Apple just issued US$200 million 10 year bond at PAR with an annual coupon of 2%...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

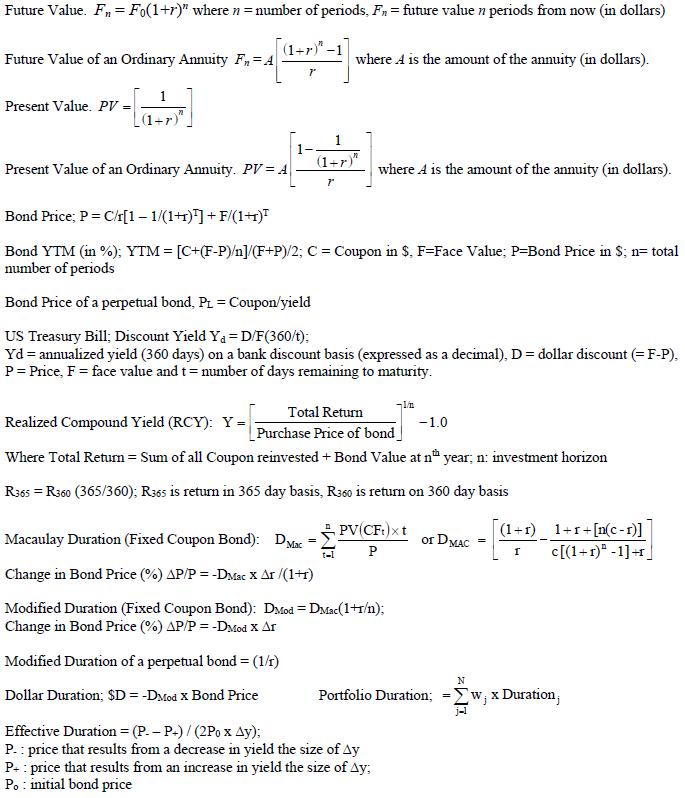

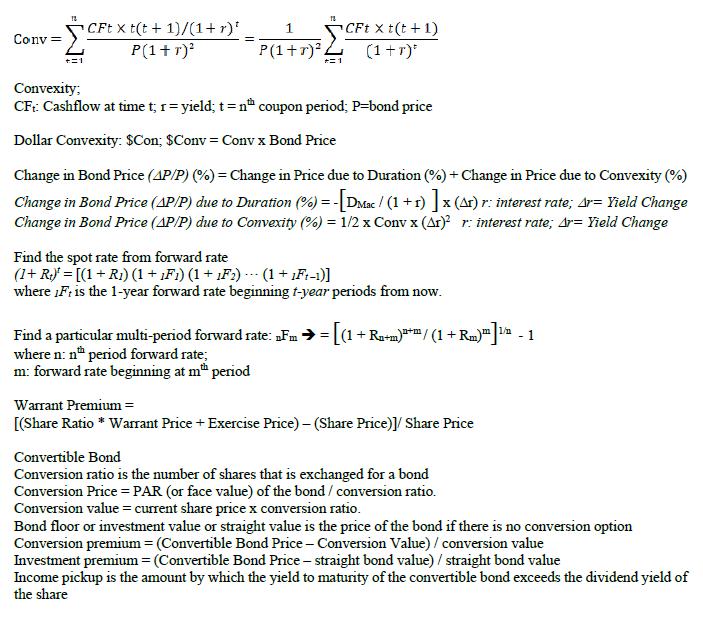

Apple just issued US$200 million 10 year bond at PAR with an annual coupon of 2% attached with a 3 year warrants on Apple shares. Each bond has a US$10,000 denomination and has 500 detachable warrants. 1 warrant allows bondholder to purchase one Apple share at an exercise price of US52. Currently the Apple share is quoted at US$40 and the Yield to Maturity (YTM) of a similar fixed coupon bond issued by Apple is 4%. (a) If the market has a standard that if a warrant has a premium greater than 20%, the warrant is then expensive. Given the issuance terms, would you recommend investors to buy this issue? Hint: Calculate the $ value per warrant to evaluation the warrant premium in %. (8 Marks) (b) At the same time as (a), Apple also issued a Convertible Bond (CB) with a zero coupon with a Conversion Price that gives the Conversion Premium the same Warrant Premium as Bond cum Warrant in (a). If investors have an extremely bullish view on Apple over the next 10 years, what would you recommend to investors between this CB and the "Bond with Warrants" described in (a). Explain the rationale between your recommendation. (2 Marks) (c) Apple is considered issuing a callable fixed coupon bond. The issuing terms are 6 year maturity with 8% annual coupon callable at year 3 and every year thereafter at a Call Price of $110. The issue price is at PAR with the yield to maturity (YTM) is 7%. A similar 6 year government bond yields 4%. If the call option part of this Callable Bond is valued at 7. The market has a comparable non callable fixed coupon bond by another issuer (EAF) that has a 3% YTM. Can you review the attractiveness of Apple callable bond's credit (or yield) spread comparing with the EAF bond? Hint: Analyze the Call Adjusted Yield spread (CAS) to assess. (5 Marks)- (d) An investor is assessing the Callable Bond in (c) with the market is expected the YTM to fall significantly. The investor wants to estimate the rough YTM level that Apple will call the bonds. Explain how the investor would work it out? (5 Marks) Future Value. F, = Fo(1+r)" where n = number of periods, Fn = future value n periods from now (in dollars) (1+r)"-1] Future Value of an Ordinary Annuity F, = A where A is the amount of the annuity (in dollars). Present Value. PV = (1+r) 1- (1+r)" Present Value of an Ordinary Annuity. PV = A where A is the amount of the annuity (in dollars). Bond Price; P = C/r[1– 1/(1+1)] + F/(1+r)F Bond YTM (in %); YTM = [C+(F-P)/n]/(F+P)/2; C = Coupon in $. F=Face Value; P=Bond Price in S; n= total number of periods Bond Price of a perpetual bond, Pr = Coupon/yield US Treasury Bill; Discount Yield Ya = D/F(360/t); Yd = annualized yield (360 days) on a bank discount basis (expressed as a decimal), D= dollar discount (= F-P). P= Price, F = face value and t= number of days remaining to maturity. Total Return Realized Compound Yield (RCY): Y = -1.0 Purchase Price of bond_ Where Total Retum = Sum of all Coupon reinvested + Bond Value at n year; n: investment horizon R365 = R360 (365/360); R365 is return in 365 day basis, R360 is retum on 360 day basis [(1+r)_ 1+r+[n(c-1)] c[(1+r)" -1]-r] PV(CF:)xt Macaulay Duration (Fixed Coupon Bond): DMae or DMAC P Change in Bond Price (%) AP/P = -DMac x Ar /(1+1) Modified Duration (Fixed Coupon Bond): DMod = DMac(1+r/n); Change in Bond Price (%) AP/P = -Dcod X Ar Modified Duration of a perpetual bond = (1/t) N Dollar Duration; $D = -DMod X Bond Price Portfolio Duration; =Ew, x Duration, %3D Effective Duration = (P. - P-)/ (2Po x Ay): P. : price that results from a decrease in yield the size of Ay P. : price that results from an increase in yield the size of Ay; Po : initial bond price CFt X t(t + 1)/(1+r)' P(1+r) CFt X t(t +1) (1+r)* Conv %3D P(1+r), Convexity; CF: Cashflow at time t; 1= yield; t=nª coupon period; P=bond price Dollar Convexity: $Con; $Conv = Conv x Bond Price Change in Bond Price (AP/P) (%) = Change in Price due to Duration (%) + Change in Price due to Convexity (%) Change in Bond Price (AP/P) due to Duration (%) = -[DMac / (1 + r) ]x (Ar) r: interest rate; Ar= Yield Change Change in Bond Price (AP/P) due to Convexity (%) = 1/2 x Conv x (Ar) r: interest rate; Ar= Yield Change Find the spot rate from forward rate (1+ R) = [(1 + R1) (1 + Fi) (1+ 1F1) - (1 + 1F:-1)] where iF: is the 1-year forward rate beginning t-year periods from now. Find a particular multi-period forward rate: „Fm >= (1+ Ra+m)*/(1+Rm) where n: n period forward rate; m: forward rate beginning at m period m 1 Warrant Premium = [(Share Ratio * Warrant Price + Exercise Price) – (Share Price)y Share Price Convertible Bond Conversion ratio is the number of shares that is exchanged for a bond Conversion Price = PAR (or face value) of the bond / conversion ratio. Conversion value = current share price x conversion ratio. Bond floor or investment value or straight value is the price of the bond if there is no conversion option Conversion premium = (Convertible Bond Price- Conversion Value) / conversion value Investment premium (Convertible Bond Price - straight bond value) / straight bond value Income pickup is the amount by which the yield to maturity of the convertible bond exceeds the dividend yield of the share Apple just issued US$200 million 10 year bond at PAR with an annual coupon of 2% attached with a 3 year warrants on Apple shares. Each bond has a US$10,000 denomination and has 500 detachable warrants. 1 warrant allows bondholder to purchase one Apple share at an exercise price of US52. Currently the Apple share is quoted at US$40 and the Yield to Maturity (YTM) of a similar fixed coupon bond issued by Apple is 4%. (a) If the market has a standard that if a warrant has a premium greater than 20%, the warrant is then expensive. Given the issuance terms, would you recommend investors to buy this issue? Hint: Calculate the $ value per warrant to evaluation the warrant premium in %. (8 Marks) (b) At the same time as (a), Apple also issued a Convertible Bond (CB) with a zero coupon with a Conversion Price that gives the Conversion Premium the same Warrant Premium as Bond cum Warrant in (a). If investors have an extremely bullish view on Apple over the next 10 years, what would you recommend to investors between this CB and the "Bond with Warrants" described in (a). Explain the rationale between your recommendation. (2 Marks) (c) Apple is considered issuing a callable fixed coupon bond. The issuing terms are 6 year maturity with 8% annual coupon callable at year 3 and every year thereafter at a Call Price of $110. The issue price is at PAR with the yield to maturity (YTM) is 7%. A similar 6 year government bond yields 4%. If the call option part of this Callable Bond is valued at 7. The market has a comparable non callable fixed coupon bond by another issuer (EAF) that has a 3% YTM. Can you review the attractiveness of Apple callable bond's credit (or yield) spread comparing with the EAF bond? Hint: Analyze the Call Adjusted Yield spread (CAS) to assess. (5 Marks)- (d) An investor is assessing the Callable Bond in (c) with the market is expected the YTM to fall significantly. The investor wants to estimate the rough YTM level that Apple will call the bonds. Explain how the investor would work it out? (5 Marks) Future Value. F, = Fo(1+r)" where n = number of periods, Fn = future value n periods from now (in dollars) (1+r)"-1] Future Value of an Ordinary Annuity F, = A where A is the amount of the annuity (in dollars). Present Value. PV = (1+r) 1- (1+r)" Present Value of an Ordinary Annuity. PV = A where A is the amount of the annuity (in dollars). Bond Price; P = C/r[1– 1/(1+1)] + F/(1+r)F Bond YTM (in %); YTM = [C+(F-P)/n]/(F+P)/2; C = Coupon in $. F=Face Value; P=Bond Price in S; n= total number of periods Bond Price of a perpetual bond, Pr = Coupon/yield US Treasury Bill; Discount Yield Ya = D/F(360/t); Yd = annualized yield (360 days) on a bank discount basis (expressed as a decimal), D= dollar discount (= F-P). P= Price, F = face value and t= number of days remaining to maturity. Total Return Realized Compound Yield (RCY): Y = -1.0 Purchase Price of bond_ Where Total Retum = Sum of all Coupon reinvested + Bond Value at n year; n: investment horizon R365 = R360 (365/360); R365 is return in 365 day basis, R360 is retum on 360 day basis [(1+r)_ 1+r+[n(c-1)] c[(1+r)" -1]-r] PV(CF:)xt Macaulay Duration (Fixed Coupon Bond): DMae or DMAC P Change in Bond Price (%) AP/P = -DMac x Ar /(1+1) Modified Duration (Fixed Coupon Bond): DMod = DMac(1+r/n); Change in Bond Price (%) AP/P = -Dcod X Ar Modified Duration of a perpetual bond = (1/t) N Dollar Duration; $D = -DMod X Bond Price Portfolio Duration; =Ew, x Duration, %3D Effective Duration = (P. - P-)/ (2Po x Ay): P. : price that results from a decrease in yield the size of Ay P. : price that results from an increase in yield the size of Ay; Po : initial bond price CFt X t(t + 1)/(1+r)' P(1+r) CFt X t(t +1) (1+r)* Conv %3D P(1+r), Convexity; CF: Cashflow at time t; 1= yield; t=nª coupon period; P=bond price Dollar Convexity: $Con; $Conv = Conv x Bond Price Change in Bond Price (AP/P) (%) = Change in Price due to Duration (%) + Change in Price due to Convexity (%) Change in Bond Price (AP/P) due to Duration (%) = -[DMac / (1 + r) ]x (Ar) r: interest rate; Ar= Yield Change Change in Bond Price (AP/P) due to Convexity (%) = 1/2 x Conv x (Ar) r: interest rate; Ar= Yield Change Find the spot rate from forward rate (1+ R) = [(1 + R1) (1 + Fi) (1+ 1F1) - (1 + 1F:-1)] where iF: is the 1-year forward rate beginning t-year periods from now. Find a particular multi-period forward rate: „Fm >= (1+ Ra+m)*/(1+Rm) where n: n period forward rate; m: forward rate beginning at m period m 1 Warrant Premium = [(Share Ratio * Warrant Price + Exercise Price) – (Share Price)y Share Price Convertible Bond Conversion ratio is the number of shares that is exchanged for a bond Conversion Price = PAR (or face value) of the bond / conversion ratio. Conversion value = current share price x conversion ratio. Bond floor or investment value or straight value is the price of the bond if there is no conversion option Conversion premium = (Convertible Bond Price- Conversion Value) / conversion value Investment premium (Convertible Bond Price - straight bond value) / straight bond value Income pickup is the amount by which the yield to maturity of the convertible bond exceeds the dividend yield of the share

Expert Answer:

Answer rating: 100% (QA)

a Calculation of Theoretical Market Price of bond at the ... View the full answer

Related Book For

Financial Markets And Institutions

ISBN: 978-0132136839

7th Edition

Authors: Frederic S. Mishkin, Stanley G. Eakins

Posted Date:

Students also viewed these general management questions

-

A $1,000 par bond with an annual coupon has only one year until maturity. Its current yield is 6.713%, and its yield to maturity is 10%. What is the price of the bond?

-

Which of the following is not an example of a barter arrangement? A. A carpenter builds a fence for a farmer, instead of the farmer paying the builder $1,000 in cash for labor and materials, the...

-

Consider a 30-year bond paying an annual coupon of $70 and selling at par value of $1,000. The bonds initial yield to maturity is 8%. Show that if yield to maturity increases, then holding-period...

-

Develop a two-period weighted moving average forecast for periods 12 through 15. Use weights of 0.7 and 0.3, with the most recent observation weighted higher. PERIOD DEMAND 10............ 248...

-

Produce a list of the names and addresses of all employees who work for the IT department.

-

Orange Corp., a high-technology company, utilizes the following procedures for recording materials and transferring them to work in process. (1) Upon receipt of raw materials by stores, the...

-

Show that during the early part of the electron-positron annihilation era, the ratio of the electron number density to the photon number density scaled with temperature as \[\frac{n_{-}}{n_{\gamma}}...

-

The Bottled Water Company has been bottling and selling water since 1940. Ginnie Adams, the current owner of The Bottled Water Company, would like to know how a new product would affect the company's...

-

1 = We know that all the statements [4] Consider the system (0.3)-(0.4) in the particular case f(r) = proven in Problem [3] apply to this case, so for example, we know that c2 7 = - 1 12 (0.6) de and...

-

Draw the starting materials (diene and dienophile) for the preparation of the following compounds. X COOH COOH

-

You sold a certain financial asset for $133.10 just now. You had purchased this asset three years ago for $100.00. Your investment of $100 in this asset in the market had a value of $116.00 at the...

-

Write in your own words, what is the main idea behind the Divide and Conquer algorithms and Which one among the following step is always present in a Divide and Conquer algorithm, recursion or...

-

Company O has outstanding accounts receivables of $1,650,000 at year-end. During the year, $35,000 of accounts receivables were written-o. The company estimates allowance for bad debts to be 3% of...

-

Difference between ascomycota and basidiomycota in terms of how spores are produced

-

Show that, if r(t)= eti+ej, then r(t) and r"(t) are parallel.

-

explain how half-life of glutamine synthetase can be determined using cell lines

-

Identify two ways to deposit money into and withdraw money out of your checking account. What is one disadvantage of NOT having a checking account? Every time you owe a person or business money, you...

-

1. Firms may hold financial assets to earn returns. How the firm would classify financial assets? What treatment will such financial assets get in the financial statements in accordance with US GAAP...

-

Suppose that the pension you are managing is expecting an inflow of funds of $100 million next year and you want to make sure that you will earn the current interest rate of 8% when you invest the...

-

A bank currently holds $150,000 in excess reserves. If the current reserve requirement is 12.5%, how much could the money supply change? How could this happen?

-

What would be your annualized discount rate % and your annualized investment rate % on the purchase of a 182-day Treasury bill for $4,925 that pays $5,000 at maturity?

-

Compare the full sets of public service announcements (PSAs) represented by Figures 7.11, 7.12, and 7.13 by visiting http://city.milwaukee.gov/health/Safe-Sleep-Campaign. Which set is most effective?...

-

In a pair or in small groups, find three online shopping sites that sell similar types of merchandise (e.g., Backcountry.com, Moosejaw.com, REI.com). Consider the following questions: Who are the...

-

Ask someone to follow a set of instructions or to fill out a form. As an alternative, you also might test a document youve created for a course. You also may try ordering food from a website, such as...

Study smarter with the SolutionInn App