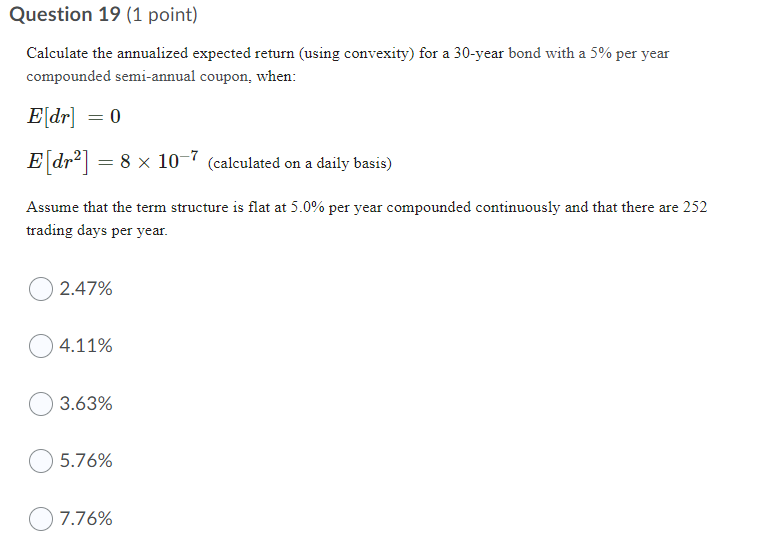

Question: Question 19 (1 point) a Calculate the annualized expected return (using convexity) for a 30-year bond with a 5% per year compounded semi-annual coupon, when:

Question 19 (1 point) a Calculate the annualized expected return (using convexity) for a 30-year bond with a 5% per year compounded semi-annual coupon, when: E[dr] 0 E [dr2] = 8 x 10-7 (calculated on a daily basis) = Assume that the term structure is flat at 5.0% per year compounded continuously and that there are 252 trading days per year. 2.47% 4.11% 3.63% 5.76% 7.76% Question 19 (1 point) a Calculate the annualized expected return (using convexity) for a 30-year bond with a 5% per year compounded semi-annual coupon, when: E[dr] 0 E [dr2] = 8 x 10-7 (calculated on a daily basis) = Assume that the term structure is flat at 5.0% per year compounded continuously and that there are 252 trading days per year. 2.47% 4.11% 3.63% 5.76% 7.76%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts