Question: Question 1 through Question 4 are based on the information on current spot and forward term structures (assume the corporate debt pays interest annually) in

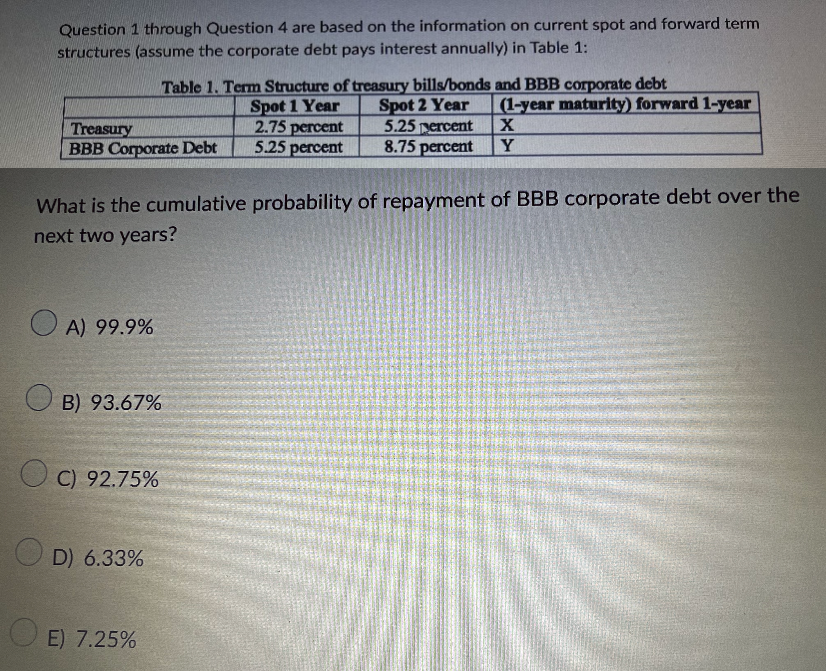

Question 1 through Question 4 are based on the information on current spot and forward term structures (assume the corporate debt pays interest annually) in Table 1: Table 1. Term Structure of treasury bills/bonds and BBB corporate debt Spot 1 Year (1-year maturity) forward 1-year Spot 2 Year 5.25 percent 2.75 percent X Treasury BBB Corporate Debt 5.25 percent 8.75 percent Y What is the cumulative probability of repayment of BBB corporate debt over the next two years? A) 99.9% B) 93.67% C) 92.75% D) 6.33% E) 7.25%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock