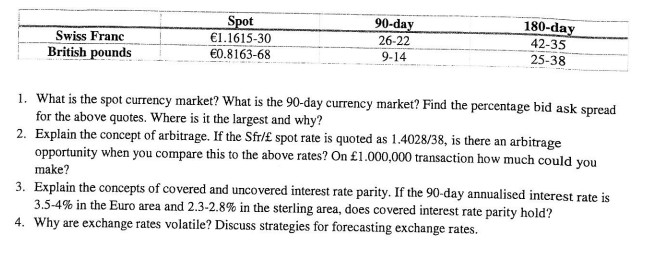

Question: Question 2 please. how do you calculate the arbitrage? Swiss Franc British pounds po E1.1615-30 60.8163-68 90-day 26-22 9-14 180-day 42-35 25-38 90-day currency market?

Question 2 please. how do you calculate the arbitrage?

Swiss Franc British pounds po E1.1615-30 60.8163-68 90-day 26-22 9-14 180-day 42-35 25-38 90-day currency market? Find the percentage bid ask spread What is the spot currency market? What is the for the above quotes. Where is it the largest and why? Explain the concept of arbitrage. If the Sfr/E spot rate is quoted as 1.4028/38, is there an arbitrage opportunity when you compare this to the above rates? On 1.000,000 transaction how much could you make? Explain the concepts of covered and uncovered interest rate parity. If the 90-day annualised interest rate is 35-4% in the Euro area and 23-28% in the sterling area, does covered interest rate parity hold? Why are exchange rates volatile? Discuss strategies for forecasting exchange rates 1. 2. 3. 4

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts