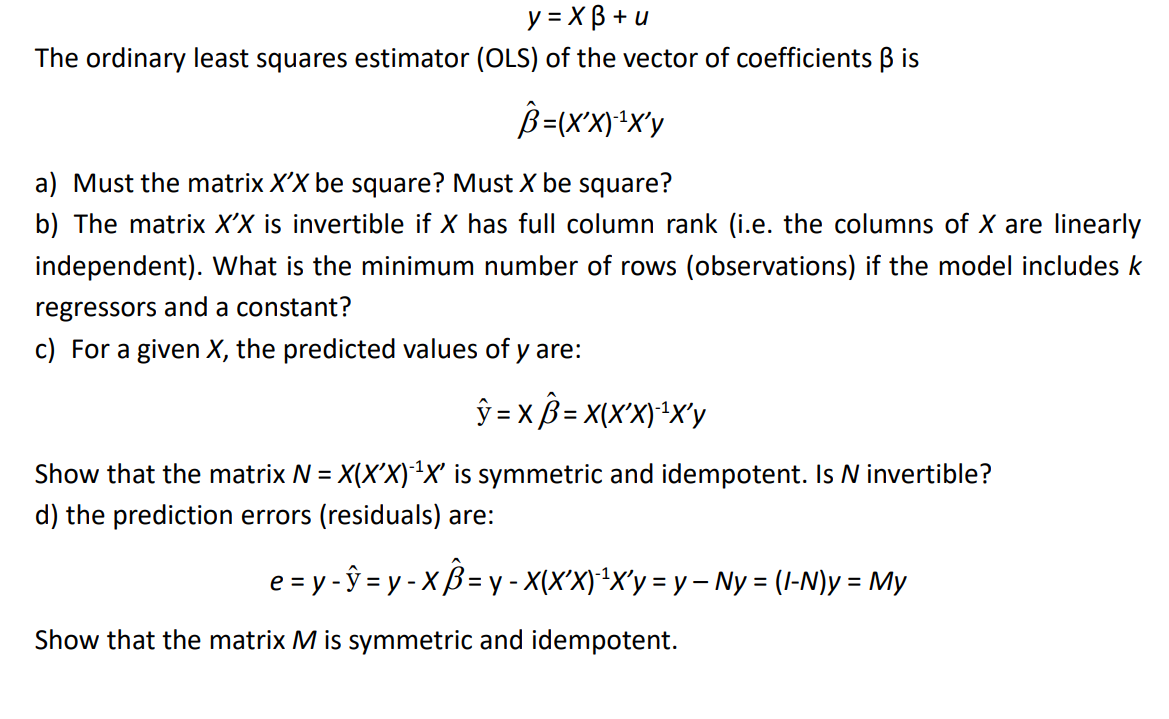

Question: Question 2 Consider the multivariate linear regression model that is described in Turkington (2007, p.71- 72.) y = XB +u The ordinary least squares estimator

Question 2 Consider the multivariate linear regression model that is described in Turkington (2007, p.71- 72.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock