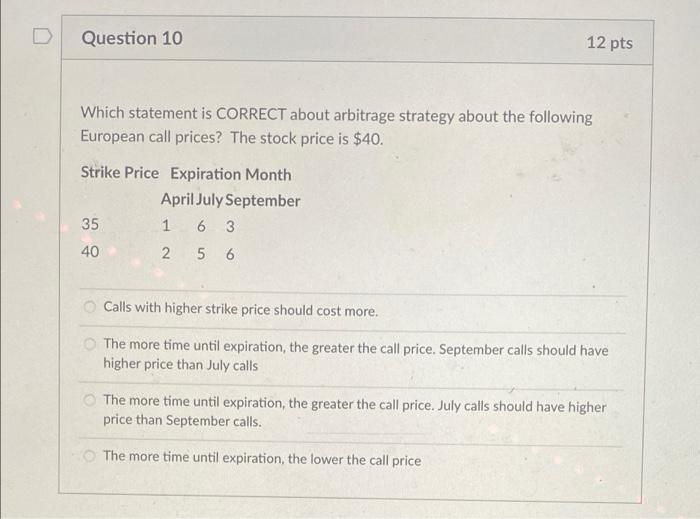

Question: Question 10 12 pts Which statement is CORRECT about arbitrage strategy about the following European call prices? The stock price is $40. Strike Price Expiration

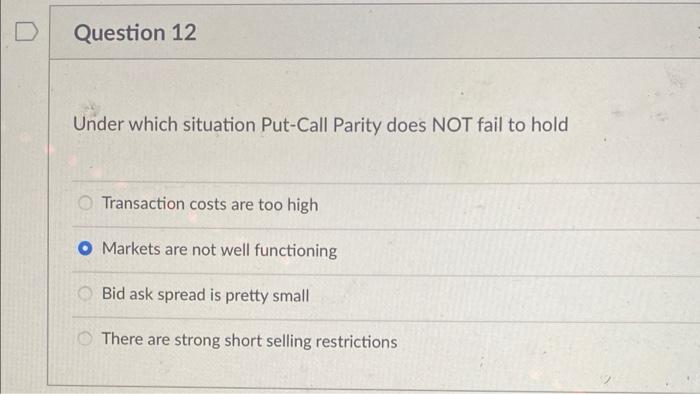

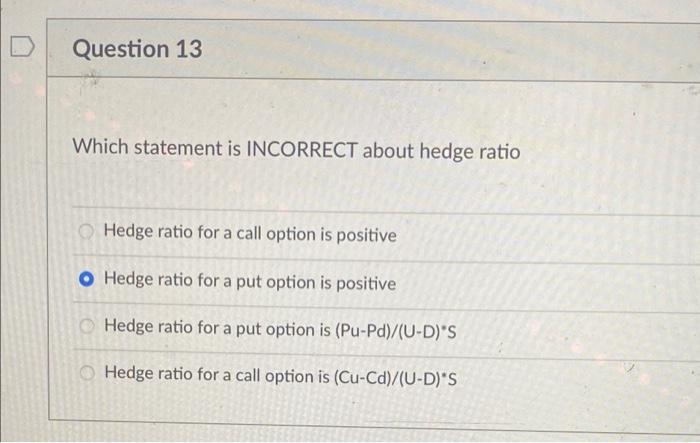

Question 10 12 pts Which statement is CORRECT about arbitrage strategy about the following European call prices? The stock price is $40. Strike Price Expiration Month AprilJuly September 1 6 3 40 2 5 6 35 Calls with higher strike price should cost more. The more time until expiration, the greater the call price. September calls should have higher price than July calls The more time until expiration, the greater the call price. July calls should have higher price than September calls. The more time until expiration, the lower the call price D Question 12 Under which situation Put-Call Parity does NOT fail to hold Transaction costs are too high O Markets are not well functioning Bid ask spread is pretty small There are strong short selling restrictions Question 13 Which statement is INCORRECT about hedge ratio Hedge ratio for a call option is positive O Hedge ratio for a put option is positive Hedge ratio for a put option is (Pu-Pd)/(U-D)'S Hedge ratio for a call option is (Cu-Cd)/(U-D)'S a

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts