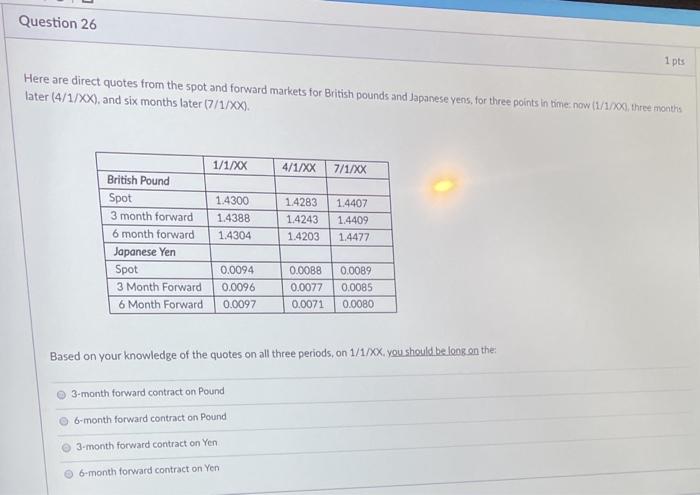

Question: Question 26 1 pts Here are direct quotes from the spot and forward markets for British pounds and Japanese yens, for three points in time

Question 26 1 pts Here are direct quotes from the spot and forward markets for British pounds and Japanese yens, for three points in time now (1/1/XX, three months later (4/1/XX), and six months later (7/1/XX). 1/1/XX 4/1/XX 7/1/XX 1.4300 1.4388 1.4304 1.4283 1.4243 1.4203 1.4407 1.4409 1.4477 British Pound Spot 3 month forward 6 month forward Japanese Yen Spot 3 Month Forward 6 Month Forward 0.0094 0.0096 0.0088 0.0077 0.0071 0.0089 0.0085 0.0080 0.0097 Based on your knowledge of the quotes on all three periods, on 1/1/XX, you should be look on the 3-month forward contract on Pound 6-month forward contract on Pound 3-month forward contract on Yen 6-month forward contract on Yen

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts