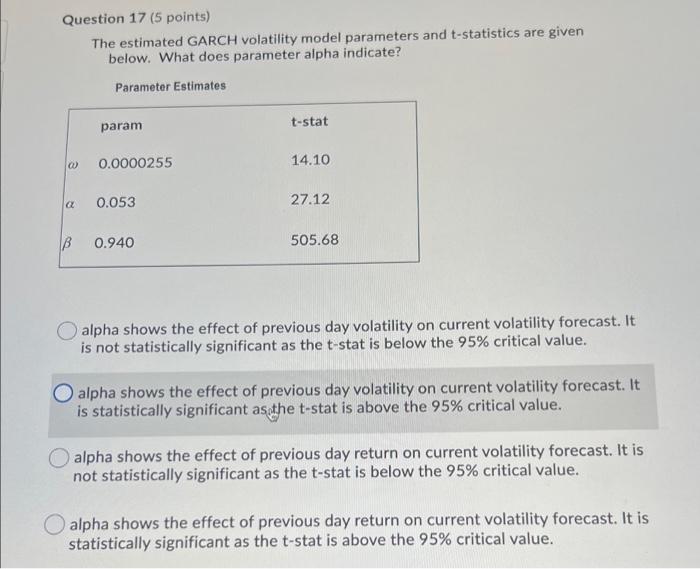

Question: Question 17 (5 points) The estimated GARCH volatility model parameters and t-statistics are given below. What does parameter alpha indicate? Parameter Estimates t-stat param 0)

Question 17 (5 points) The estimated GARCH volatility model parameters and t-statistics are given below. What does parameter alpha indicate? Parameter Estimates t-stat param 0) 0.0000255 14.10 0.053 27.12 CZ 0.940 505.68 alpha shows the effect of previous day volatility on current volatility forecast. It is not statistically significant as the t-stat is below the 95% critical value. O alpha shows the effect of previous day volatility on current volatility forecast. It is statistically significant as the t-stat is above the 95% critical value. alpha shows the effect of previous day return on current volatility forecast. It is not statistically significant as the t-stat is below the 95% critical value. alpha shows the effect of previous day return on current volatility forecast. It is statistically significant as the t-stat is above the 95% critical value

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts