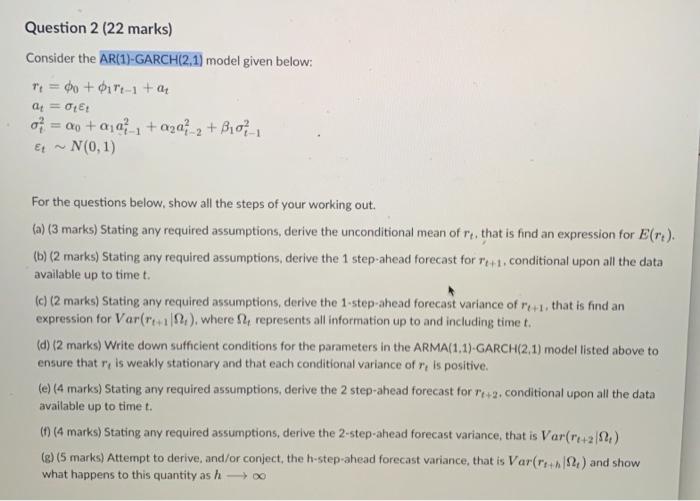

Question: Question 2 (22 marks) Consider the AR(1)-GARCH(2,1) model given below: T = 00 +017-1 + a at = Ott o= ao+aa1 + aa2+B0_1 Et~ N(0,

Question 2 (22 marks) Consider the AR(1)-GARCH(2,1) model given below: T = 00 +017-1 + a at = Ott o= ao+aa1 + aa2+B0_1 Et~ N(0, 1) For the questions below, show all the steps of your working out. (a) (3 marks) Stating any required assumptions, derive the unconditional mean of re, that is find an expression for E(re). (b) (2 marks) Stating any required assumptions, derive the 1 step-ahead forecast for P+1. conditional upon all the data available up to time t. (c) (2 marks) Stating any required assumptions, derive the 1-step-ahead forecast variance of r+1, that is find an expression for Var(r+1), where ft, represents all information up to and including time t. (d) (2 marks) Write down sufficient conditions for the parameters in the ARMA(1.1)-GARCH(2.1) model listed above to ensure that r, is weakly stationary and that each conditional variance of r, is positive. (e) (4 marks) Stating any required assumptions, derive the 2 step-ahead forecast for P+2, conditional upon all the data available up to time t. (f) (4 marks) Stating any required assumptions, derive the 2-step-ahead forecast variance, that is Var(+2) (g) (5 marks) Attempt to derive, and/or conject, the h-step-ahead forecast variance, that is Var(r+h) and show what happens to this quantity as h00 Question 2 (22 marks) Consider the AR(1)-GARCH(2,1) model given below: T = 00 +017-1 + a at = Ott o= ao+aa1 + aa2+B0_1 Et~ N(0, 1) For the questions below, show all the steps of your working out. (a) (3 marks) Stating any required assumptions, derive the unconditional mean of re, that is find an expression for E(re). (b) (2 marks) Stating any required assumptions, derive the 1 step-ahead forecast for P+1. conditional upon all the data available up to time t. (c) (2 marks) Stating any required assumptions, derive the 1-step-ahead forecast variance of r+1, that is find an expression for Var(r+1), where ft, represents all information up to and including time t. (d) (2 marks) Write down sufficient conditions for the parameters in the ARMA(1.1)-GARCH(2.1) model listed above to ensure that r, is weakly stationary and that each conditional variance of r, is positive. (e) (4 marks) Stating any required assumptions, derive the 2 step-ahead forecast for P+2, conditional upon all the data available up to time t. (f) (4 marks) Stating any required assumptions, derive the 2-step-ahead forecast variance, that is Var(+2) (g) (5 marks) Attempt to derive, and/or conject, the h-step-ahead forecast variance, that is Var(r+h) and show what happens to this quantity as h00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts