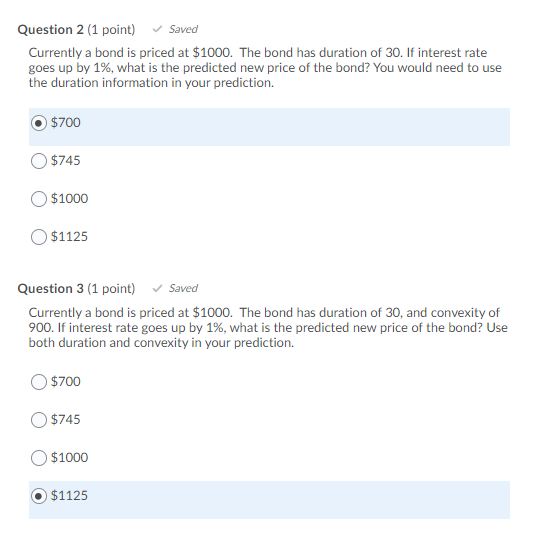

Question: Question 2 (1 point) Saved Currently a bond is priced at $1000. The bond has duration of 30. If interest rate goes up by 1%,

Question 2 (1 point) Saved Currently a bond is priced at $1000. The bond has duration of 30. If interest rate goes up by 1%, what is the predicted new price of the bond? You would need to use the duration information in your prediction. $700 $745 $1000 $1125 Question 3 (1 point) Saved Currently a bond is priced at $1000. The bond has duration of 30, and convexity of 900. If interest rate goes up by 1%, what is the predicted new price of the bond? Use both duration and convexity in your prediction. $700 $745 $1000 $1125

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock