Question: QUESTION 11 Use the data below for questions 11 to 15 (among the 4 options in each multiple choice, choose the one that is equal,

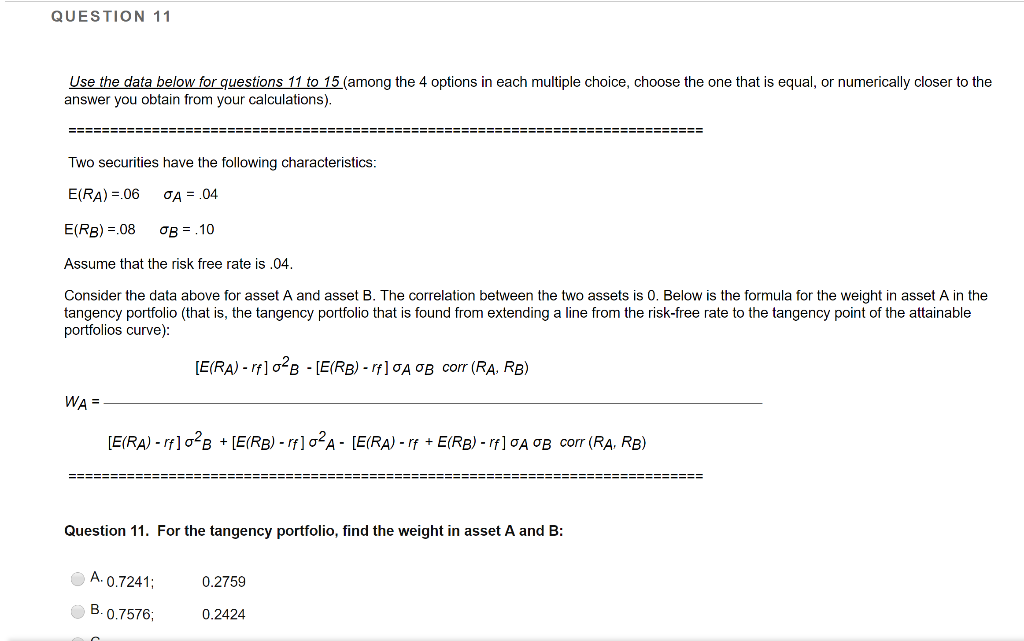

QUESTION 11 Use the data below for questions 11 to 15 (among the 4 options in each multiple choice, choose the one that is equal, or numerically closer to the answer you obtain from your calculations). = = ==== ==== === == == == ===== === == = === ===== === = == ===== === === = == === ===== === = == === = Two securities have the following characteristics: E(RA) = 06 OA = .04 E(RB) = 08 0B = 10 Assume that the risk free rate is .04. Consider the data above for asset A and asset B. The correlation between the two assets is 0. Below is the formula for the weight in asset A in the tangency portfolio (that is, the tangency portfolio that is found from extending a line from the risk-free rate to the tangency point of the attainable portfolios curve): [E(RA) - r*] 0B - [E(RB) - rf10A OB corr (RA, RB) WA= [E(RA) - rf] 02B + [E(RB) - rf] 02A - [E(RA) - rf + E(RB) - rf] CA OB corr (RA, RB) == === ===== === === = == == === === === ===== === === == = == === == === == = === === ===== == = == == Question 11. For the tangency portfolio, find the weight in asset A and B: 0.2759 A.0.7241; B.0.7576; 0.2424

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts