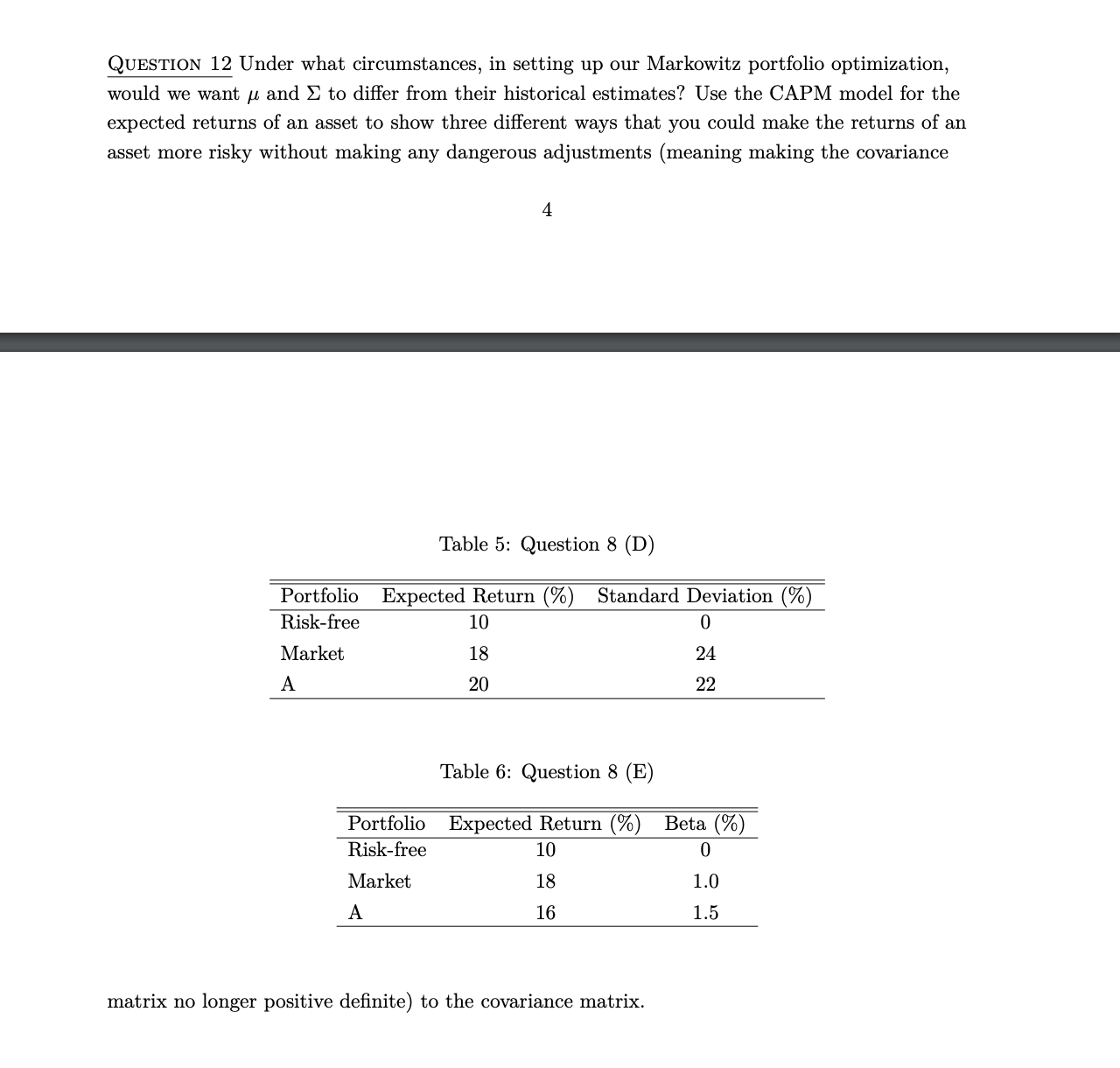

Question: QUESTION 12 Under what circumstances, in setting up our Markowitz portfolio optimization, would we want ,u and E to differ from their historical estimates? Use

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts