Question: Question 2 (20 points in total): Let's consider a world with only two dates: Today and Tomorrow. There are three possible states tomorrow: Burst, Normal,

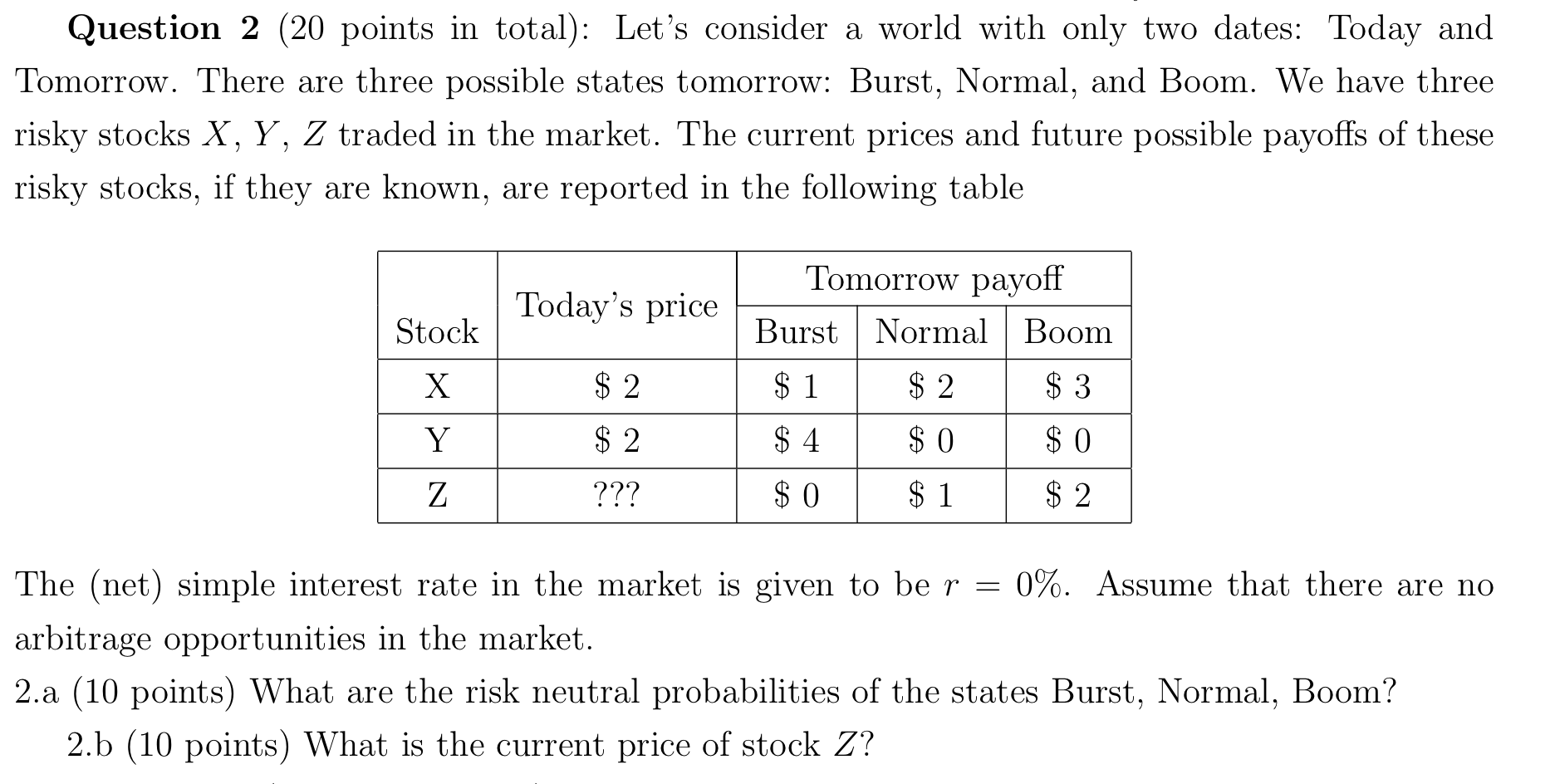

Question 2 (20 points in total): Let's consider a world with only two dates: Today and Tomorrow. There are three possible states tomorrow: Burst, Normal, and Boom. We have three risky stocks X, Y, Z traded in the market. The current prices and future possible payoffs of these risky stocks, if they are known, are reported in the following table Today's price Tomorrow payoff Burst Normal Boom Stock X $ 2 $ 1 $ 2 $ 3 Y $ 2 $ 4. $ 0 $ 0 $ 1 Z ??? $ 0 $ 2 The (net) simple interest rate in the market is given to be r = 0%. Assume that there are no arbitrage opportunities in the market. 2.a (10 points) What are the risk neutral probabilities of the states Burst, Normal, Boom? 2.b (10 points) What is the current price of stock Z? Question 2 (20 points in total): Let's consider a world with only two dates: Today and Tomorrow. There are three possible states tomorrow: Burst, Normal, and Boom. We have three risky stocks X, Y, Z traded in the market. The current prices and future possible payoffs of these risky stocks, if they are known, are reported in the following table Today's price Tomorrow payoff Burst Normal Boom Stock X $ 2 $ 1 $ 2 $ 3 Y $ 2 $ 4. $ 0 $ 0 $ 1 Z ??? $ 0 $ 2 The (net) simple interest rate in the market is given to be r = 0%. Assume that there are no arbitrage opportunities in the market. 2.a (10 points) What are the risk neutral probabilities of the states Burst, Normal, Boom? 2.b (10 points) What is the current price of stock Z

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts