Question: Question 1 Jordan Lid acquired a new equipment on 1 July 2019 for $130,000 cash. The equipment has an estimated useful life of 10 years

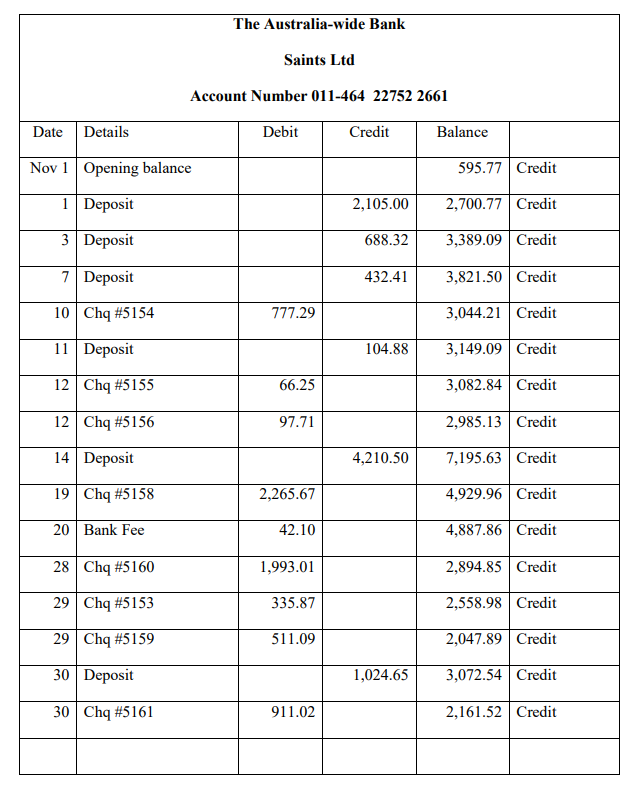

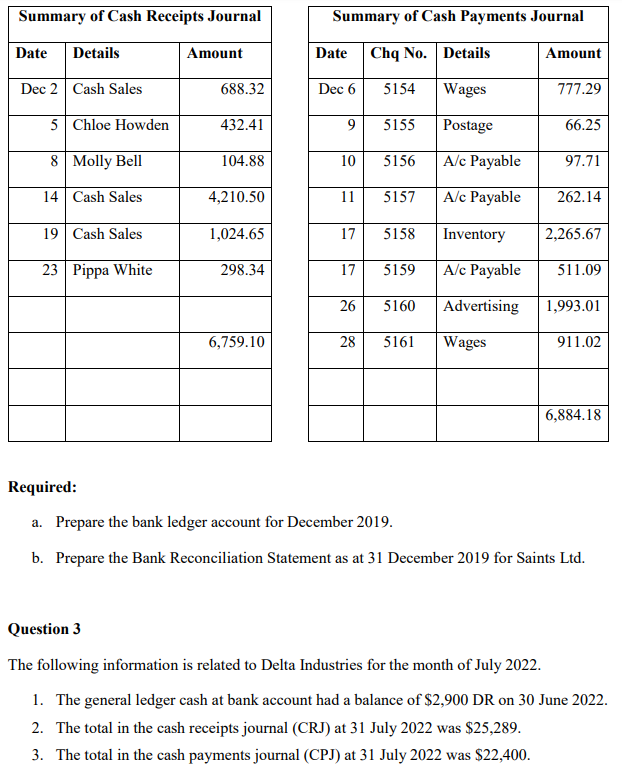

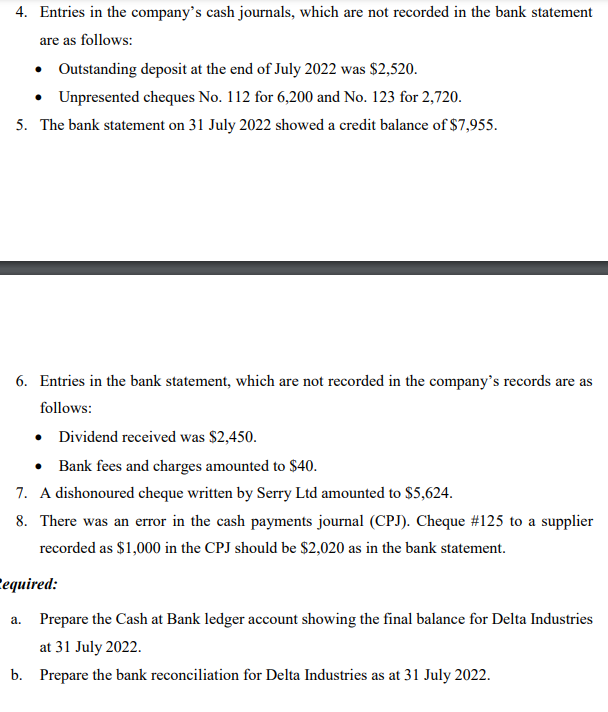

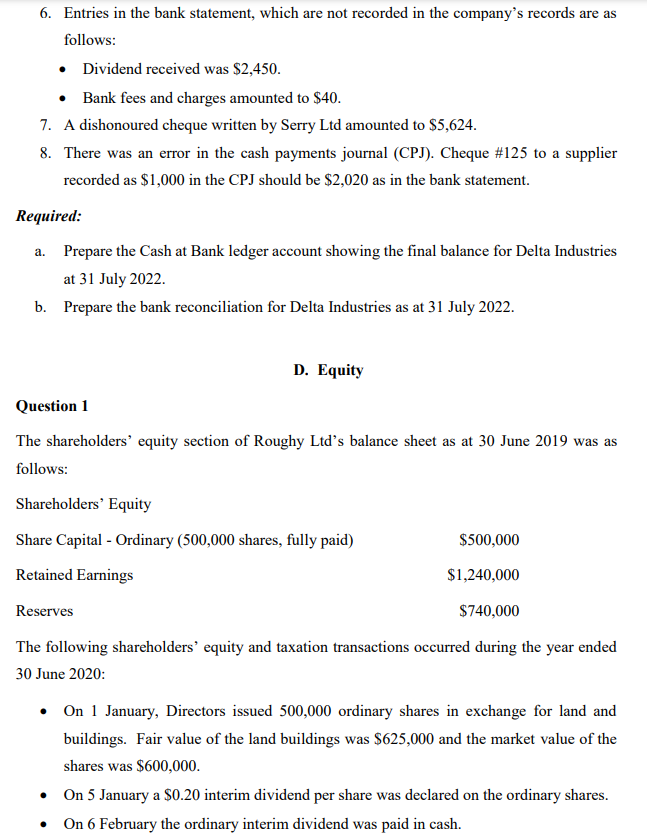

Question 1 Jordan Lid acquired a new equipment on 1 July 2019 for $130,000 cash. The equipment has an estimated useful life of 10 years and $10,000 residual value. On 30 June 2020, that equipment's fair value is $154,000. On 30 June 2021, there was no revaluation required. Jordan Ltd also purchased a new motor vehicle for cash on 1 July 2019 for $120,000. At this date the accountant determined the motor vehicle has a useful life of 4 years and an estimated residual value of $20,000. On 30 June 2020, there was no impairment recorded. On 30 June 2021, the motor vehicle had a value in use of $60,000 and the fair value less costs to sell was $58,000. Jordan Ltd uses the straight-line method to depreciate both assets. Required: a. Prepare the general journal entries for the financial years ending 30 June 2020 and 30 June 2021 related to the equipment assuming the asset is recorded under the fair value model. Justify your answer in accordance with appropriate accounting standards regarding the test of materiality. Narrations are NOT required. b. Prepare the general journal entries for the financial years ending 30 June 2020 and 30 June 2021 related to the motor vehicle assuming the asset is recorded under the cost model. Question 2 The following information is related to TWO non-current assets: Machine Delight Ltd acquired a new machine on 1 July 2020 for $300,000 and the purchase was financed through a bank loan. The machine has a residual value and useful life of $20,000 and 7 years, respectively. Delight Lid depreciates the machine using straight-line depreciation method. It was determined that there was no revaluation required on 30 June 2021. On 30 June 2022, the fair value of the machine is estimated to be $265,000.There was no revaluation required on 31} J one 21123. Motor vehica'e Delight Ltd purchased a motor vehicle on 1 J u|y 21121 for S cash. The useful life ofthe motor vehicle is 15 years with an estimated useful life of zero. On 311 June 21322. the motor vehicle had a recoverable amount of 545,111111. On 343' June 21123, there was no impairment recorded and on the same day1 the motor vehicle was sold for $411,111111 cash. Required: 1a} 1b} 1C} 1d} 16} Prepare the necessary general journal entries to record the transactions related to the machine for the nancial year ending 31] June 2112] [i.e.1 from 1 July 211211 to 311 June 21121]. Narrations are NOT required. Prepare the necessary general journal entries to record the transactions related to the machine for the nancial year ending 31] June 21122 [i.e.. from 1 July 21121 to 343' June 21122]. Justify your answer in accordance with appropriate accounting standards regarding the test of materiality. Narrations are HUT required. Prepare the necessary general journal entries to record the transactions related to the machine for the nancial year ending 31] June 21123 [i.e.1 from 1 July 21122 to 343' June 21123]. Narrations are NOT required. Prepare the necessary general journal entries to record the transactions related to the motor vehicle for the nancial year ending 311 June 21122 {i.e., from J July 21121 to 311 June 2&22}. Narrations are NOT required. Prepare the necessary general journal entries to record the transactions related to the motor vehicle for the nancial year ending 311 June 21123 {i.e., from J July 21122 to 311 June 2&23}. Narrations are NOT required. Question 3 Please see the following information related to the two noncurrent assets below: Equipment Cruise Ltd purchased equipment on I .luly EDI? for $l,,, with 343% deposit was paid in cash and the remaining 1was nanced through a bank loan. The useful life and residual value of the equipment were estimated to he 5 years and $ l. respectively. Cruise Ltd depreciates the equipment using the straightline method. The equipment is measured using the fair value jrevaluation! model. On 3|] June E, the fair value of the equipment was estimated to he $T,. There was no revaluation required for the equipment on St] .lune 2G2 l. Machine In addition. Cruise Ltd also purchased a new machine on I .luly 24319 for $96,933 cash. The useful life ofthe machine was expected to he t'i years, with an estimated residual value of zero. Cruise Ltd depreciates the machine using the straightline method. The machine is measured using the cost ! impain'nentl model. On 313 June EDED. the value in use of the machine was $. and the fair value less costs to sell of the machine was $65,. There was no impairment recorded on the machine on 30' June Zll. Required: {a} Prepare the necessary general journal entries to record the transactions related to the equipment for the nancial year ending 3|} June It'll] {i.e.. from 1 July Ell]? to 30 June Required: (a) Prepare the necessary general journal entries to record the transactions related to the equipment for the financial year ending 30 June 2020 (i.e., from 1 July 2019 to 30 June 2020). Justify your answer in accordance with appropriate accounting standards regarding the test of materiality. Narrations are NOT required. (b) Prepare the necessary general journal entry to record the transaction related to the equipment for the financial year ending 30 June 2021 (i.e., from 1 July 2020 to 30 June 2021). Narrations are NOT required. (c) Prepare the necessary general journal entries to record the transactions related to the machine for the financial year ending 30 June 2020 (i.e., from 1 July 2019 to 30 June 2020). Narrations are NOT required. (d) Prepare the necessary general journal entry to record the transaction related to the machine for the financial year ending 30 June 2021 (i.e., from 1 July 2020 to 30 June 2021). Narrations are NOT required.B. Leases Question 1 On 1 July 2018, Jones Lid entered into a non-cancellable, three-year lease of a computer system. The computer had a fair value of $30,000 and a present value of the minimum lease payments of $29,868. The computer had an estimated useful life of 4 years and a zero- residual value. The lease involved an initial payment of $5,000 on 1 July 2018 plus 3 annual payments of $10,000. Payments, except for the initial payment, are made on 30 June each year. The implicit interest rate in the lease is 10% p.a. Jones Lid intends to buy the computer at the end of the lease term. Required: a. Prepare a lease schedule for the three years of the lease. b. Prepare the general journal entries relating to the lease for the year ending 30 June 2019. c. Prepare the income statement extract for the year ended 30 June 2019. d. Prepare the balance sheet extract at 30 June 2019. Question 2 Consider the following terms relating to a lease involving machinery entered into by Superman Lid. on 1 July 2019: One initial payment of $200,000 at the date of signing, three further payments of $200,000 on 30 June each year in 2020, 2021 and 2022, and a final payment of $80,004 30 June 2023. Superman Ltd. will return the machinery at the end of the lease term. The interest rate in the lease is 20%. The machinery is expected to have a five- year useful life. It has no residual value and is depreciated using straight line. The present value of the minimum lease payments is $659,878.HEQHIFE'H: a. Prepare a lease schedule for the four years of the lease. h. Prepare the genera] journal entries relating to the lease for the years ending 30' June E and 3d June 2'32 l. c. Prepare the income statement extract for the year ended 3|] June ELIE]. d. Prepare the balance sheet extract as at 3H J une Ell? l. Question 3 On 1 July Edit]. Patrick Ltd entered into a non-cancellahle1 three-year lease of a computer system. The computer had a Fair value of $15.10!] and a present value of the minimum lease payments cf'S [4.934. The computer had an estimated useful life of4 years and a zero-residual value. The lease involved an initial payment cf$2,5 on 1 July 2G2!) plus 3 annual payments of 55.900. Payments. except for the initial payment, are made on 3t] June each year. The implicit interest rate in the lease is [3% p.a. Ownership cf'the computer system will transfer to Patrick Ltd at the end of the lease term. Required: a. Prepare a lease schedule for the three years of the lease. h. Prepare the genera] journal entries relating to the lease for the financial year ending 3t] J une ZDZI. Justify your entries by reference to the appropriate accounting standard AASB to leases. Narrations are NOT required. c. Prepare the Balance Sheet extract as at 343' June 2132]. d. Prepare the Income Statement extract for the year ended 3|] June 2G2 l. C. Bank Reconciliation Question 1 At the end of the second month of trading, the owner of Super Services Pty Ltd prepared the information for a bank reconciliation. The following has been provided: The bank ledger account balance at 30 April 2021 was $109,920 Dr. The bank statement on 31 May 2021 showed a credit balance of $96,460. A comparison between the business records and the bank statement highlighted the following: Entries in the bank statement, which are not in the company's records, follow: i. Interest received into the account $280 ii. Bank fees and charges $78 Entries in the company's cash journals, which are not recorded in the bank statement, follow: i. Deposits not appearing in the bank statement $6,840 ii. Unpresented cheques No. 54 for $1,978, No. 63 for $1,730 Other information a. Chq no. 95 to a creditor recorded as $320 in the Cash Payments Journal should be $300 as in the bank statement. b. Other information reveals the total in the Cash Receipts Journal at 31 May 2021 is $55,390, while the total in the Cash Payments Journal at 31 May 2021 is $65,940.Required: a. Prepare the Cash at Bank ledger account showing the final balance at 31 May 2021. b. Prepare a Bank Reconciliation Statement at 31 May 2021. Question 2 The owner of Saints Ltd performs the bank reconciliation procedure at the end of each month. She is in the process of preparing the statement for the month of December 2019, and has gathered the following information: Saints Ltd Bank Reconciliation Statement as at 30 November 2019 $ Balance as per bank statement 595.77 Cr Add deposits not credited 2.105.00 2,700.77 Less unpresented cheques #5153 (335.87) Balance as per bank ledger account 2,364.90 DrThe Australia-wide Bank Saints Ltd Account Number 011-464 22752 2661 Date Details Debit Credit Balance Nov 1 Opening balance 595.77 Credit Deposit 2,105.00 2,700.77 Credit 3 Deposit 688.32 3,389.09 Credit Deposit 432.41 3,821.50 Credit 10 Chq #5154 777.29 3,044.21 Credit 11 Deposit 104.88 3,149.09 Credit 12 Chq #5155 66.25 3,082.84 Credit 12 Chq #5156 97.71 2,985.13 Credit 14 Deposit 4,210.50 7,195.63 Credit 19 Chq #5158 2,265.67 4,929.96 Credit 20 | Bank Fee 42.10 4,887.86 Credit 28 Chq #5160 1,993.01 2,894.85 Credit 29 Chq #5153 335.87 2,558.98 Credit 29 Chq #5159 511.09 2,047.89 Credit 30 Deposit 1,024.65 3,072.54 Credit 30 Chq #5161 911.02 2,161.52 CreditSummary of Cash Receipts Journal Summary of Cash Payments Journal Date Details Amount Date Chq No. Details Amount Dec 2 Cash Sales 688.32 Dec 6 5154 Wages 777.29 5 Chloe Howden 432.41 9 5155 Postage 66.25 8 Molly Bell 104.88 10 5156 A/c Payable 97.71 14 Cash Sales 4,210.50 11 5157 A/c Payable 262.14 19 Cash Sales 1,024.65 17 5158 Inventory 2,265.67 23 Pippa White 298.34 17 5159 A/c Payable 511.09 26 5160 Advertising 1,993.01 6,759.10 28 5161 Wages 911.02 6,884.18 Required: a. Prepare the bank ledger account for December 2019. b. Prepare the Bank Reconciliation Statement as at 31 December 2019 for Saints Ltd. Question 3 The following information is related to Delta Industries for the month of July 2022. 1. The general ledger cash at bank account had a balance of $2,900 DR on 30 June 2022. 2. The total in the cash receipts journal (CRJ) at 31 July 2022 was $25,289. 3. The total in the cash payments journal (CPJ) at 31 July 2022 was $22,400.4. Entries in the company's cash journals1 which are not recorded in the bank statement are as follows: I Outstanding deposit at the end of July 21222 was $2.52. I Unpresented cheques No. 1 12 for b.2430 and No. 123 for 2.2243. 5. The bank statement on 3] Jul}; 2D22 showed a credit balance of'$'.l.955. ti. Entries in the bank statement1 which are not recorded in the company's records are as follows: I Dividend received was 52.4543. I Bank fees and charges amounted to 34!]. "a". A dishonoured cheque written by Berry Ltd amounted to 55.624. 3. There was an error in the cash payments journal {CPJ}. Cheque #l25 to a supplier recorded as $1 Hill] in the CPI should be $2,D2D as in the bank statement. required: a. Prepare the 'Cash at Bank ledger account showing the nal balance for Delta Industries at 31 Jul}.r 222. b. Prepare the bank reconciliation for Delta Industries as at 3| July 222. ti. Entries in the bank statement1 which are not recorded in the company's records are as follows: I Dividend received was 32,459. I Bank fees and charges amounted to Ml]. T. A dishonoured cheque written by Berry Ltd amounted to 55.624. 3. There was an error in the cash payments journal {CPJ}. Cheque #l25 to a supplier recorded as $1 , in the CPI should be ELIE!) as in the bank statement. Required: a. Prepare the Cash at Bank ledger account showing the nal balance I or Delta Industries at 31 July EGEE. b. Prepare the bank reconciliation for Delta Industries as at 3l July 21322. I]. Equity Question 1 The shareholders' equity section of'Roughy Ltd's balance sheet as at 3B June EDIE! was as fol lows: Shareholders' Equity Share Capital Ordinary {S shares, fully paid} $5, Retained Earnings $1,24, Reserves $74!],l] The following shareholders' equity and taxation transactions occurred during the year ended 3U June 2929: I On 1 January, Directors issued SDDJJIJD ordinary shares in exchange for land and buildings. Fair value of the land buildings was Sl- and the market value of the shares was $,ll I On 5 January a 50.243 interim dividend per share was declared on the ordinary shares. I On ti February the ordinary interim dividend was paid in cash. . On 6 February the ordinary interim dividend was paid in cash. . On 30 June the company's income tax expense was estimated to be $75,600 and profit before tax was $300,000. . On 30 June the company transferred $50,000 from retained earnings to Reserves. . On 30 June Directors declared a $0.30 ordinary dividend. Required: Prepare the journal entries to record the above transactions and events. Question 2 The following information is related to the shareholder's equity of King Ltd at 1 July 2022. Shareholder's equity Share capital (1,000,000 shares) $1,000,000 General reserve $400,000 Retained earnings $500,000 Total $1,900,000 . On 5 July 2022, King Ltd issued 200,000 shares for $200,000 cash. . On 1 August 2022, King Ltd declared an interim dividend of 5 cents per share. The dividend was paid on 1 September 2022. . The profit before tax for the year ended 30 June 2023 was $700,000 and the income tax was $210,000.The profit before tax for the year ended 30 June 2023 was $700,000 and the income tax was $210,000. . On 30 June 2023, King Ltd transferred $50,000 from retained earnings to general reserve. On 30 June 2023, King Ltd declared a final dividend of 10 cents per share. Required: Prepare general journal entries to record all the above transactions and events. Narrations are NOT required.E. Inventory valuation Question 1 Jack Ltd is a wholesale distributor of hand-made glazed garden pots to retail stores. Details for March 2021 are shown below. March 1 Opening inventory 2,000 pots - cost $35 each 9 Purchases 1,600 pots - purchase price $36 each 23 Purchases 1,000 pots - purchase price $37 each 31 Closing inventory 1,500 pots from the stock take Additional information: i. Freight costs from the supplier to Jack Lid.'s warehouse is $4 for each garden pot. Jack Ltd pays for these freight costs. ii. The latest selling price of the garden pots is $84 each. The handling and transportation costs is $10 each pot (paid by Jack Ltd). iii. 200 of the garden pots in the closing inventory (originally purchased on 23 January) have imperfections in the glazing and can only be sold for $30 each. Handling and transportation costs of $10 still apply. iv. Jack Ltd prepares monthly reports and applies the periodic (physical) and the first-in- first-out (FIFO) method. Required: a. Calculate the value of total closing inventory at 31 March 2021 as provided for in AASB 102. Justify all assumptions and calculations. b. Prepare necessary journal entry to record the inventory write-down. Narrations are NOT required.Question 2 Veronica Fresh is a wholesale distribution business that sells a flavoured cheese product to supermarkets. The following relates to the business's activities during January 2020: January 1 Opening inventory 2,000 boxes - cost $8.40 6 Sales 800 boxes - selling price $14.00 8 Purchases 1,000 boxes - cost $9.00 18 Sales 600 boxes - selling price $14.00 23 Purchases 1,500 boxes - cost $9.60 27 Sales 900 boxes - selling price $14.50 31 Closing inventory (as per physical stocktake) 2,200 boxes Additional information i. Two hundred boxes from the 8/1 purchase have passed their use-by date and cannot be sold for human consumption. However, they can be sold as poultry feed for $2 per box. ii. Transportation from the supplier to Veronica Fresh costs $1 per box. Transportation from Veronica Fresh to supermarkets costs $1.20 per box and would also apply to boxes sold for poultry feed. Veronica Fresh pays both sets of transportation costs. Required: a. Calculate the value of closing inventory as provided for in AASB 102, applying the weighted average cost under periodic system. Justify all aspects of your calculation. b. Prepare necessary journal entry to record the inventory write-down expense. Narrations are NOT required.Question 3 Williams Ltd is a wholesale distribution business that sells ceramic vases. Williams Ltd uses the periodic inventory system. The following information relates to the business's activities during the financial year ending 30 June 2021: 1 July 2020 - Opening balance 10,000 vases (purchase price $35 per vase) 1 September 2020 - Purchased 20,000 vases (purchase price $37 per vase) 1 February 2021 - Purchased 30,000 vases ($40 per vase) 30 June 2021 - Closing inventory as per physical stocktake is 44,000 vases Additional information: 1 . Williams Ltd adopts the FIFO cost-flow method. 1i. Transportation from supplier to Williams Ltd costs $8 per vase. Transportation from Williams Ltd to the retailer costs $10 per vase. Williams Ltd pays all of the transportation costs. iii. 4,000 of the vases in the closing inventory are damaged and can only be sold to the retailer for $20 per vase. These vases were originally purchased on 1 February 2021. Transportation cost to the retailer of $10 per vase still applies. iV . The latest selling price for the ceramic vases is $90 per vase. Required: a. Calculate the value of inventory in the Balance Sheet of Williams Ltd at 30 June 2021 in accordance with AASB 102 Inventories. Justify your answer and show all workings. b. Calculate Cost of Sales for the financial year ending 30 June 2021. Show your workings. c. Prepare the necessary journal entries to record the inventory write-down expense. Narrations are not required

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To tackle these problems lets break them down step by step Question 1 a Journal Entries for Equipmen... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!