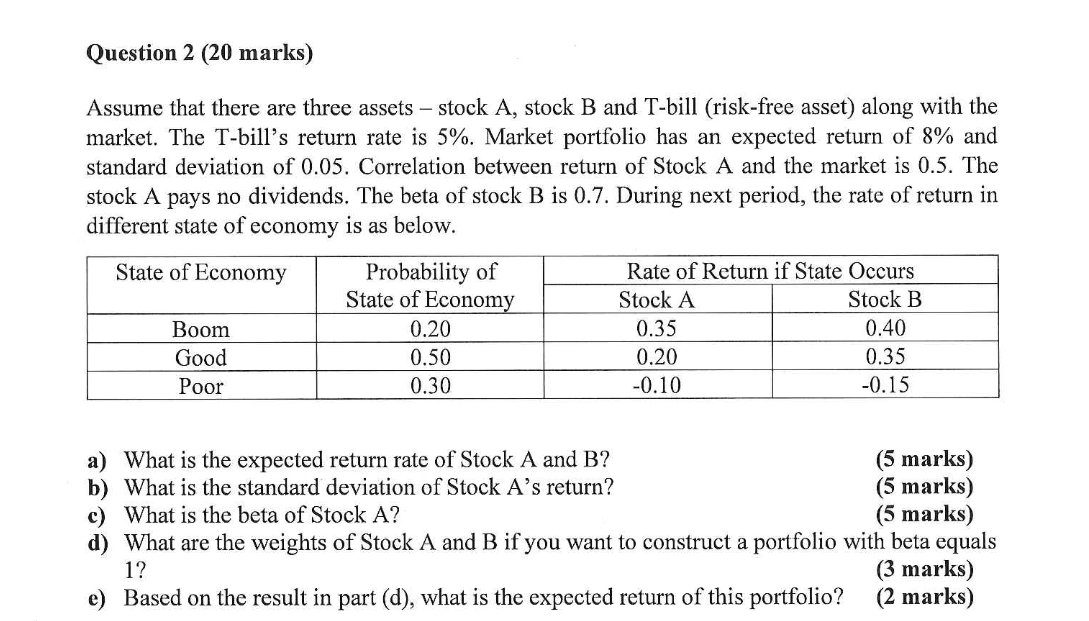

Question: Question 2 (20 marks) Assume that there are three assets - stock A, stock B and T-bill (risk-free asset) along with the market. The

Question 2 (20 marks) Assume that there are three assets - stock A, stock B and T-bill (risk-free asset) along with the market. The T-bill's return rate is 5%. Market portfolio has an expected return of 8% and standard deviation of 0.05. Correlation between return of Stock A and the market is 0.5. The stock A pays no dividends. The beta of stock B is 0.7. During next period, the rate of return in different state of economy is as below. State of Economy Probability of Boom Good Poor State of Economy 0.20 0.50 0.30 Rate of Return if State Occurs Stock A Stock B 0.35 0.40 0.20 0.35 -0.10 -0.15 a) What is the expected return rate of Stock A and B? (5 marks) b) What is the standard deviation of Stock A's return? c) What is the beta of Stock A? (5 marks) (5 marks) d) What are the weights of Stock A and B if you want to construct a portfolio with beta equals 1? (3 marks) e) Based on the result in part (d), what is the expected return of this portfolio? (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts