Question: Question 2 (12 marks) Dan, a foreign exchange trader at Credit Swiss, can invest A$2 million, or its the foreign currency equivalent, in a covered

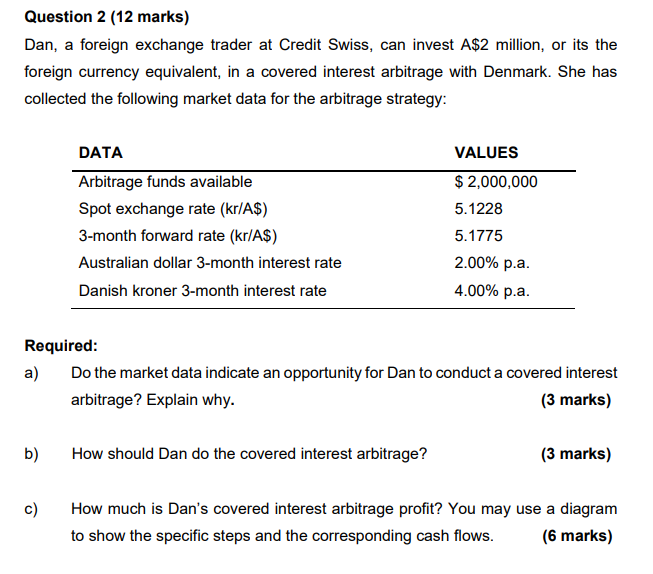

Question 2 (12 marks) Dan, a foreign exchange trader at Credit Swiss, can invest A$2 million, or its the foreign currency equivalent, in a covered interest arbitrage with Denmark. She has collected the following market data for the arbitrage strategy: DATA VALUES Arbitrage funds available $ 2,000,000 5.1228 Spot exchange rate (kr/A$) 3-month forward rate (kr/A$) 5.1775 Australian dollar 3-month interest rate 2.00% p.a. Danish kroner 3-month interest rate 4.00% p.a. Required: a) Do the market data indicate an opportunity for Dan to conduct a covered interest arbitrage? Explain why. (3 marks) b) How should Dan do the covered interest arbitrage? (3 marks) c) How much is Dan's covered interest arbitrage profit? You may use a diagram to show the specific steps and the corresponding cash flows. (6 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts