Question: QUESTION 3 (a) Let S = RM100, K = 90, r = 8%, o = 5% and T = 1. Find the Black-Scholes call price.

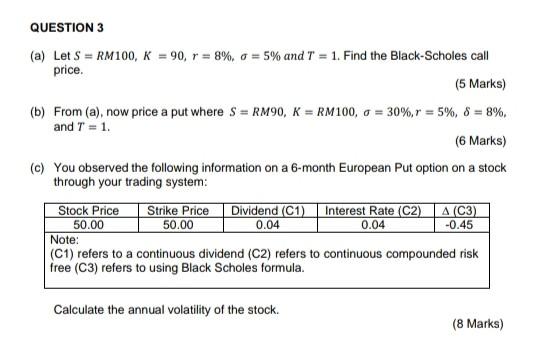

QUESTION 3 (a) Let S = RM100, K = 90, r = 8%, o = 5% and T = 1. Find the Black-Scholes call price. (5 Marks) (b) From (a), now price a put where S = RM90, K = RM100, 0 = 30%,r = 5%, 8 = 8%. and T = 1. (6 Marks) (c) You observed the following information on a 6-month European Put option on a stock through your trading system: Stock Price Strike Price Dividend (C1) Interest Rate (C2) A (C3) 50.00 50.00 0.04 0.04 (C1) refers to a continuous dividend (C2) refers to continuous compounded risk free (C3) refers to using Black Scholes formula. -0.45 Note: Calculate the annual volatility of the stock. (8 Marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock