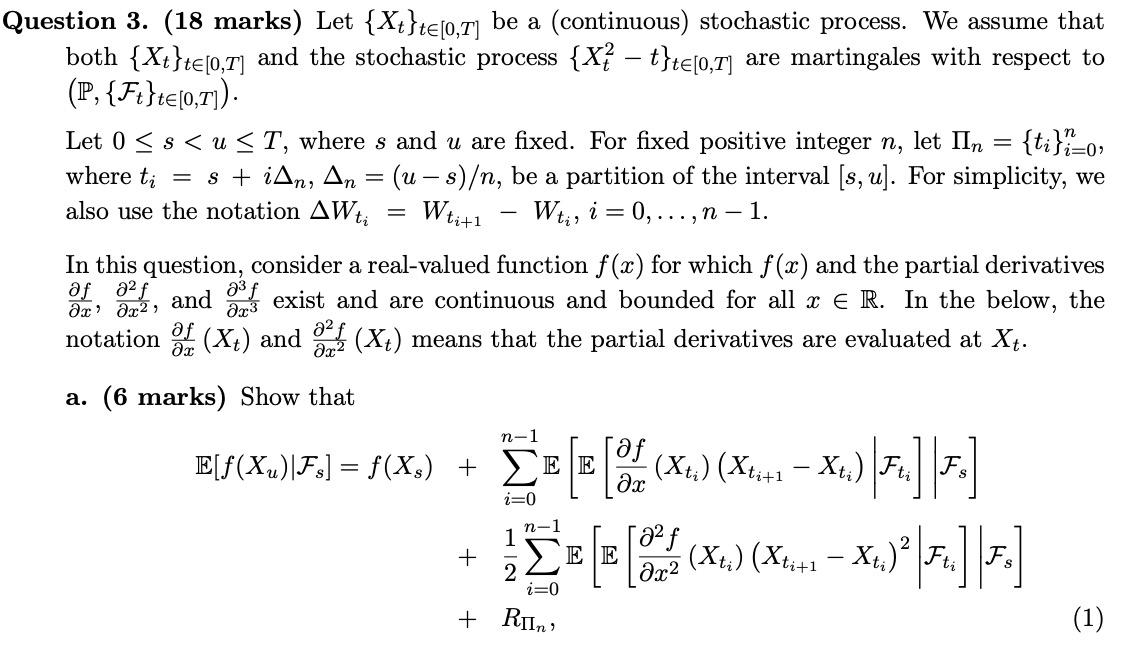

Question: Question 3. (18 marks) Let {X}teo,m be a (continuous) stochastic process. We assume that both {Xt}tejo,m and the stochastic process {X7 - theo, are martingales

![are martingales with respect to (IP, { F }telo, I]). Let 0](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6679c3a7048e2_9746679c3a6ced3e.jpg)

Question 3. (18 marks) Let {X}teo,m be a (continuous) stochastic process. We assume that both {Xt}tejo,m and the stochastic process {X7 - theo, are martingales with respect to (IP, { F }telo, I]). Let 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock