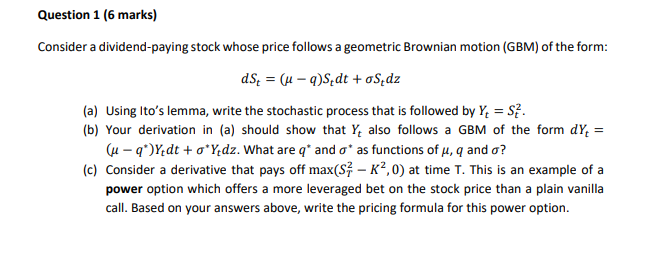

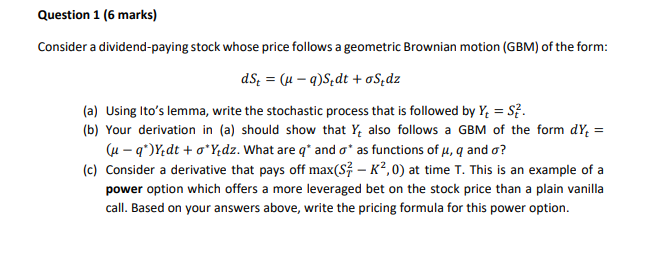

Question: Question 1 [6 marks} Consider a dividendpaving stoclt whose price follows a geometric Brownian motion {GBMJ of the form: as = o was: + ass:

Question 1 [6 marks} Consider a dividendpaving stoclt whose price follows a geometric Brownian motion {GBMJ of the form: as = o was: + ass: to] Using Ito's lemma, write the stochastic process that is followed hv Y: = SE. [is] "four derivation In Ila] should show that Yr also follows a GEM of the form of: = [p vitriol: + o's'z. What are If and o' as functions of ,u, q and o? [cl Consider a derivative that pavs off mastq' HE. D] at time T. This is an example of a power option which offers a more leveraged bet on the stock price than a plain vanilla call. Based on I.nsiur answers above, write the pricing formula for this power option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts