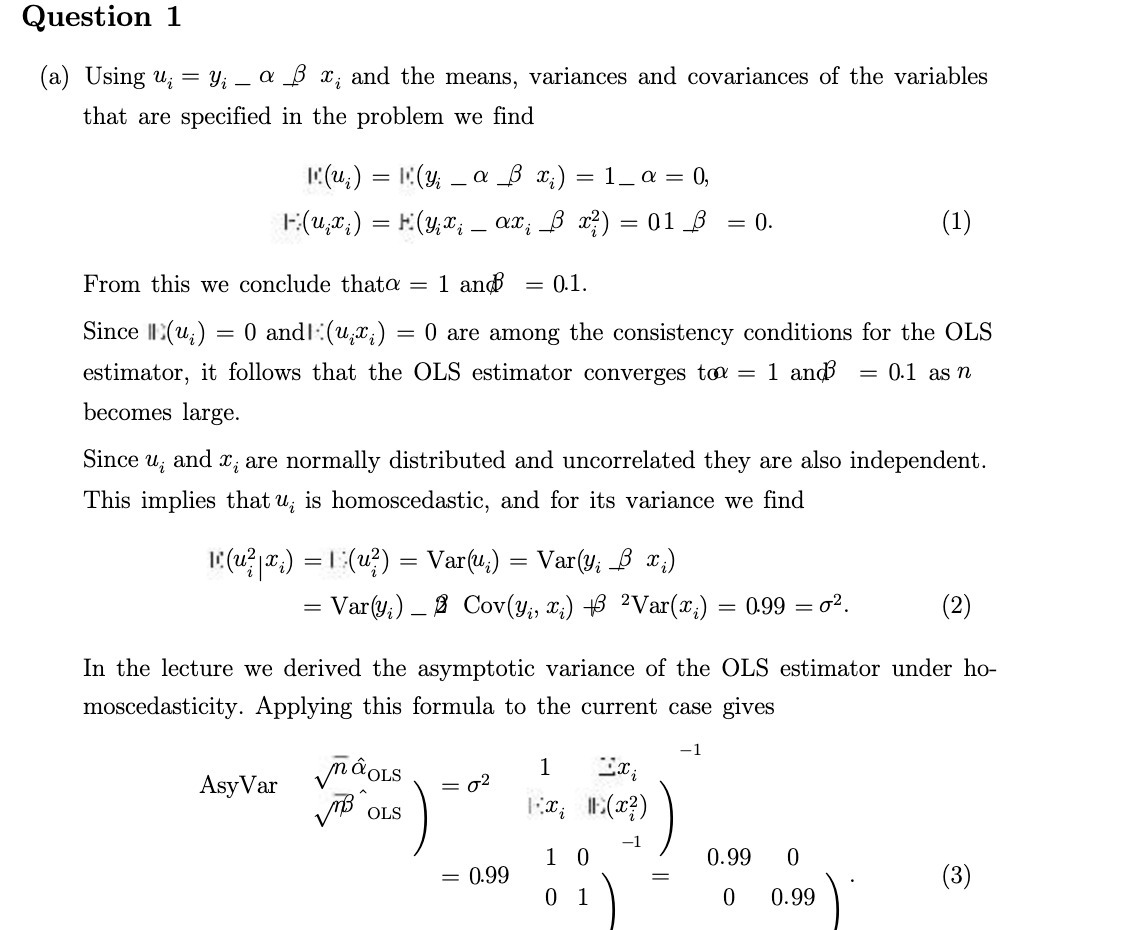

Question: Question 1 (a) Using u; = y; _ a B x; and the means, variances and covariances of the variables that are specified in the

Question 1 (a) Using u; = y; _ a B x; and the means, variances and covariances of the variables that are specified in the problem we find (u; ) = 1(y; _ a B x;) = 1_a=0, H(u,x; ) = H(y;x; _ ax; B x2) = 01 B =0. (1) From this we conclude thata = 1 and = 0.1. Since II:(u;) = 0 andl (ux;) = 0 are among the consistency conditions for the OLS estimator, it follows that the OLS estimator converges to = 1 and = 0.1 as n becomes large. Since u; and x; are normally distributed and uncorrelated they are also independent. This implies that u; is homoscedastic, and for its variance we find 1. (2 2 20;) = 1 :(u?) = Var(u;) = Var(y; B x;) = Var(y;) _ 2 Cov(yi, X;) +3 2Var(x;) = 0.99 = 02. (2) In the lecture we derived the asymptotic variance of the OLS estimator under ho- moscedasticity. Applying this formula to the current case gives MaOLS 1 Asy Var = 02 VOLS -1 1 0 0.99 0 0.99 = (3 0 1 0 0.99

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts