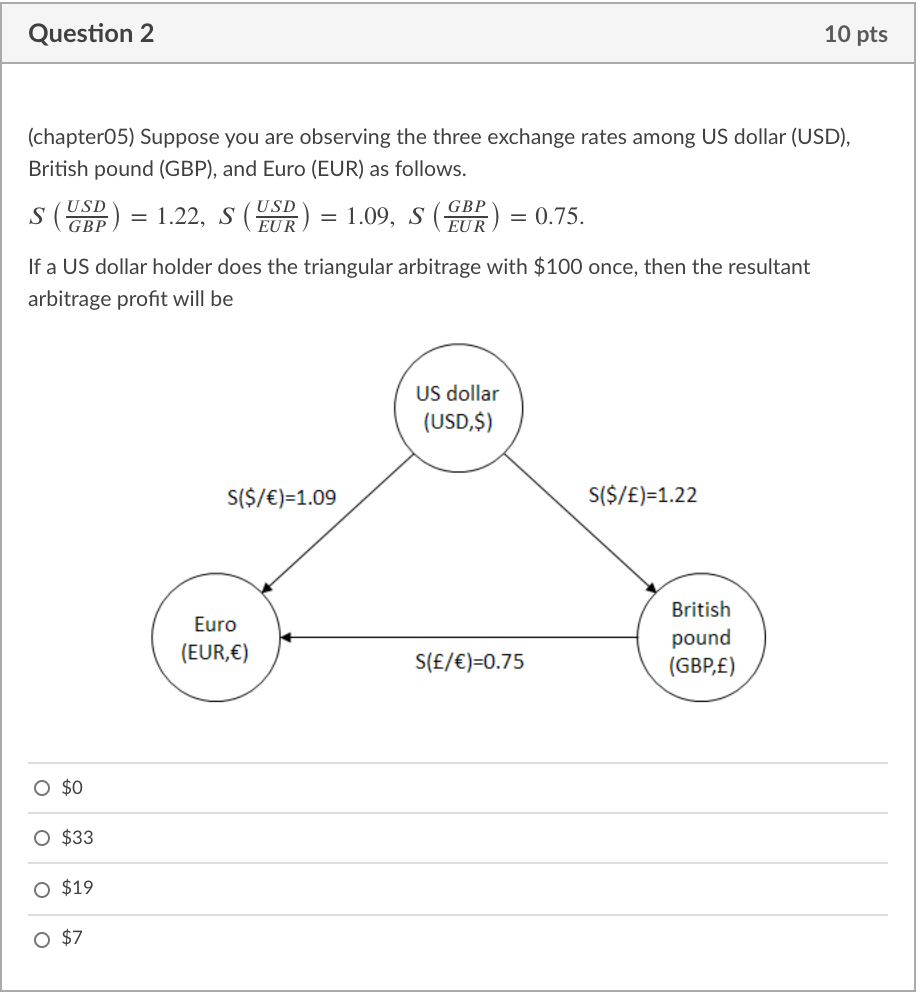

Question: Question 2 10 pts (chapter05) Suppose you are observing the three exchange rates among US dollar (USD), British pound (GBP), and Euro (EUR) as follows.

Question 2 10 pts (chapter05) Suppose you are observing the three exchange rates among US dollar (USD), British pound (GBP), and Euro (EUR) as follows. USD USD S GBP = 1.22, s EUR = 1.09, S (EBR) = 0.75. If a US dollar holder does the triangular arbitrage with $100 once, then the resultant arbitrage profit will be US dollar (USD$) S($/ )=1.09 S($/)=1.22 British Euro (EUR,) S(/ )=0.75 pound (GBP,) O $0 O $33 O $19 O $7

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock