Question: Question 2 (5 points) The estimated GARCH volatility model parameters and t-statistics are given below. Volatility Prediction for today is 20%. If the stock falls

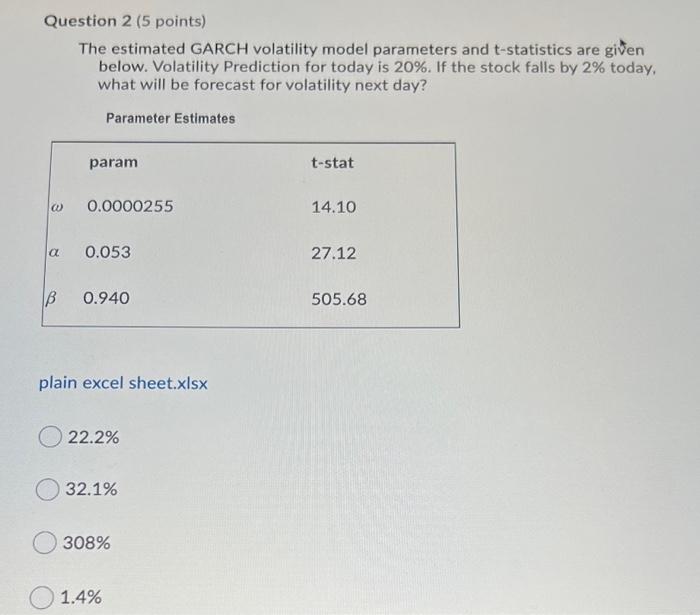

Question 2 (5 points) The estimated GARCH volatility model parameters and t-statistics are given below. Volatility Prediction for today is 20%. If the stock falls by 2% today, what will be forecast for volatility next day? Parameter Estimates param t-stat @ 0.0000255 14.10 a 0.053 27.12 B 0.940 505.68 plain excel sheet.xlsx 22.2% 32.1% 308% 1.4%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock