Question: Question 17. Consider a binomial model with So = 100, u = 1.2, d = .9 and r = .05. Use a three period (two

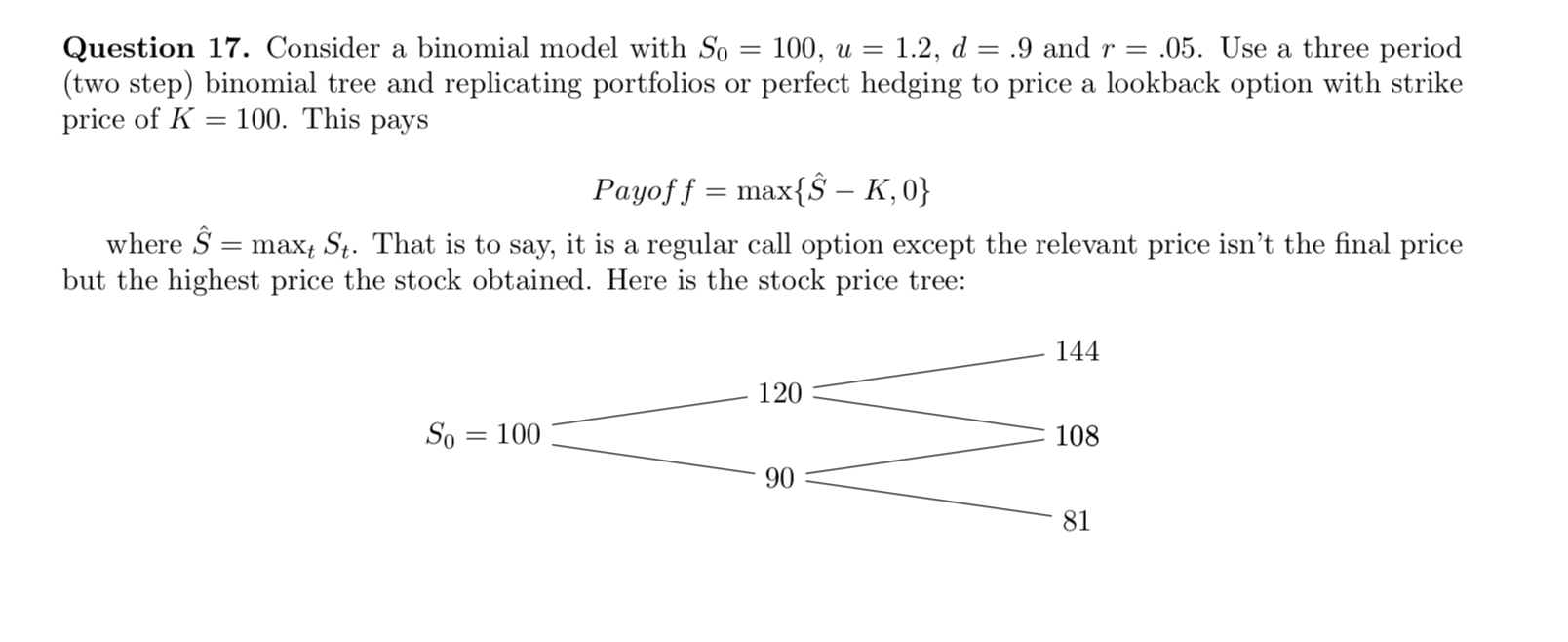

Question 17. Consider a binomial model with So = 100, u = 1.2, d = .9 and r = .05. Use a three period (two step) binomial tree and replicating portfolios or perfect hedging to price a lookback option with strike price of K = 100. This pays Payof f = max{ K,0} where = max+ St. That is to say, it is a regular call option except the relevant price isn't the final price but the highest price the stock obtained. Here is the stock price tree: 144 - 120 - So = 100 - = 108 - 90 - - 81 Question 17. Consider a binomial model with So = 100, u = 1.2, d = .9 and r = .05. Use a three period (two step) binomial tree and replicating portfolios or perfect hedging to price a lookback option with strike price of K = 100. This pays Payof f = max{ K,0} where = max+ St. That is to say, it is a regular call option except the relevant price isn't the final price but the highest price the stock obtained. Here is the stock price tree: 144 - 120 - So = 100 - = 108 - 90 - - 81

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts