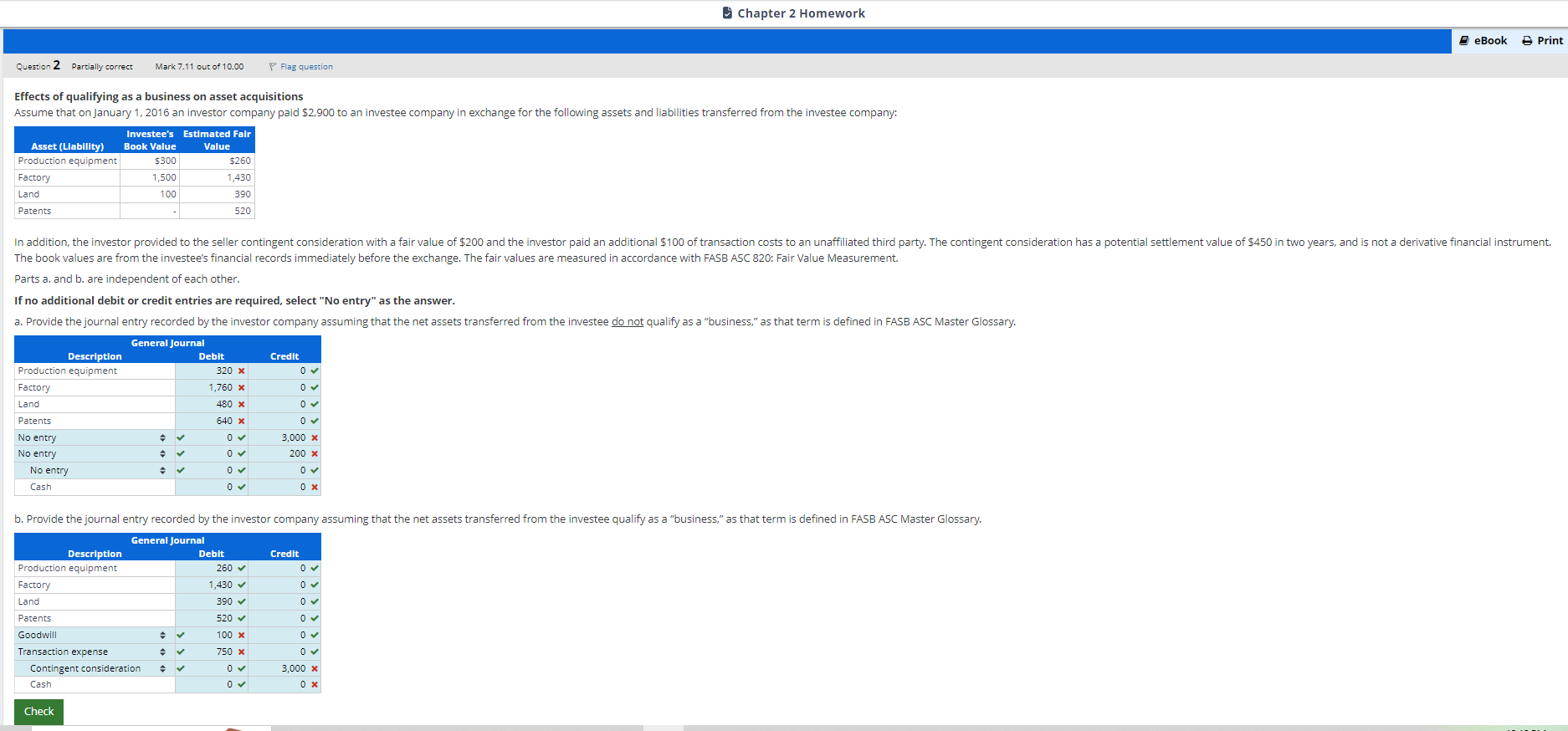

Question: Question 2- Chapter 2 Homework Queston 2 Partially corect Mark 7.1 out of 10.00 Flag question Effects of qualifying as a business on asset acquisitions

Question 2-

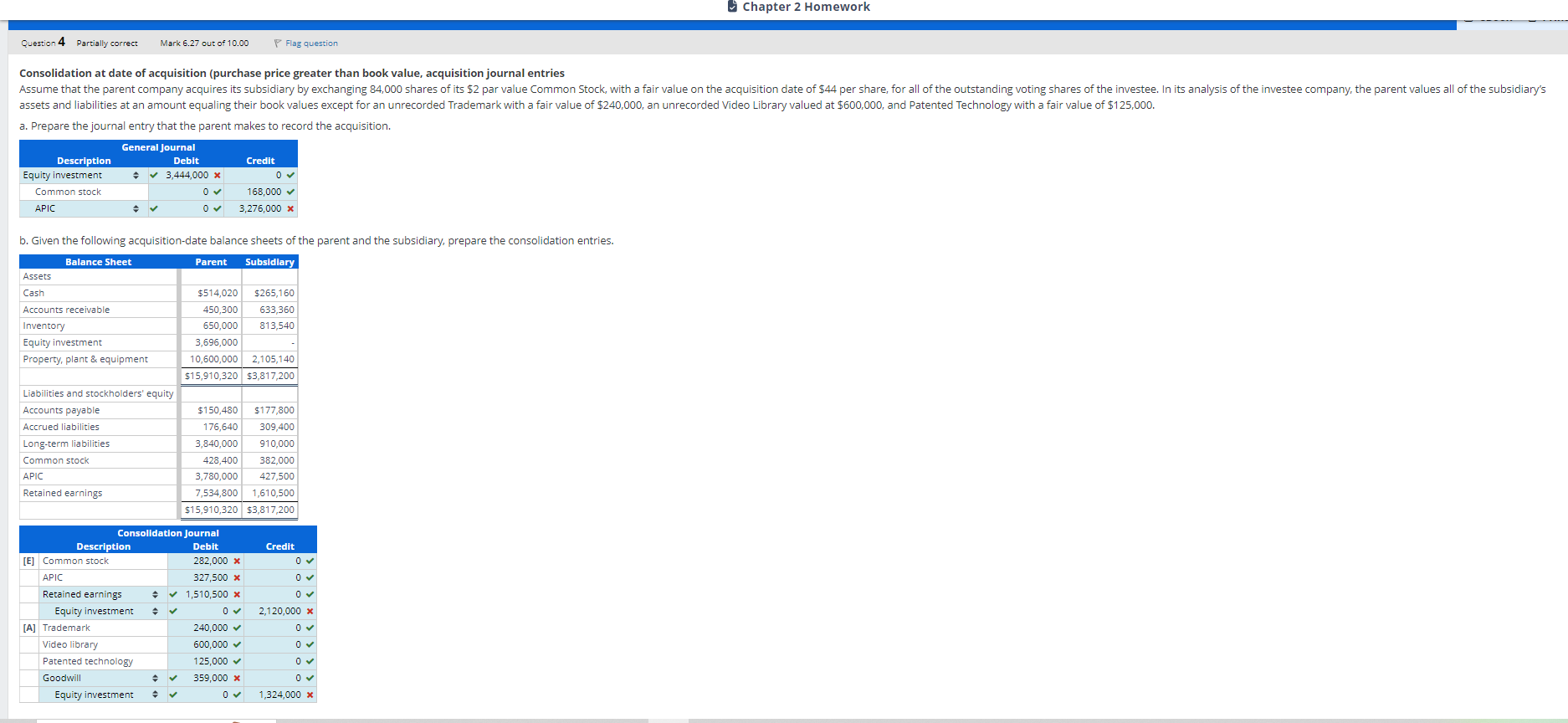

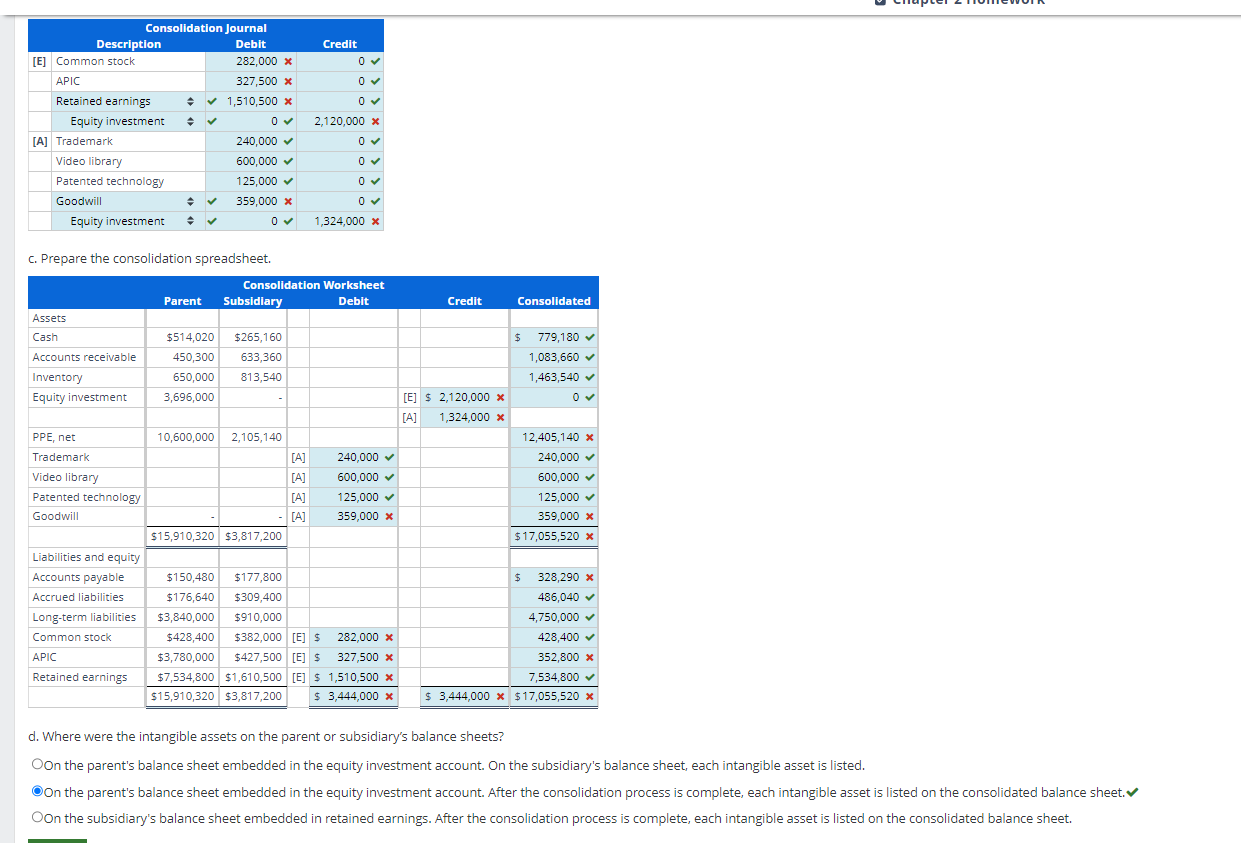

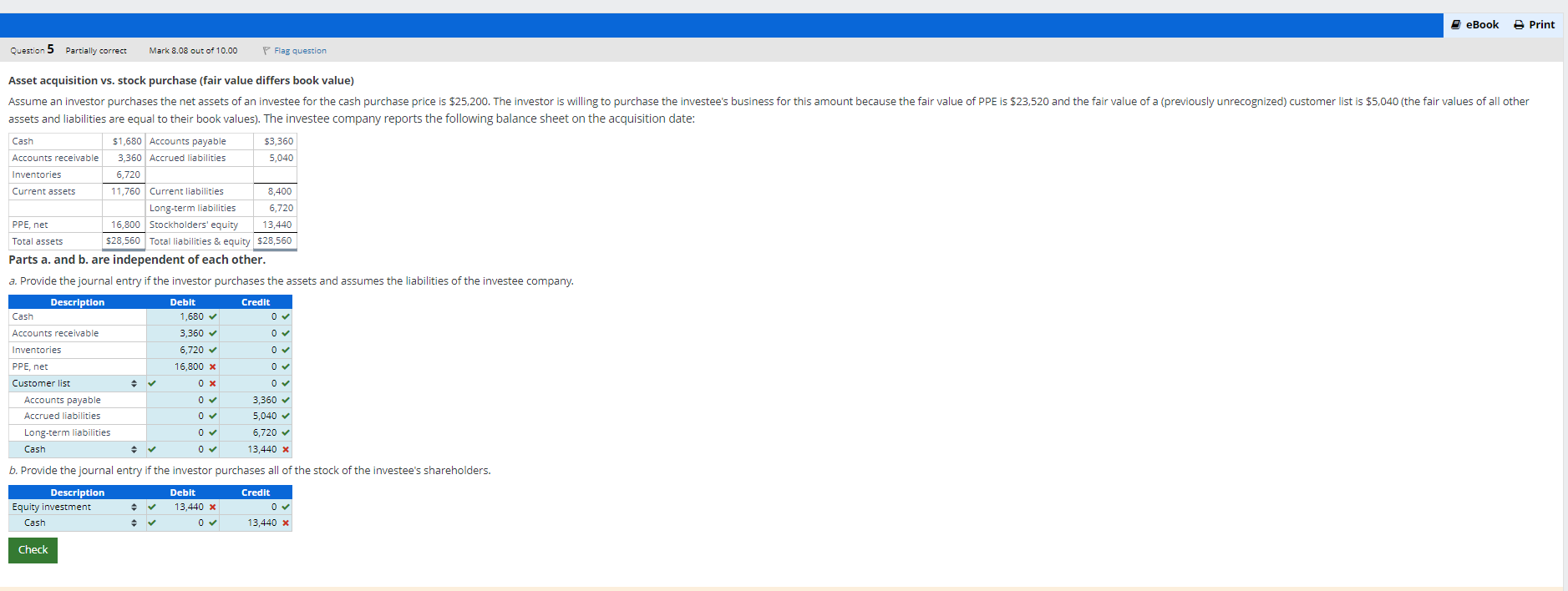

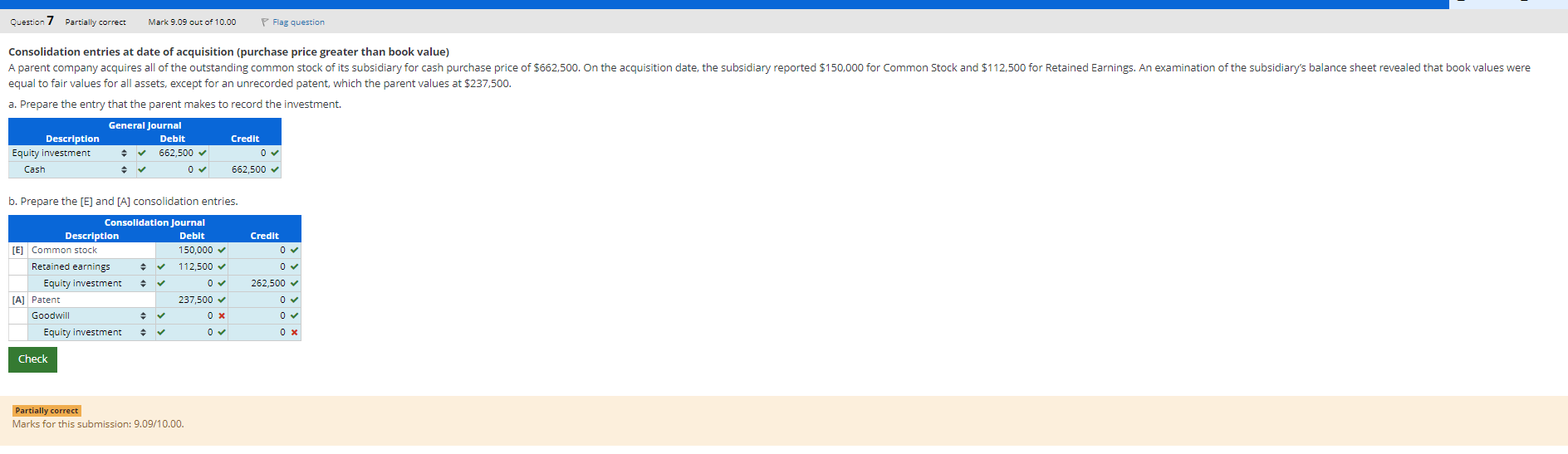

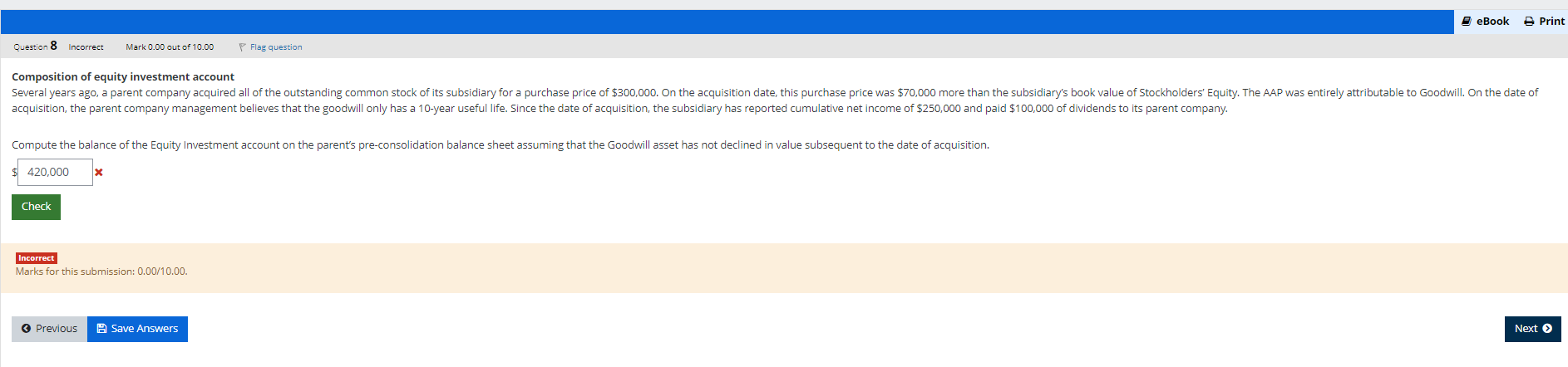

Chapter 2 Homework Queston 2 Partially corect Mark 7.1 out of 10.00 Flag question Effects of qualifying as a business on asset acquisitions Assume that on January 1, 2016 an investor company paid 52,900 to an investee company in exchange for the following assets and liabil ties transferred from the investee company: Investee's Esti LN T Production equipment 5300 Factory 1,500 Land 100 390 Paems 520 In addition, the investor provided to the seller contingent consideration with a fair value of $200 and the investor paid an additional $100 of transaction costs to an unaffiliated third party. The contingent consideration has a potential settlement value of $450 in two years, and is not a derivative financial instrument, The book values are from the investee's financial records immediately before the exchange. The fair values are measured in accordance with FASB ASC 820: Fair Value Measurement. Parts 2. and b. are independent of each other. If no additional debit or credit entries are required, select "No entry\" as the answer. 2. Provide the journal entry recorded by the investor company assuming that the net assets transferred from the Investee do not qualify as a \"business\" as that term is defined in FASE ASC Master Glossary. General Journal e Debit Credit Production equipment 320 x 0w Factory 1.760 % 0 Land 250 % ov Paems 840 x 0w No entry & v av 3,000 % No entry s v 0w 200 x No entry & v 0w 0V Cash [R% 0% b. Provide the journal entry recorded by the investor company assuming that the net assets transferred from the investee qualify as a \"business,\" as that term is defined in FASE ASC Master Glossary. General Journal L) LT Credit Production equipment 260 v 0w Factory 1430 v 0w Land 3% v v Patents 520 v 0w Gooduill s v 100 x 0w Transaction expense & v 750 0 Contingent consideration & v 0w 3,000 % Cash 0w 0% Chapter 2 Homework Question 4 Partially correct Mark 6.27 out of 10.00 P Flag question Consolidation at date of acquisition (purchase price greater than book value, acquisition journal entries Assume that the parent company acquires its subsidiary by exchanging 84,000 shares of its $2 par value Common Stock, with a fair value on the acquisition date of $44 per share, for all of the outstanding voting shares of the investee. In its analysis of the investee company, the parent values all of the subsidiary's assets and liabilities at an amount equaling their book values except for an unrecorded Trademark with a fair value of $240,000, an unrecorded Video Library valued at $600,000, and Patented Technology with a fair value of $125,000. a. Prepare the journal entry that the parent makes to record the acquisition. General Journal Description Debit Credit Equity investment 3,444,000 x Common stock Ov 168,000 APIC ov 3,276,000 x b. Given the following acquisition-date balance sheets of the parent and the subsidiary, prepare the consolidation entries. Balance Sheet Parent Subsidiary Assets Cash $514,020 $265,160 Accounts receivable 450,300 633,360 Inventory 650,000 813,540 Equity investment 3,696,000 Property, plant & equipment 10,600,000 2,105,140 $15,910,320 $3,817,200 Liabilities and stockholders' equity Accounts payable $150,480 $177,800 Accrued liabilities 176,640 309,400 Long-term liabilities 3,840,000 910,000 Common stock 428,400 382,000 APIC 3,780,000 427,500 Retained earnings 7,534,800 1,610,500 $15,910,320 $3,817,200 Consolidation Journal Description Debit Credit [E] Common stock 282,000 x APIC 327,500 x Retained earnings 1,510,500 x Equity investment OV 2,120,000 x [A] Trademark 240,000 0 Video library 500,000 0 Patented technology 125,000 Goodwill 359,000 * Equity investment OV 1,324,000 xConsolidation Journal Description Debit Credit [E] Common stock 282,000 x O V APIC 327,500 x Retained earnings 1,510,500 x OV Equity investment 2,120,000 x [A] Trademark 240,000 Video library 600,000 Patented technology 125,000 0 V Goodwill 359,000 * Equity investment 1,324,000 x c. Prepare the consolidation spreadsheet. Consolidation Worksheet Parent Subsidiary Debit Credit Consolidated Assets Cash $514,020 $265,160 $ 779,180 V Accounts receivable 450,300 633,360 1,083,660 v Inventory 650,000 813,540 1,463,540 v Equity investment 3,696,000 [E] $ 2,120,000 x ov [A] 1,324,000 x PPE, net 10,600,000 2, 105,140 12,405,140 x Trademark [A] 240,000 240,000 Video library [A] 600,000 600,000 Patented technology [A] 125,000 125,000 Goodwill [A] 359,000 * 359,000 x $15,910,320 $3,817,200 $17,055,520 x Liabilities and equity Accounts payable $150,480 $177,800 $ 328,290 x Accrued liabilities $176,640 $309,400 486,040 v Long-term liabilities $3,840,000 $910,000 4,750,000 Common stock $428,400 $382,000 [E] $ 282,000 x 428,400 APIC $3,780,000 $427,500 [E] $ 327,500 * 352,800 x Retained earnings $7,534,800 $1,610,500 [E] $ 1,510,500 x 7,534,800 $15,910,320 $3,817,200 $ 3,444,000 * $ 3,444,000 * $17,055,520 x d. Where were the intangible assets on the parent or subsidiary's balance sheets? OOn the parent's balance sheet embedded in the equity investment account. On the subsidiary's balance sheet, each intangible asset is listed. OOn the parent's balance sheet embedded in the equity investment account. After the consolidation process is complete, each intangible asset is listed on the consolidated balance sheet. v OOn the subsidiary's balance sheet embedded in retained earnings. After the consolidation process is complete, each intangible asset is listed on the consolidated balance sheet.eBook & Print Question 5 Partially correct Mark 8.08 out of 10.00 P Flag question Asset acquisition vs. stock purchase (fair value differs book value) Assume an investor purchases the net assets of an investee for the cash purchase price is $25,200. The investor is willing to purchase the investee's business for this amount because the fair value of PPE is $23,520 and the fair value of a (previously unrecognized) customer list is $5,040 (the fair values of all other assets and liabilities are equal to their book values). The investee company reports the following balance sheet on the acquisition date: Cash $1,680 Accounts payable $3,360 Accounts receivable 3,360 Accrued liabilities 5,040 Inventories 6,720 Current assets 11,760 Current liabilities 8,400 Long-term liabilities 6,720 PPE, net 16,800 Stockholders' equity 13,440 Total assets $28,560 Total liabilities & equity $28,560 Parts a. and b. are independent of each other. a. Provide the journal entry if the investor purchases the assets and assumes the liabilities of the investee company. Description Debit Credit Cash 1,680 v Accounts receivable 3,360 0 Inventories 6,720 PPE, net 16,800 x 0 V Customer list 0 x Accounts payable Ov 3,360 v Accrued liabilities 5,040 Long-term liabilities 6,720 Cash 13,440 x b. Provide the journal entry if the investor purchases all of the stock of the investee's shareholders. Description Debi Credit Equity investment 13,440 x Cash Ov 13,440 X CheckQuestion 7 Partially correct Mark 9.09 out of 10.00 Flag question Consolidation entries at date of acquisition (purchase price greater than book value) A parent company acquires all of the outstanding common stock of its subsidiary for cash purchase price of $662,500. On the acquisition date, the subsidiary reported $150,000 for Common Stock and $112,500 for Retained Earnings. An examination of the subsidiary's balance sheet revealed that book values were equal to fair values for all assets, except for an unrecorded patent, which the parent values at $237,500. a. Prepare the entry that the parent makes to record the investment. General Journal Description Debit Credit Equity investment 662,500 Cash ov 662,500 b. Prepare the [E] and [A] consolidation entries. Consolidation Journa Description Debit Credit [E] Common stock 50,000 Retained earnings 112,500 Equity investment 262,500 v [A] Patent 237,500 Goodwill 0x Equity investment theck Partially correct Marks for this submission: 9.09/10.00.Questien 8 Incorrect Mark 0.00 out of 10.00 Flag question Composition of equity investment account Several years ago, a parent company acquired all of the outstanding common stock of its subsidiary for 3 purchase price of $300,000. O the acquisition date, this purchase price was $70,000 more than the subsidiary's book value of Stockholders Equity. The AAP was entirely attributable to Goodwill. On the date of acquisition, the parent company management believes that the gooduill only has a 10-year useful life. Since the date of acquisition, the subsidiary has reported cumulative net income of $250,000 and paid $100,000 of dividends to its parent company. Compute the balance of the Equity Investment account en the parent's pre-consolidation balance shest assuming that the Goodwill asset has not declined in value subsequent to the date of acquisition. 420,000 x Marks for this submission: 0.00/10.00. @ Previous LV

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!