Question: QUESTION 16 A 5year zero coupon bond is stated to yield 10% continuousiy compounded return for the entire period (holding period return over 5 years)

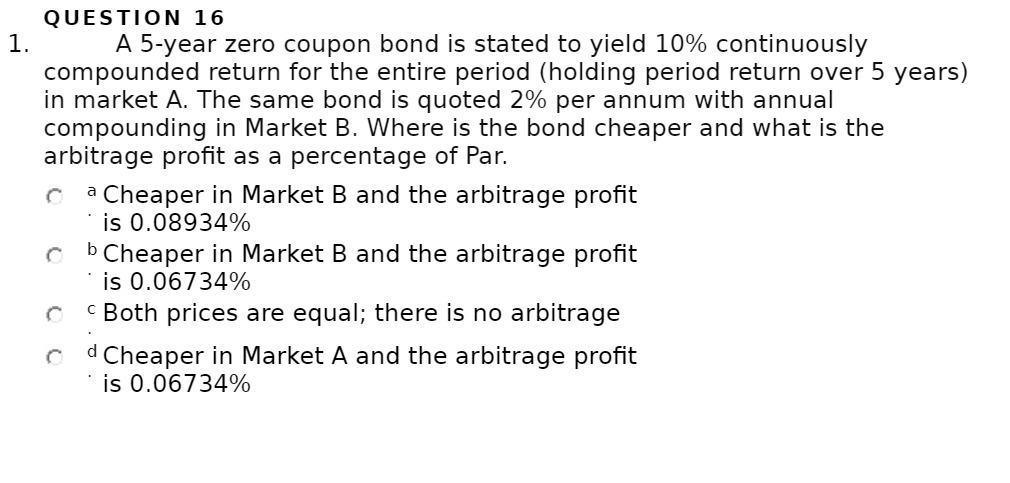

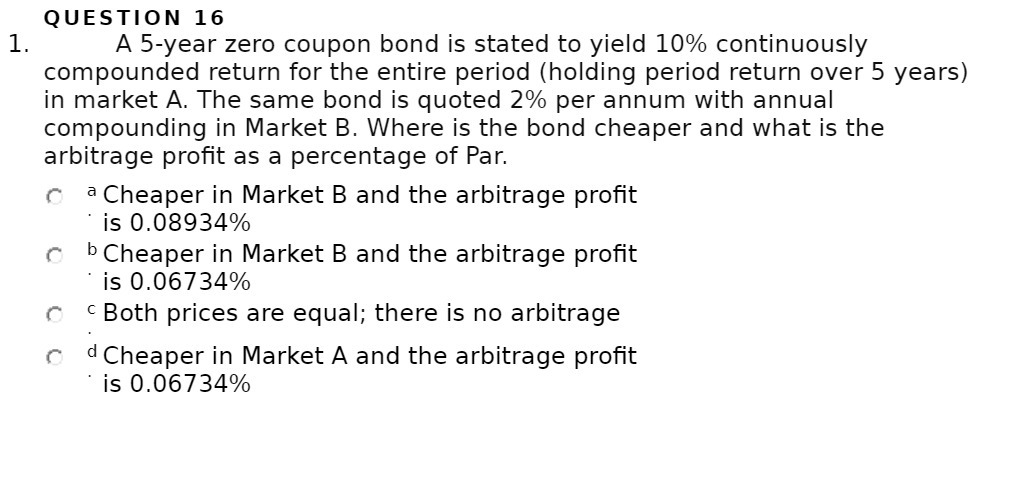

QUESTION 16 A 5year zero coupon bond is stated to yield 10% continuousiy compounded return for the entire period (holding period return over 5 years) in market A. The same bond is quoted 2% per annum with annual compounding in Market B. Where is the bond cheaper and what is the arbitrage prot as a percentage of Par. 1" a Cheaper in Market B and the arbitrage prot ' is 0.0893496 r' b Cheaper in Market B and the arbitrage prot ' is 0.0673496 r" C Both prices are equal; there is no arbitrage F d Cheaper in Market A and the arbitrage prot ' is 0.06734%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock