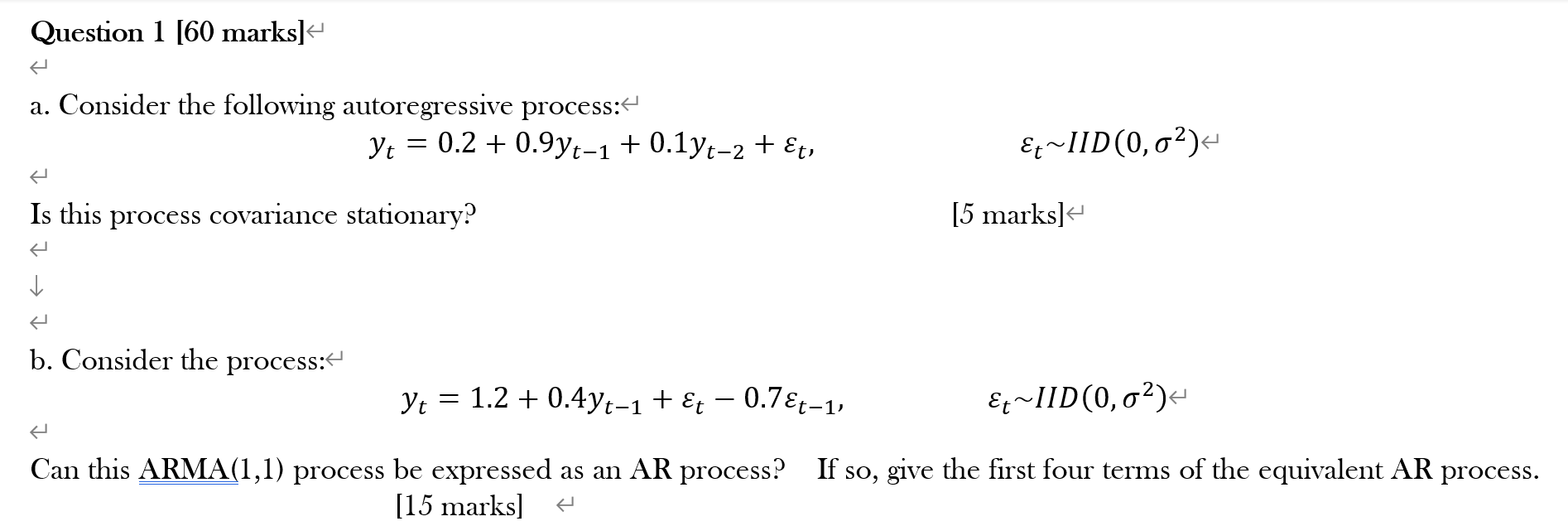

Question: Question 1 [60 marks] a. Consider the following autoregressive process: Question 1 [60 marksle a. Consider the following autoregressive process: Yt = 0.2 + 0.9Yt_1

Question 1 [60 marks] a. Consider the following autoregressive process:

Question 1 [60 marksle a. Consider the following autoregressive process: Yt = 0.2 + 0.9Yt_1 + 0. I y t _ 2 -k E Is this process covariance stationary. p b. Consider the process: Yt = 1.2 + 0.4yt_1 + Et o.7Et-1, [5 marks]e Can this ARMA(I,I) process be expressed as an AR process? If so, give the first four terms of the equivalent AR process. [15 marks]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock