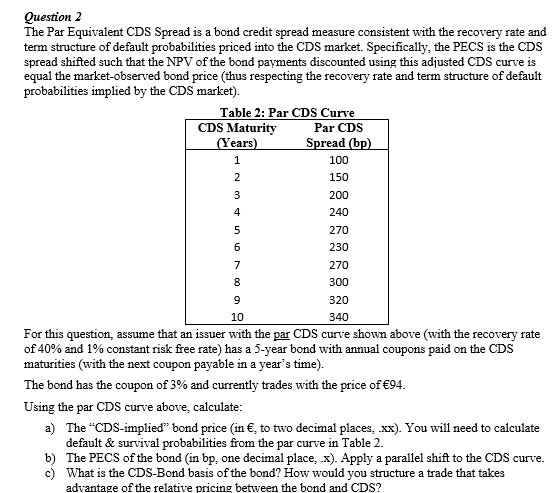

Question: Question 2 The Par Equivalent CDS Spread is a bond credit spread measure consistent with the recovery rate and term structure of default probabilities priced

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts