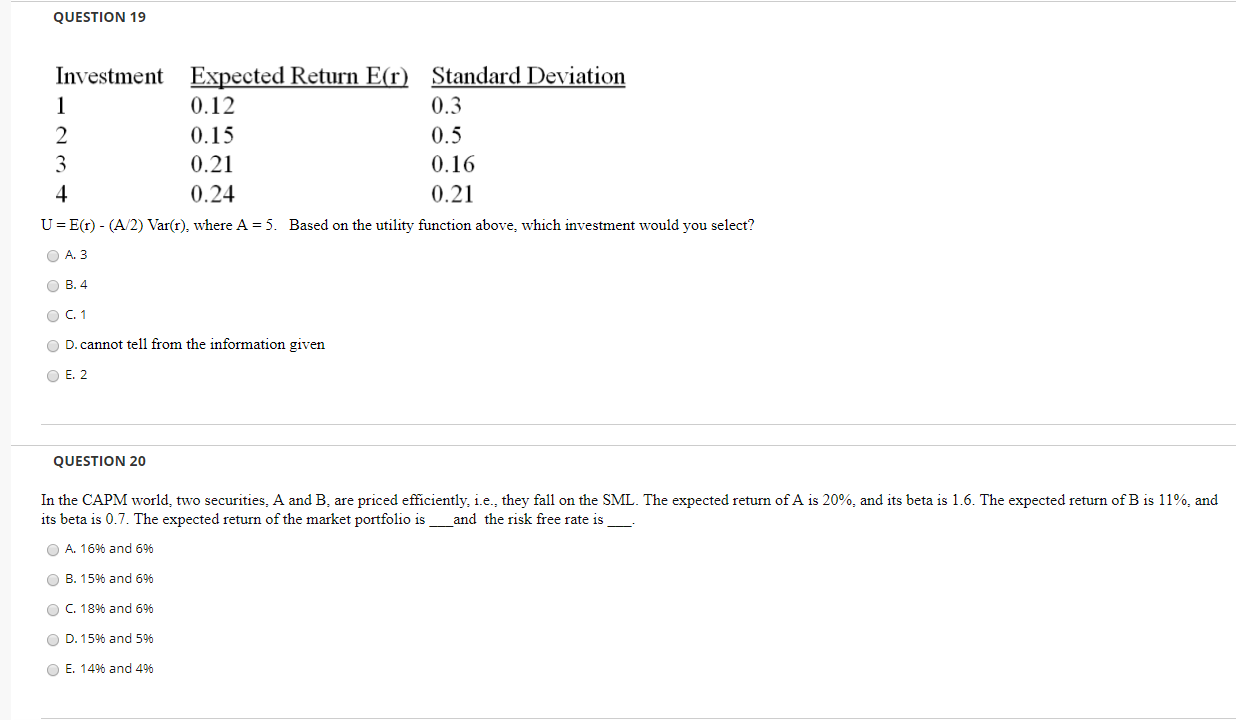

Question: QUESTION 19 Investment Expected Return E(r) Standard Deviation 0.12 0.3 0.15 0.5 0.21 0.16 0.24 0.21 U = E(1) - (A/2) Var(), where A =

QUESTION 19 Investment Expected Return E(r) Standard Deviation 0.12 0.3 0.15 0.5 0.21 0.16 0.24 0.21 U = E(1) - (A/2) Var(), where A = 5. Based on the utility function above, which investment would you select? A. 3 B.4 OC. 1 OD. cannot tell from the information given E. 2 QUESTION 20 In the CAPM world, two securities, A and B, are priced efficiently, i.e., they fall on the SML. The expected return of A is 20%, and its beta is 1.6. The expected return of B is 11%, and its beta is 0.7. The expected return of the market portfolio is_ and the risk free rate is __ A. 16% and 696 B. 1596 and 696 C. 1896 and 696 OD. 1596 and 596 E. 1496 and 496

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts