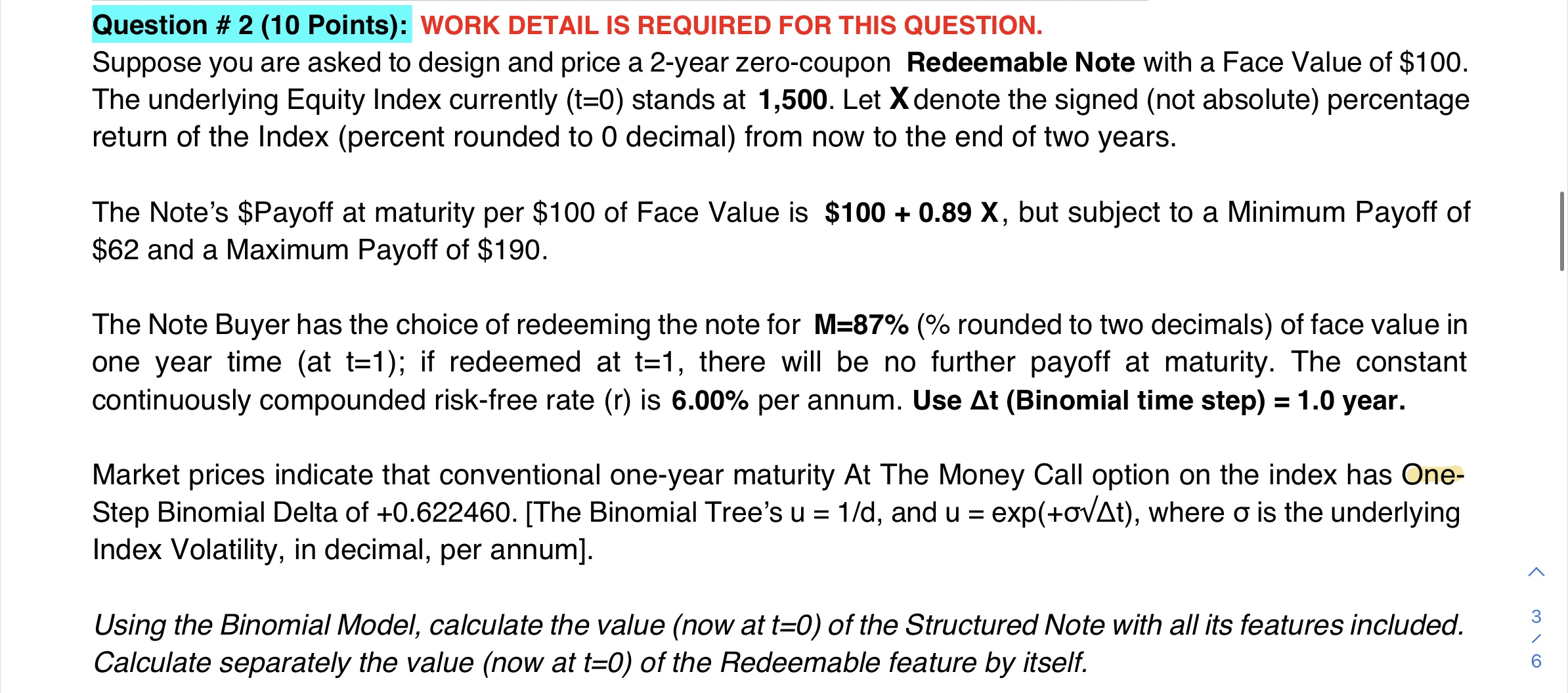

Question: Question # 2 (10 Points): WORK DETAIL IS REQUIRED FOR THIS QUESTION. Suppose you are asked to design and price a 2-year zero-coupon Redeemable Note

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts