Question: QUESTION 3 Oct 2020 Q1 Read the case study below and answer the questions based on the case study. You have recently read through Chapter

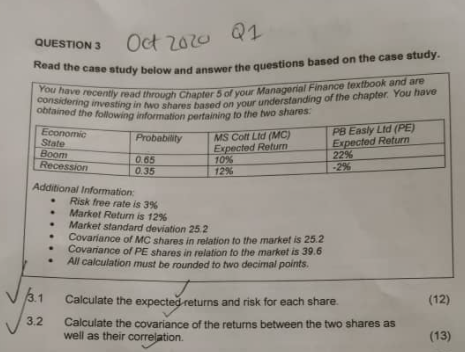

QUESTION 3 Oct 2020 Q1 Read the case study below and answer the questions based on the case study. You have recently read through Chapter 5 of your Managerial Finance textbook and are considering investing in two shares based on your understanding of the chapter. You have obtained the following information pertaining to the two shares Economic Probability MS Coff Lid (MC) PB Easy Lid (PE) Expected Return Expected Return 0.65 10% 22% 0.35 12% -2% State Boom Recession Additional Information Risk free rate is 3% Market Return is 1256 Market standard deviation 252 Covariance of MC shares in relation to the market is 25.2 Covariance of PE shares in relation to the market is 39.6 All calculation must be rounded to two decimal points, . 13.1 (12) 3.2 Calculate the expected returns and risk for each share. Calculate the covariance of the returns between the two shares as well as their correlation (13)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts