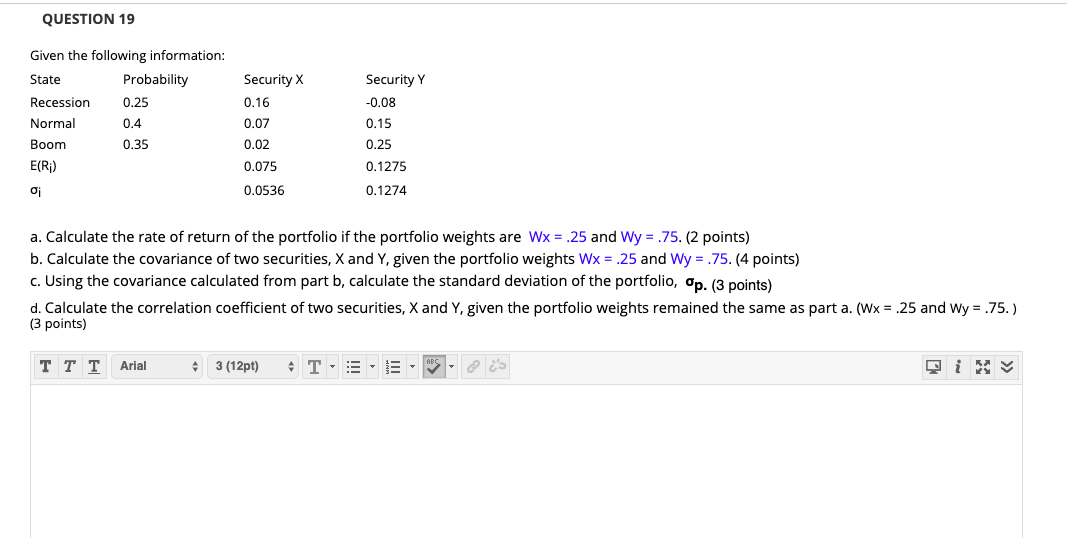

Question: QUESTION 19 Given the following information: State Probability Recession Normal 0.4 Boom 0.35 E(Ri) 0.25 Security X 0.16 0.07 0.02 0.075 0.0536 Security Y -0.08

QUESTION 19 Given the following information: State Probability Recession Normal 0.4 Boom 0.35 E(Ri) 0.25 Security X 0.16 0.07 0.02 0.075 0.0536 Security Y -0.08 0.15 0.25 0.1275 0.1274 a. Calculate the rate of return of the portfolio if the portfolio weights are Wx = -25 and Wy = .75. (2 points) b. Calculate the covariance of two securities, X and Y, given the portfolio weights Wx = 25 and Wy = .75.(4 points) c. Using the covariance calculated from part b, calculate the standard deviation of the portfolio, Op. (3 points) d. Calculate the correlation coefficient of two securities, X and Y, given the portfolio weights remained the same as part a. (Wx = 25 and Wy = .75.) (3 points) TTT Arial 3 (12pt) T - - E - m ecs

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts